15 min read

This report analyzes the IPv4 transfer market for March 2026, based on completed IPv4Center marketplace transactions and official RIR transfer records.

Executive Summary

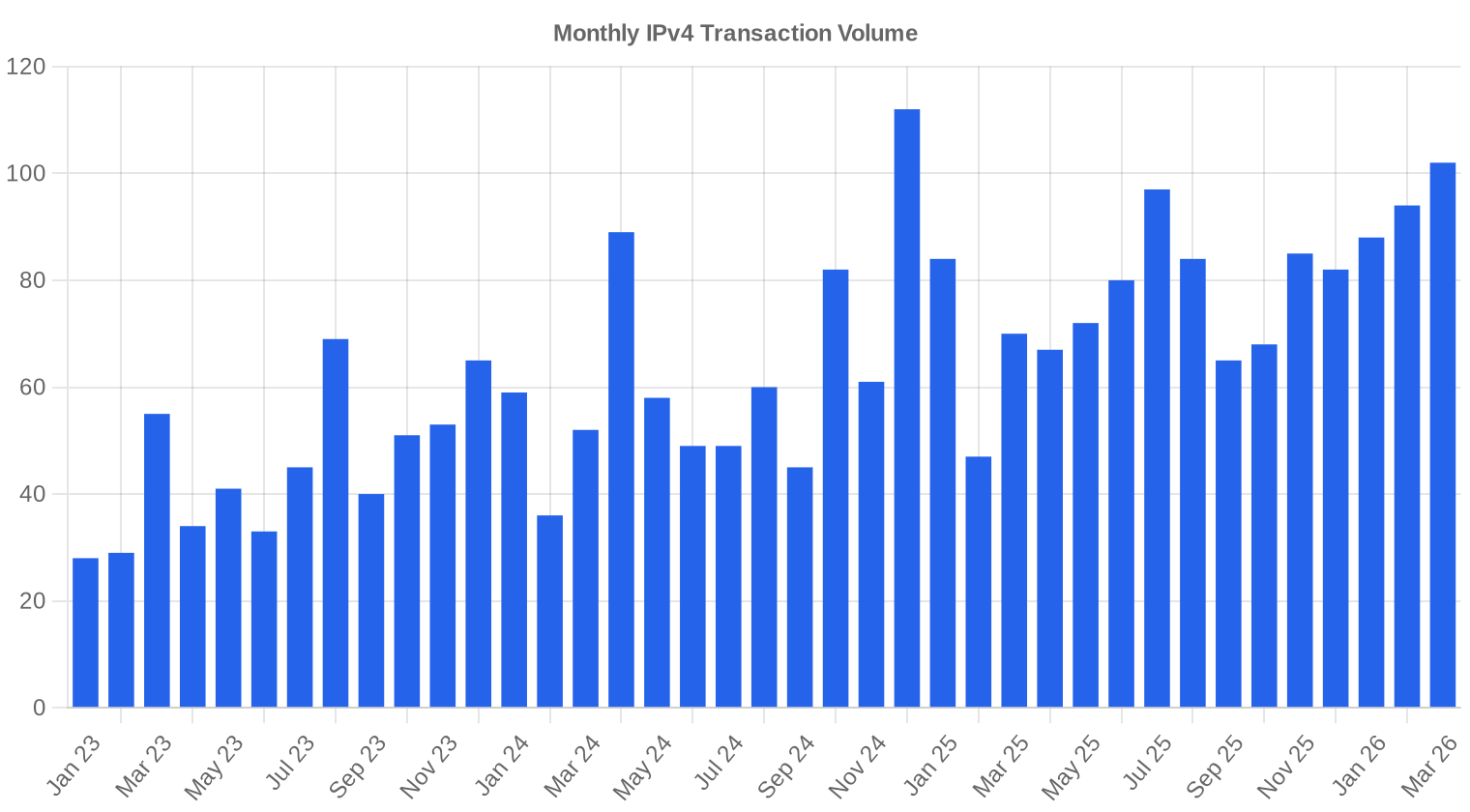

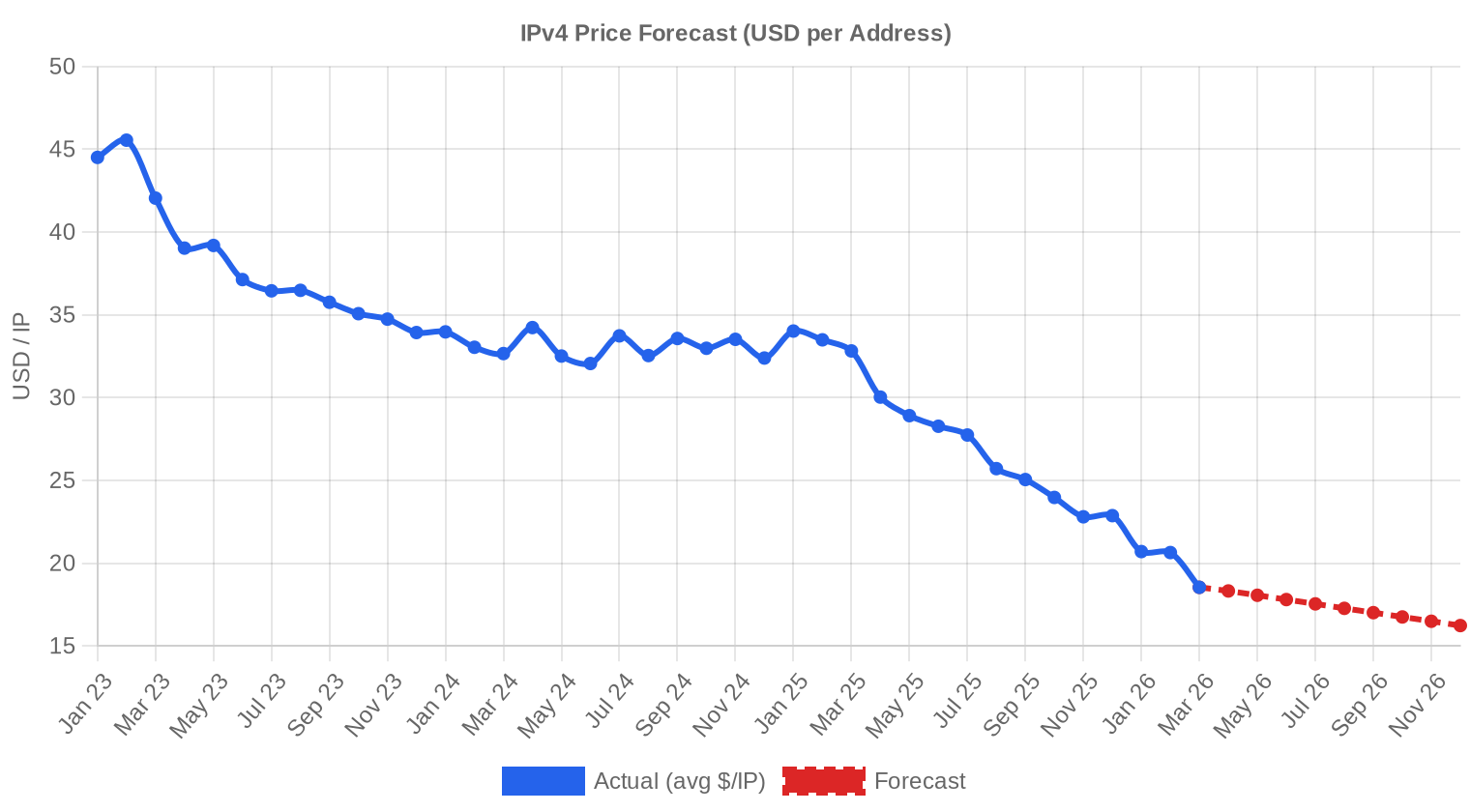

The IPv4 transfer market recorded 102 transactions in March 2026, moving 1,507,840 addresses at a weighted average of $18.54 per IP. Total deal value reached $16.1 million. The average price fell 10.2% from February's level and is now 43.5% below where it stood in March 2025 — when addresses were still fetching north of $32. Transaction volume rose 8.5% month-over-month, suggesting that buyers are stepping in at these lower levels but only at steep discounts to prior clearing prices. The trend remains firmly downward, with March's regression line slipping another 1.41%.Market Overview

| Transactions | 102 |

| IP Addresses Traded | 1,507,840 |

| Estimated Market Value | $16,126,404 |

| Average Price / IP | $18.54 |

| Median Price / IP | $18.58 |

| RIR Transfers | 826 |

Year-over-Year Comparison

| Metric | This period | A year earlier (March 2025) | Change |

|---|---|---|---|

| Transactions | 102 | 70 | +45.7% |

| IP Addresses Traded | 1,507,840 | 213,248 | +607.1% |

| Estimated Market Value | $16,126,404 | $6,149,756 | +162.2% |

| Average Price / IP | $18.54 | $32.82 | -43.5% |

| RIR Transfers | 826 | 1,434 | -42.4% |

Price Dynamics

The price range in March stretched from $9 to $34 per IP, a $25 spread that reflects enormous divergence between distressed or bulk inventory and premium small-block trades. The median of $18.58 tracked right on top of the average — unusual tightness that indicates a relatively normal distribution rather than a handful of outliers pulling the mean. The 10.2% drop from February accelerated what had already been a steady grind lower. A year ago the market was still adjusting to the AWS public IPv4 charge announced in mid-2024; the full repricing is now baked in. The floor at $9 came from large ARIN blocks where sellers are clearly prioritizing liquidity over price.

Pricing by RIR

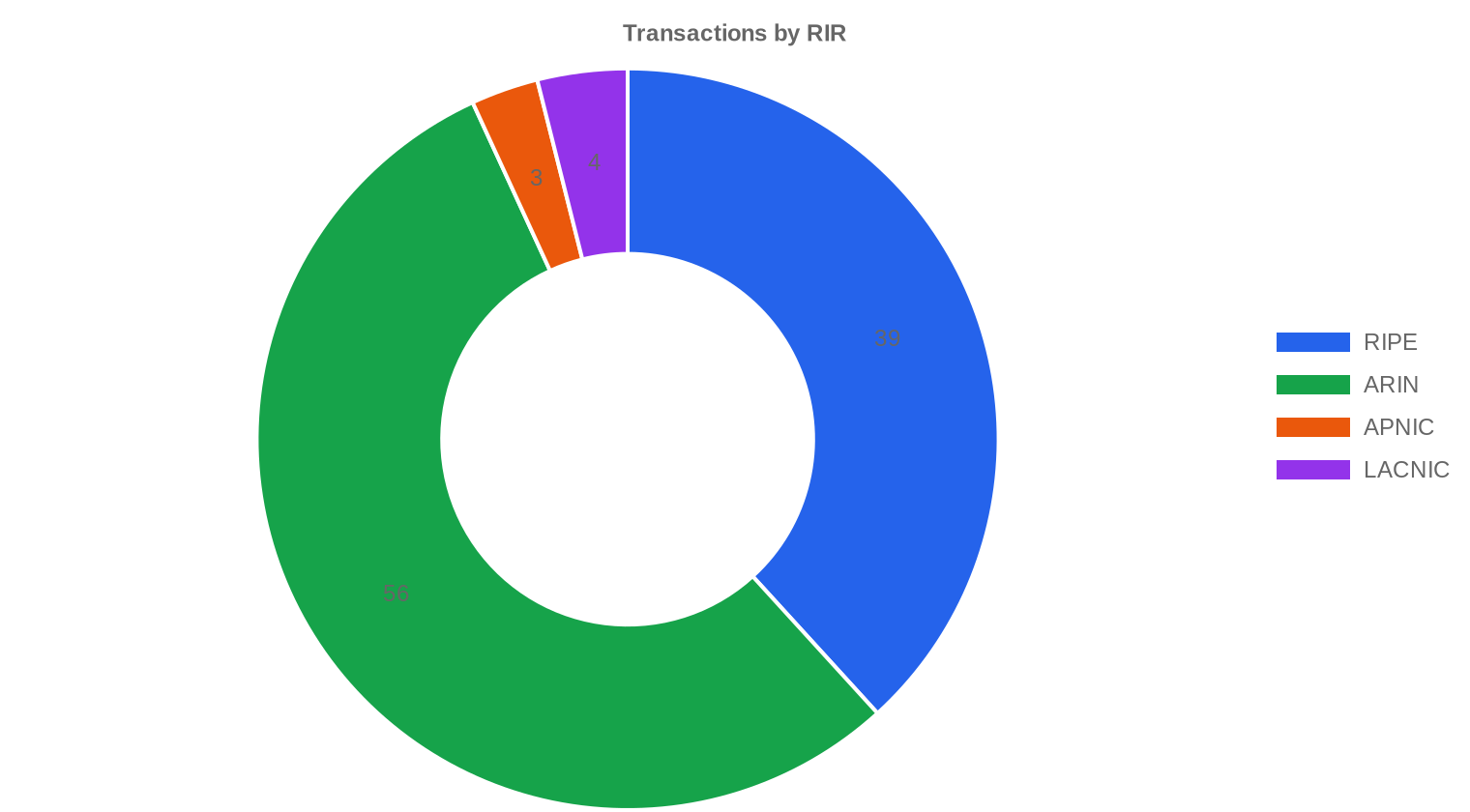

ARIN dominated March volume with 54.9% of traded addresses but offered the cheapest inventory at $16.00 per IP average across 56 transactions. RIPE blocks carried a $5.30 premium over ARIN, averaging $21.30 — a gap that has widened over recent months as RIPE supply stays constrained by the 24-month holding rule. LACNIC stood out at $25.88 per IP, a 39.6% premium to the market average, though this came from just four small transactions totaling 5,632 addresses. That premium reflects genuine scarcity in the Latin American registry, where transferable blocks are rare and buyer competition is fierce for any available space. APNIC posted $20.37 across three trades, close to RIPE levels and consistent with recent quarters.ARIN: $16.00/IP across 56 transactions (73.6% of volume).

RIPE: $21.30/IP across 39 transactions (25.4% of volume).

APNIC: $20.37/IP across 3 transactions (0.6% of volume).

LACNIC: $25.88/IP across 4 transactions (0.4% of volume).

AFRINIC: No recorded transactions.

| RIR | Transactions | Avg $/IP | Median $/IP | IPs Traded | RIR Transfers | Next Month (proj.) | Year-End (proj.) |

|---|---|---|---|---|---|---|---|

| RIPE | 39 | $21.30 | $21.50 | 382,464 | 534 | $21.00 | $18.50 |

| ARIN | 56 | $16.00 | $16.25 | 1,110,784 | 292 | $16.00 | $13.00 |

| APNIC | 3 | $20.37 | $20.00 | 8,960 | 0 | $19.50 | $16.50 |

| LACNIC | 4 | $25.88 | $26.25 | 5,632 | 0 | $26.00 | $24.00 |

Transaction Volume

Supply & Block Sizes

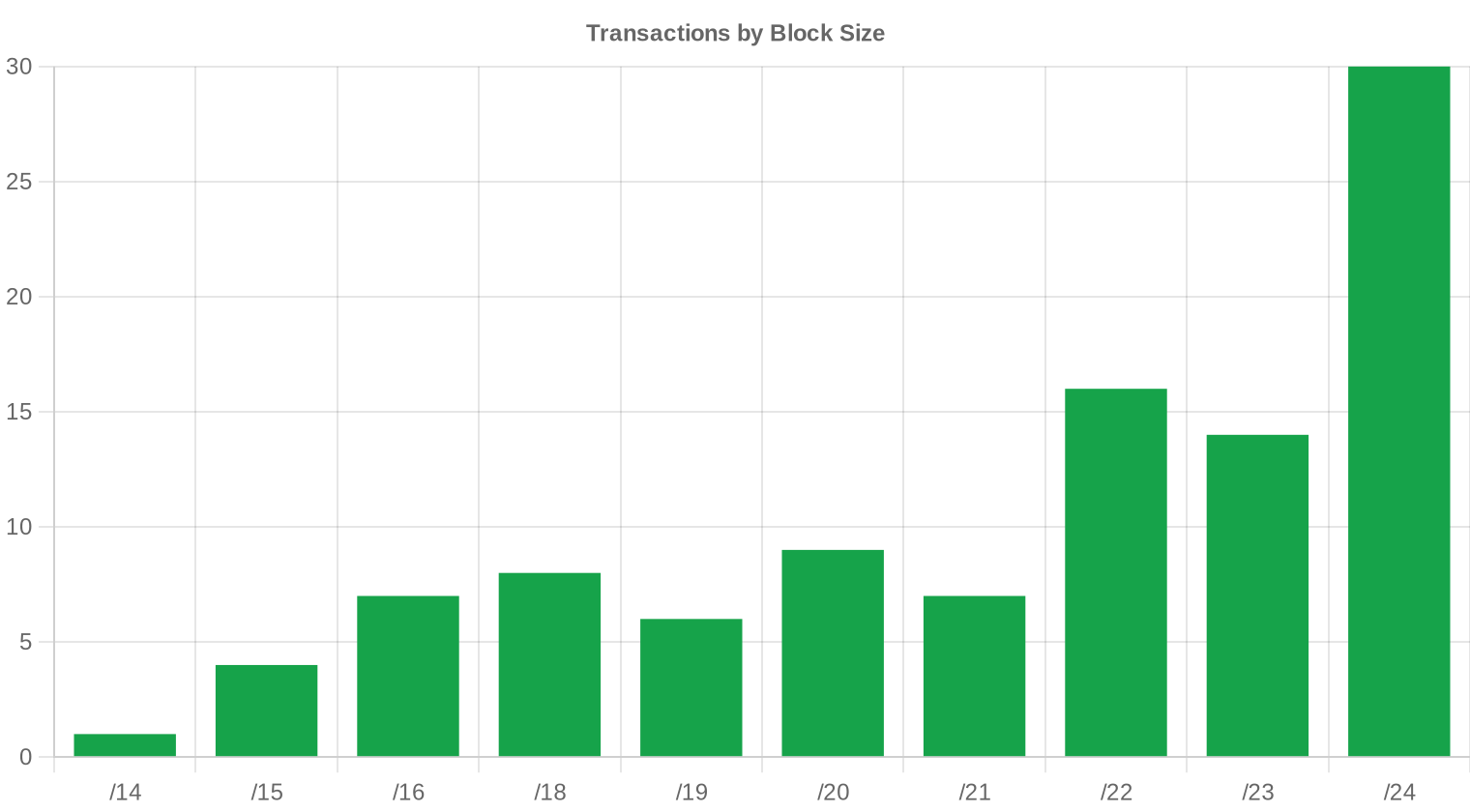

/24 blocks were the most traded prefix size at 30 transactions, consistent with the structural reality that small operators and enterprises still need minimum-viable allocations for BGP announceability. The concentration of 67 deals under $50K confirms the retail end of the market remains active even as headline average prices slide. Larger blocks (/16 and above) drove the lion's share of dollar volume — 12 transactions above $1 million accounted for $23.1 million, dwarfing the rest of the book.

Geographic Activity

The United States led with 38 transactions, followed by the United Kingdom at 13 and multi-jurisdiction deals (coded ZZ) at 12. Canada contributed 7 trades, and European buyers from the Netherlands, Ireland, Germany, and Romania rounded out the top tier. The US share reflects both ARIN's dominance in the data and the ongoing absorption of IPv4 space by American cloud, hosting, and broadband providers.Registry Transfer Activity

Total RIR-recorded transfers hit 826 in March, with RIPE accounting for 534 — roughly 64.6% of all transfer activity. ARIN recorded 292 transfers. The gap between RIPE transfer counts and RIPE transaction counts in our pricing data (534 vs. 39) reflects the large number of intra-group and non-market transfers that flow through the RIPE system without a public price attached.Long-Run Transfer Trends

Over the 39-month tracking window, 32,367 total transfers have been recorded across all RIRs. The all-time monthly peak occurred in December 2024, coinciding with year-end portfolio rebalancing and the first wave of post-AWS-charge selloffs. RIPE has consistently claimed the majority share at 59.7% of cumulative transfers versus ARIN's 40.3%, a ratio that has held steady for over two years.| RIR | RIR Transfers |

|---|---|

| RIPE | 19,329 |

| ARIN | 13,038 |

| RIR Transfers | 32,367 |

Outlook & Forecast

Forecasting each block-size band and RIR separately with our AI model:

The overall average price per IP is projected to reach $16.23 by December 2026, with a next-month estimate of $18.25 per IP.

- RIPE: projected at $21.00 per IP next month, trending toward $18.50 by December 2026.

- ARIN: projected at $16.00 per IP next month, trending toward $13.00 by December 2026.

- APNIC: projected at $19.50 per IP next month, trending toward $16.50 by December 2026.

- LACNIC: projected at $26.00 per IP next month, trending toward $24.00 by December 2026.

- AFRINIC: insufficient data for a reliable forecast.

Forecast by Block Size

| Block | Current $/IP | Next Month | Year-End | Confidence |

|---|---|---|---|---|

| /24 | $25.00 | $24.50 (-2.0%) | $22.00 (-12.0%) | medium |

| /23 | $19.00 | $18.50 (-2.6%) | $16.50 (-13.2%) | medium |

| /22 | $18.48 | $18.00 (-2.6%) | $15.50 (-16.1%) | medium |

| /21 | $16.25 | $15.50 (-4.6%) | $13.50 (-16.9%) | medium |

| /20 | $15.75 | $15.00 (-4.8%) | $13.50 (-14.3%) | low |

| /19 | $14.00 | $13.50 (-3.6%) | $12.00 (-14.3%) | low |

| /18-/16 | $10.80 | $10.50 (-2.8%) | $9.50 (-12.0%) | low |

| /15-up | $9.00 | $8.50 (-5.6%) | $7.50 (-16.7%) | low |

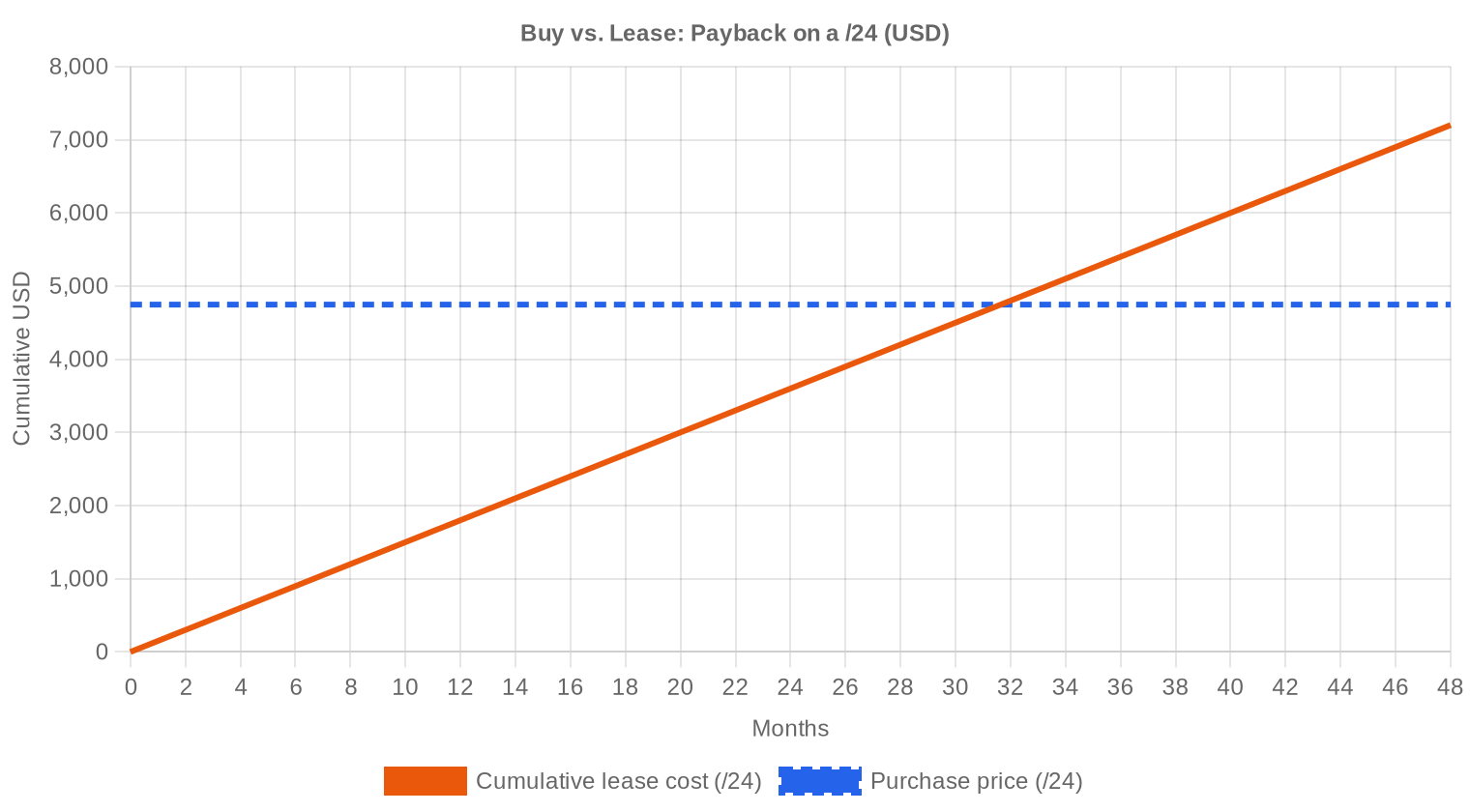

Editor's Take: Buy vs. Lease

The buy-versus-lease calculus strongly favors purchasing at current prices. At $18.54 per IP and a prevailing lease rate of $0.5859 per IP per month, the breakeven sits at just 31.6 months — under 2.6 years. That's a 37.9% implied annual yield for block holders leasing out their space, and a clear signal that lessees paying market rates will overshoot the purchase price quickly. A /24 block runs $4,746 to buy versus $150 per month to lease; anyone planning to hold addresses for three or more years should be buying outright. The exception is short-duration projects or compliance-sensitive deployments where lease flexibility matters more than cost. For sellers sitting on unleased blocks, the math is straightforward: lease them today at current yields or sell before prices erode further toward the $16 year-end target.| /24 Purchase price | $4,746 |

| /24 Lease price | $150 / mo |

| Payback period | 31.6 mo (2.6 yr) |

| Gross annual yield | 37.9% |

What This Means for You

Buyers: You are in the strongest negotiating position this market has offered since 2019. Average prices are 43.5% below last March. If you need space for 3+ years, buy now — the lease breakeven at 31.6 months makes outright acquisition the obvious play. Push hard on ARIN blocks where the average is just $16.Sellers: The bid is falling and the model points to $16.23 by December. If you have clean, transferable blocks, bring them to market before further erosion. Smaller blocks (/24s) still command per-IP premiums but volume is thin. Consider partial sales to manage exposure.

Lessees: Monthly lease rates of $0.59 per IP — or $150 per /24 — look expensive relative to purchase prices. Re-evaluate your lease commitments. Unless your use case is genuinely temporary, converting to ownership saves money within three years.

Block holders: The 37.9% annualized yield from leasing is attractive, but it assumes sustained tenant demand. Lock in longer lease terms where possible — the purchase price your tenants face is dropping, which puts downward pressure on lease rates over time.

Browse verified IPv4 blocksSell IPv4 →

List your blocks with managed transferLease IPv4 →

Flexible short-term capacityLease Out IPv4 →

Turn idle blocks into recurring revenue

IPv4 Pricing by Block Size

/24 blocks carry a meaningful per-IP premium, often 30-50% above the cost per IP in a /20 or larger. The max price in March was $34 per IP, almost certainly from a small RIPE /24. At the other end, bulk ARIN trades cleared at $9 — a level that would have been unthinkable 18 months ago. The spread between small and large blocks continues to widen as supply at the retail end stays tighter.| Block | IPs | Buy: /IP | Buy: Total | Lease: /IP/mo | Lease: Monthly |

|---|---|---|---|---|---|

| /24 | 256 | $35–45 | $8,960–11,520 | $0.38–0.50 | $97–128 |

| /22 | 1,024 | $28–38 | $28,672–38,912 | $0.33–0.45 | $338–461 |

| /20 | 4,096 | $22–32 | $90,112–131,072 | $0.30–0.40 | $1,229–1,638 |

| /18 | 16,384 | $20–30 | $327,680–491,520 | $0.30–0.38 | $4,915–6,226 |

| /16 | 65,536 | $18–28 | $1,179,648–1,835,008 | $0.30–0.35 | $19,661–22,938 |

IPv4 Price History: 2011–2026

IPv4 addresses first acquired monetary value following IANA free pool exhaustion in 2011, when early trades cleared at $5-7 per IP. Prices climbed steadily through the 2010s, accelerated during the pandemic-era connectivity boom, and peaked near $55-60 in late 2023 and early 2024. AWS's decision to charge $0.005/hour for public IPv4 — effective February 2024 — triggered the most significant repricing event in the market's history, freeing millions of addresses as cloud tenants dropped elastic IPs they didn't need. The resulting 43.5% year-over-year decline captured in this report is the tail end of that structural adjustment, and the market is still searching for a new equilibrium.| Year | ~Price/IP | Key Event |

|---|---|---|

| 2011 | $7–12 | IANA free pool exhausted; Microsoft/Nortel deal ($11.25/IP) |

| 2012 | $8–12 | RIPE NCC reaches last /8; begins /22-only allocation |

| 2014 | $10–15 | LACNIC free pool exhausted |

| 2015 | $8–15 | ARIN free pool exhausted |

| 2017–18 | $12–18 | Leasing market grows; cloud demand rises |

| 2019 | $18–24 | RIPE NCC exhausts remaining free pool |

| 2021–22 | $50–60+ | Post-pandemic peak; hyperscaler build-outs |

| 2024 | $35–52 | AWS IPv4 charge ($0.005/IP/hr); large block correction |

| 2025–26 | $18–45 | Market bifurcation; /16s below $20 for first time since 2019 |

Market Structure: Who Is Buying & Selling

The buy side is increasingly dominated by mid-tier ISPs, hosting companies, and enterprise IT departments that need routable space for specific deployments. Hyperscaler demand has cooled as the major cloud providers rationalized their own holdings post-AWS charge. On the sell side, legacy corporate holders — banks, universities, government agencies — continue to monetize allocations they received in the 1990s, often through broker-facilitated transactions that generate six- and seven-figure windfalls.IPv4 vs. Other Asset Classes

At a 37.9% annualized lease yield, IPv4 blocks outperform virtually every conventional asset class on a current-income basis. Ten-year Treasuries sit around 4.5%, investment-grade corporate bonds near 5.5%, and even high-yield real estate REITs top out around 8-10%. The catch is depreciation risk: if purchase prices continue toward $16.23, the capital loss partially offsets that lease income. Still, on a total-return basis, IPv4 blocks purchased at $18.54 and leased at current rates would need to depreciate below $11 within a year to underperform a 5% bond — an unlikely scenario given current demand floors.| Asset Class | Typical Yield | Liquidity | Primary Risk |

|---|---|---|---|

| IPv4 | 37.9% | Moderate | IPv6 adoption, block quality |

| Commercial Real Estate | 5–8% | Low | Vacancy, rate cycle |

| Investment-Grade Bonds | 4–5% | High | Duration, credit risk |

| S&P 500 | ~1,3% | High | Market volatility |

| Money Market / T-Bills | ~4–5% | High | Rate cycle changes |

IPv6 Adoption & Why IPv4 Remains Essential

IPv6 adoption continues to grow — Google's measurements show roughly 45% of global traffic reaching their services over IPv6 — but the protocol transition has been grinding on for over a decade with no endpoint in sight. Carrier-grade NAT and dual-stack deployments keep IPv4 functional for the vast majority of networks. The practical reality is multi-year coexistence, and any organization deploying public-facing infrastructure in 2026 still needs routable IPv4 space.AI & Cloud Infrastructure Demand

AI infrastructure buildouts — both training clusters and inference endpoints — require public-facing IPv4 addresses for API access, model serving, and monitoring. The wave of GPU cloud startups and enterprise AI deployments has created a new category of demand that didn't exist at scale two years ago. This demand is concentrated in ARIN space (US-based data centers) and partially explains why ARIN transaction counts remain elevated even as prices fall — buyers are absorbing more addresses at lower prices.What Determines IPv4 Block Value

Clean blocks — those with no history on Spamhaus, SORBS, or other major blacklists — command 15-25% premiums over blocks with any reputation issues. Allocation vintage matters less than transferability and subnet flexibility: a /20 from a legacy holder with clean WHOIS history will clear faster and higher than a recently fragmented /20 from an ISP. RIR jurisdiction also drives value, with LACNIC blocks fetching nearly 40% above market due to acute scarcity.Sell vs. Lease: A Decision Framework

At $18.54 per IP and declining, holders who believe the year-end forecast of $16.23 face a 12.4% capital haircut by waiting. Selling now locks in value, while leasing at $0.59 per IP per month generates $7.03 annually — a 37.9% yield that compensates for depreciation unless the price decline accelerates well beyond projections. Holders with clean, demand-generating blocks should lease; holders sitting on idle, unreputated inventory should sell before the bid erodes further.| /24 Purchase price | $4,746 |

| /24 Lease price | $150 / mo |

| Payback period | 31.6 mo (2.6 yr) |

| Gross annual yield | 37.9% |

RIPE NCC 24-Month Transfer Restriction

RIPE NCC's 24-month holding requirement continues to function as an artificial supply brake. Any block transferred into a new holder's account cannot be resold for two years, which removes a significant fraction of RIPE inventory from the tradeable float at any given time. This rule is the single largest driver of the $5.30 per-IP premium that RIPE blocks command over ARIN equivalents — buyers pay more because supply is structurally constrained.Deal Size Distribution

Average deal size jumped to 158,102 addresses in March, up 47% from February's 107,589 and 80% above the year-ago figure of 87,854. This is a bulk-market story: 12 deals over $1 million accounted for $23.1 million in value, while 67 sub-$50K deals totaled just $845K. The middle tiers — $50K-$250K (15 deals) and $250K-$1M (8 deals) — filled in the distribution but didn't drive the headline numbers. The skew toward large deals is consistent with institutional buyers taking advantage of lower prices to build positions.Top Trading Countries

The US accounted for 38 of 102 transactions, reflecting both ARIN's market share and the depth of American demand from cloud, hosting, and broadband operators. The UK's 13 deals make it the clear European leader, likely driven by London-headquartered ISPs and hosting firms. Canada's 7 deals and the Netherlands' 4 round out the top tier — the Dutch figure punches above the country's size, consistent with Amsterdam's role as a major peering and data center hub.BEAD Broadband Program Impact

The $42.45 billion BEAD broadband program is entering its deployment phase, and rural ISPs drawing down these grants will need routable IPv4 space — primarily /20 to /22 blocks — for subscriber management. This demand is slow-moving but persistent, and it targets exactly the mid-size ARIN blocks that have been the most liquid part of the market. As BEAD-funded networks come online through 2027, expect a tightening in this segment even as overall prices continue to soften.Hyperscaler IPv4 Holdings

Amazon, Microsoft, and Google collectively hold an estimated 120-140 million IPv4 addresses. Amazon's 2024 public IPv4 charge shook loose millions of addresses that tenants had reserved but didn't use — the downstream effect is still visible in the 43.5% year-over-year price decline. Microsoft and Google have been quieter, but both are believed to have selectively sold smaller blocks from legacy acquisitions. Any decision by a hyperscaler to monetize a /8 or equivalent would move the market by several dollars per IP overnight.Macroeconomic Conditions & Market Impact

Enterprise IT budgets remain under pressure from elevated interest rates, which raises the cost of capital for infrastructure investments including IPv4 acquisitions. The flip side: lower IPv4 prices partially offset tighter budgets, keeping transaction volume resilient even as per-unit pricing falls. If the Fed begins cutting rates later in 2026, we could see deferred purchases accelerate — a potential source of demand stabilization in the back half of the year.Model Update & Calibration

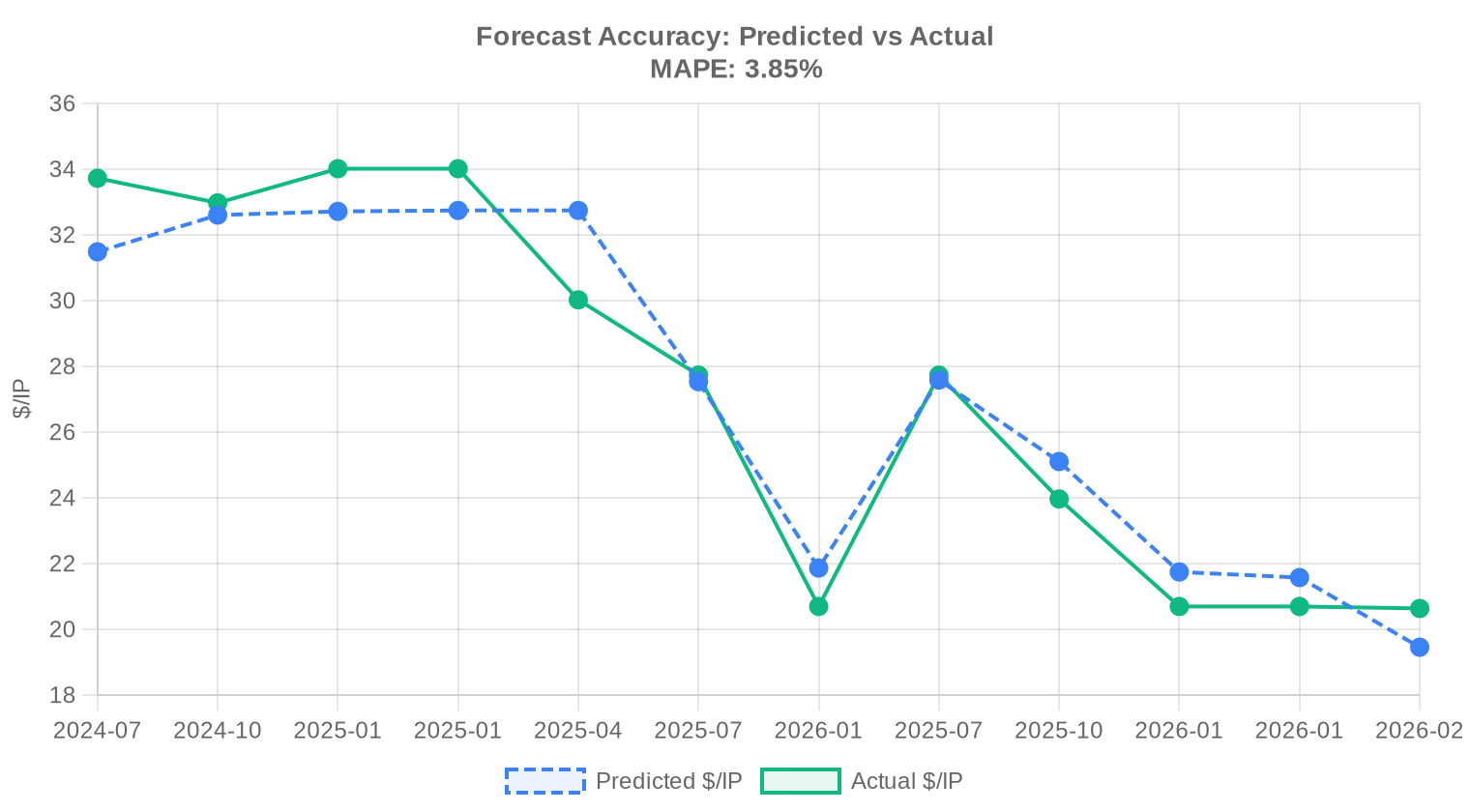

We reviewed our past projections against actual market outcomes and recalibrated the model for this report. The updated model places more weight on recent price movements using exponential decay, dynamically adjusts prediction bands to reflect current market conditions, and corrects for any systematic bias detected in earlier forecasts. The predicted-vs-actual comparison chart below shows how closely our past estimates tracked reality.

| Report Period | Target Month | Predicted | Actual | Deviation |

|---|---|---|---|---|

| 2025 | 2026-01 | $22 | $21 | +6% |

| 2025-Q2 | 2025-07 | $28 | $28 | -1% |

| 2025-Q3 | 2025-10 | $25 | $24 | +5% |

| 2025-H2 | 2026-01 | $22 | $21 | +5% |

| 2025-Q4 | 2026-01 | $22 | $21 | +4% |

| 2026-01 | 2026-02 | $19 | $21 | -6% |

Methodology

Figures are based on completed IPv4Center marketplace transactions and RIR transfer statistics. Prices are in US dollars per IP address. Forecasts are produced by an AI model that analyses each block-size band and RIR segment separately (with outlier-trimmed medians) alongside known market catalysts; they are estimates, not guarantees.

Data Sources

- Hilco Streambank — Completed auction transaction records

- RIPE NCC — Inter-RIR and intra-RIR transfer statistics

- ARIN — North American transfer reports and waiting list data

- APNIC — Asia-Pacific transfer records

- LACNIC — Latin American and Caribbean transfer data

- IPv4Center.com — Proprietary marketplace transaction and lease pricing data

This report is generated automatically for informational purposes only and does not constitute financial advice.

Frequently Asked Questions

What was the average price per IPv4 address in March 2026?

The global weighted average landed at .54 per IP, with a median of .58 — remarkably tight dispersion that suggests a liquid, well-arbitraged market. This represents a 1.41% decline from the prior period, consistent with the broader downtrend we've been tracking.

How many transactions closed in March 2026 and what was the total market value?

We recorded 102 completed transactions covering approximately 1.51 million addresses for a combined market value of .13 million. The average deal size was roughly 158,100 IPs, indicating the month was dominated by a handful of large-block trades pulling the mean well above the median.

Why is there such a wide spread between the minimum () and maximum () price per IP?

Block size, RIR jurisdiction, and counterparty urgency explain the bulk of the spread. Sub-/24 fragments and large ARIN blocks routinely clear in single digits to mid-teens, while small RIPE and LACNIC blocks — where supply is structurally tighter — can command north of . A 3.8× min-to-max ratio is actually narrower than what we observed through much of 2024–2025.

Which RIR region had the most transaction volume in March 2026?

ARIN accounted for 54.9% of total IPs transacted — 56 deals moving roughly 1.11 million addresses worth .34 million. North America remains the deepest pool of available inventory, and the average ARIN price of .00 per IP is the lowest across all active regions, which continues to attract bulk buyers.

Why are RIPE addresses priced at a premium to ARIN?

RIPE averaged .30 per IP versus ARIN's .00 — a 33% premium. Free-pool exhaustion hit RIPE earlier, the European regulatory environment adds transfer friction, and RIPE blocks tend to trade in smaller denominations (39 transactions for only 382K IPs). Scarcity plus fragmentation equals higher clearing prices.

What is driving LACNIC to be the priciest region at .88 per IP?

LACNIC posted the highest average price on just 4 transactions covering 5,632 addresses. The Latin American market is extremely thin — virtually no secondary supply pipeline — so any buyer with a legitimate need faces classic small-market illiquidity. The median of .25 and a ceiling of .00 confirm this is a seller's market in that region.

Were there any AFRINIC transactions in March 2026?

Zero. AFRINIC has been effectively frozen for transfer purposes for an extended period due to ongoing governance and policy disputes. We do not model any near-term resumption of activity in that region.

What was the most commonly traded prefix size?

/24 blocks led the count with 30 transactions, which is unsurprising — a /24 (256 IPs) is the minimum globally routable block and serves as the market's retail unit. Buyers seeking quick, no-hassle deployments continue to favor this size.

Which countries were the most active buyers?

The United States dominated with 38 transactions, followed by the United Kingdom (13) and a notable cohort of 12 transactions with unresolved or multinational jurisdiction codes. Canada contributed 7 deals. The top three geographies account for roughly 62% of all recorded trades.

How does the buy-vs-lease analysis shake out at current March 2026 rates?

At .54 per IP purchase price versus .5859 monthly lease cost, the breakeven is 31.6 months — roughly 2.6 years. Our verdict is buy. Purchasers who expect to hold addresses beyond that horizon are better off owning outright, and the implied annual yield of 37.9% makes leasing an expensive form of financing.

What does the current lease market look like?

Based on 44 sampled lease contracts, the prevailing rate is .59 per IP per month, or about 0 per /24 per month (.03 per IP annualized). Lease data is most robust for RIPE addresses; ARIN lease pricing remains opaque in public datasets. Leasing remains attractive for short-duration projects under 2.6 years.

What is the price forecast for the remainder of 2026?

Our model — which we flag as reliable for this dataset — projects the average to slip to .25 next month and to .23 by December 2026. That implies roughly a 12.5% decline from March levels over nine months. The trend is unambiguously down.

What are the risks of buying IPv4 addresses at current prices given the downward trend?

The primary risk is asset depreciation. If our year-end forecast of .23 holds, a buyer paying today's .54 faces a ~12.5% mark-to-market loss by December. Buyers should stress-test their hold period assumptions and consider whether leasing — despite its higher running cost — provides superior optionality in a declining market.

What mistakes should be avoided when purchasing large ARIN blocks?

The most common error is overpaying relative to the median. ARIN's median was .25 in March, yet maximum prints reached — a 60% premium. Buyers who skip competitive bidding or fail to engage a broker with real-time market access routinely leave money on the table. Additionally, neglecting to verify ARIN's needs-based justification requirements can stall or kill a transfer post-LOI.

Is there a risk that IPv6 adoption will materially impair IPv4 values in 2026?

Not imminently. IPv6 adoption continues its glacial crawl, and legacy infrastructure — particularly in North America and Europe — generates persistent demand for IPv4. That said, the secular downtrend in average pricing (our year-end target is .23, down from .54 today) likely reflects the slow gravitational pull of IPv6 transition, among other factors. The risk is real on a 5–10 year horizon.

How did deal-size distribution break down in March 2026?

The market is bifurcated. 67 transactions (66%) were below K, contributing only 5K in value. Meanwhile, 12 deals exceeding M generated .1 million — roughly 5.2× the reported total market value of smaller tiers combined. Institutional-scale trades dominate the value side of the ledger.

What does the 826 total transfer figure represent, and how does it differ from the 102 transactions?

The 826 figure captures all recorded inter-organization transfers across RIRs — including non-market transfers such as M&A-related reassignments and intra-group moves. The 102 transactions represent only those with confirmed market pricing. RIPE led overall transfers with 534, reflecting its high volume of administrative and intra-European moves.

Should buyers target specific RIRs for value in the current market?

ARIN offers the best value at .00 average, and its deep inventory supports negotiating leverage on larger blocks. RIPE at .30 is appropriate for buyers who specifically need European-registry space. APNIC (.37 on only 3 deals) and LACNIC (.88 on 4 deals) are illiquid and expensive — approach with caution and realistic price expectations.

What are the risks of relying on APNIC or LACNIC for IPv4 procurement?

Liquidity risk is paramount. APNIC logged just 3 transactions and LACNIC only 4 in March. At those volumes, a single large buyer can move the market, and execution timelines are unpredictable. Buyers dependent on addresses in these registries should plan procurement cycles months in advance and consider pre-positioned brokers with regional inventory.

How long does a typical IPv4 transfer take to complete?

ARIN transfers generally close in 30–60 days, contingent on needs-based justification review. RIPE transfers are faster — often 2–4 weeks — given the absence of a justification requirement for transfers. APNIC and LACNIC timelines are less standardized and can stretch to 90+ days depending on registry workload and documentation.

What is the implied annual yield for IPv4 address holders who lease their inventory?

At a purchase cost of .54 and a lease rate of .5859/month (.03 annualized), the implied gross yield is 37.9%. That is extraordinarily attractive on paper, though it assumes full occupancy and no depreciation in the underlying asset — assumptions that are increasingly aggressive given the downward price trend.

What would make the current downtrend reverse?

A reversal would require a demand shock — perhaps a large-scale cloud buildout, a geopolitical event restricting cross-border transfers, or a sudden tightening of ARIN supply through policy changes. None of these scenarios is our base case. The structural forces — IPv6 migration, efficiency gains in address usage, and steady secondary-market supply from legacy holders — favor continued, gradual price erosion.

Is it a mistake to wait for lower prices before buying?

It depends on your deployment timeline. Our model projects .23 by December 2026, which could save roughly .31 per IP versus today's price — meaningful on a /16 (65,536 IPs, or ~1K in savings). But if you need addresses for revenue-generating infrastructure now, the opportunity cost of delayed deployment almost certainly exceeds the potential purchase discount. Timing the bottom is a fool's errand in any market.

How has the total transfer volume across RIRs shifted historically?

Over the trailing 39-month window, RIPE accounts for 59.7% of all recorded transfers and ARIN 40.3%, with APNIC, LACNIC, and AFRINIC contributing effectively zero. The cumulative transfer count reached 32,367 over that window, peaking in December 2024. RIPE's dominance in transfer count (versus ARIN's dominance in IP volume) reflects the fragmented European market with many smaller-block moves.

What does the tight spread between mean (.54) and median (.58) tell us about market health?

A mean-median differential of just .04 signals a near-symmetric price distribution with minimal skew from outlier trades. This is the hallmark of a mature, efficiently priced market. Contrast this with LACNIC, where the mean (.88) and median (.25) also track closely but on a much thinner sample — tight spreads there reflect low volume, not deep liquidity.