15 min read

This report analyzes the IPv4 transfer market for First Half 2024, based on completed IPv4Center marketplace transactions and official RIR transfer records.

Executive Summary

The IPv4 transfer market moved 641,792 addresses across 343 transactions in the first half of 2024, generating $21.8 million in total transaction value. The average price per IP landed at $33.22, down 6.1% from the $35.38 average recorded in the second half of 2023 and off 19.2% year-over-year versus H1 2023. The median price of $32.50 sat slightly below the mean, suggesting a distribution skewed by a handful of premium ARIN transactions at the top end. Transaction volume rose 6.2% from the prior half, meaning more deals got done — just at lower prices. The trend remains firmly downward, with prices declining for a third consecutive period.Market Overview

| Transactions | 343 |

| IP Addresses Traded | 641,792 |

| Estimated Market Value | $21,813,123 |

| Average Price / IP | $33.22 |

| Median Price / IP | $32.50 |

| RIR Transfers | 5,171 |

Year-over-Year Comparison

| Metric | This period | A year earlier (H1 2023) | Change |

|---|---|---|---|

| Transactions | 343 | 220 | +55.9% |

| IP Addresses Traded | 641,792 | 779,520 | -17.7% |

| Estimated Market Value | $21,813,123 | $36,390,182 | -40.1% |

| Average Price / IP | $33.22 | $41.09 | -19.2% |

| RIR Transfers | 5,171 | 4,282 | +20.8% |

Price Dynamics

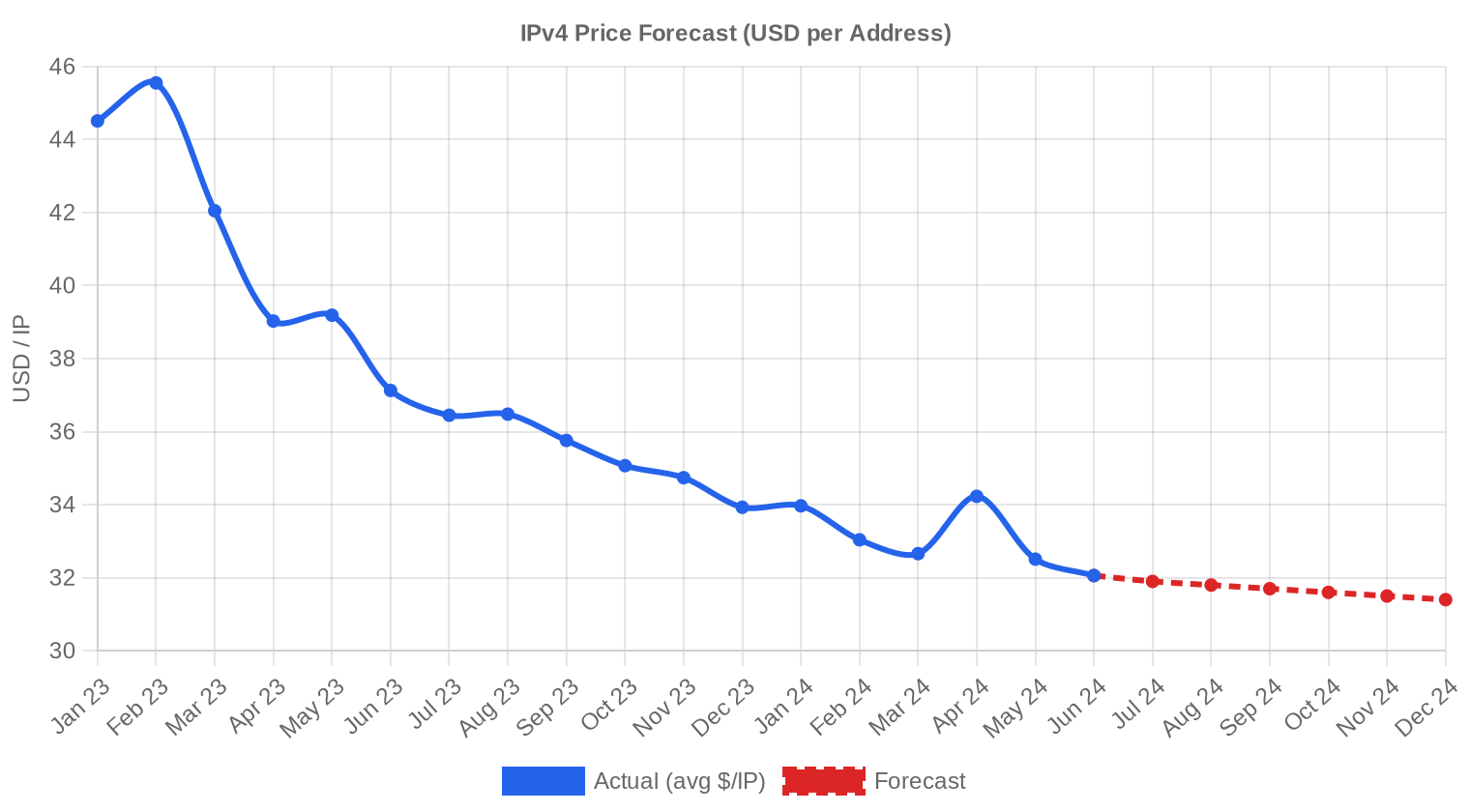

The pricing range in H1 2024 ran from a floor of $26/IP to a ceiling of $50.12/IP — a $24.12 spread that reflects persistent fragmentation between distressed inventory and premium clean blocks. That high watermark of $50.12 came out of APNIC, while ARIN produced the bulk of transactions above $40. The 6.1% half-over-half decline and 19.2% annual drop are impossible to dismiss as noise; this is a market repricing. The regression line points to further softening — our model projects $31.61 next month and $31.40 by December. Sellers who waited for a bounce through the first half didn't get one, and the data doesn't suggest they'll get one in the second half either.

Pricing by RIR

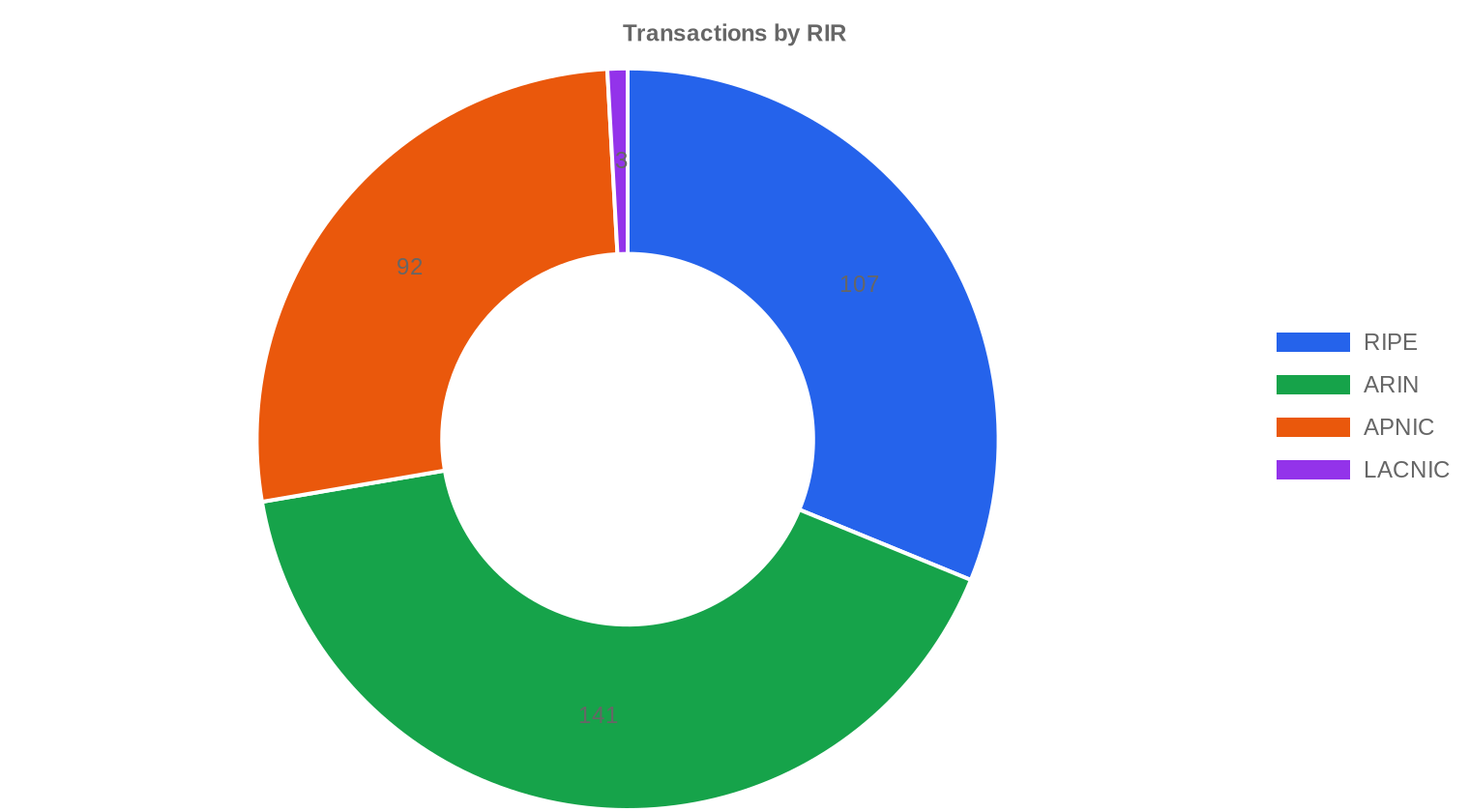

ARIN continues to command the highest per-IP pricing in the market, and it isn't close. At $35.11 average across 141 transactions, ARIN blocks carry a $2.99 premium over RIPE and a $3.44 premium over APNIC — roughly a 10% surcharge that reflects the relative ease of ARIN transfers and strong US-based demand. RIPE settled at $32.12 average on 107 deals, a solid middle ground considering the 24-month holding rule that constrains speculative flipping. APNIC came in at $31.67 across 92 transactions, with the widest max-min spread of any RIR ($27 to $50.12), pointing to highly variable block quality. LACNIC barely registered — just 3 transactions at $31.33 average. AFRINIC recorded zero transactions.ARIN: $35.11/IP across 141 transactions (41.1% of volume).

RIPE NCC: $32.12/IP across 107 transactions (26.7% of volume).

APNIC: $31.67/IP across 92 transactions (30.1% of volume).

LACNIC: $31.33/IP across 3 transactions (1.8% of volume).

AFRINIC: No recorded transactions.

| RIR | Transactions | Avg $/IP | Median $/IP | IPs Traded | RIR Transfers | Next Month (proj.) | Year-End (proj.) |

|---|---|---|---|---|---|---|---|

| RIPE | 107 | $32.12 | $32.00 | 171,264 | 3,383 | $32.50 | $32.00 |

| ARIN | 141 | $35.11 | $35.00 | 266,240 | 1,788 | $33.00 | $33.50 |

| APNIC | 92 | $31.67 | $30.50 | 193,024 | 0 | $29.00 | $28.50 |

| LACNIC | 3 | $31.33 | $30.00 | 11,264 | 0 | $29.50 | $28.00 |

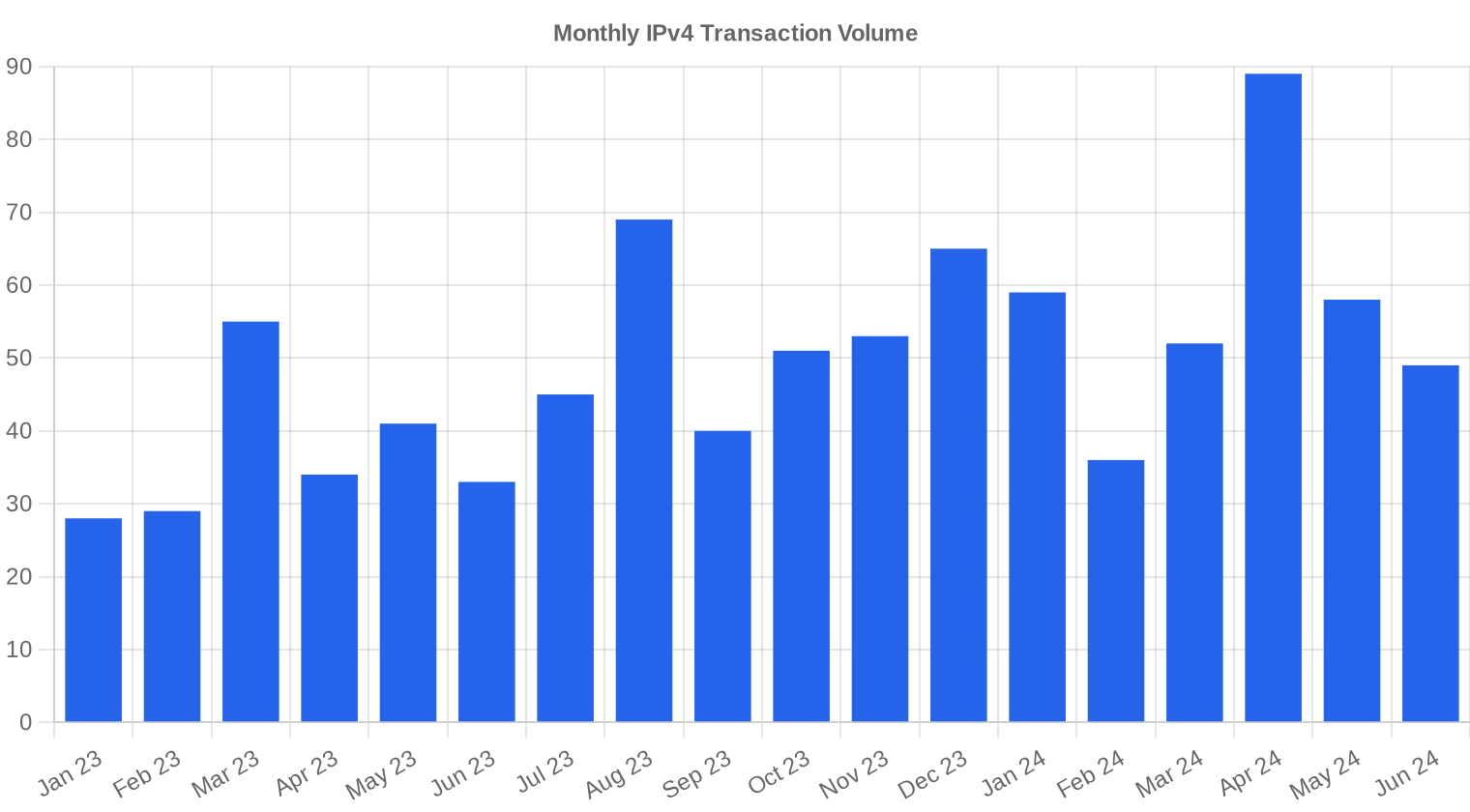

Transaction Volume

Supply & Block Sizes

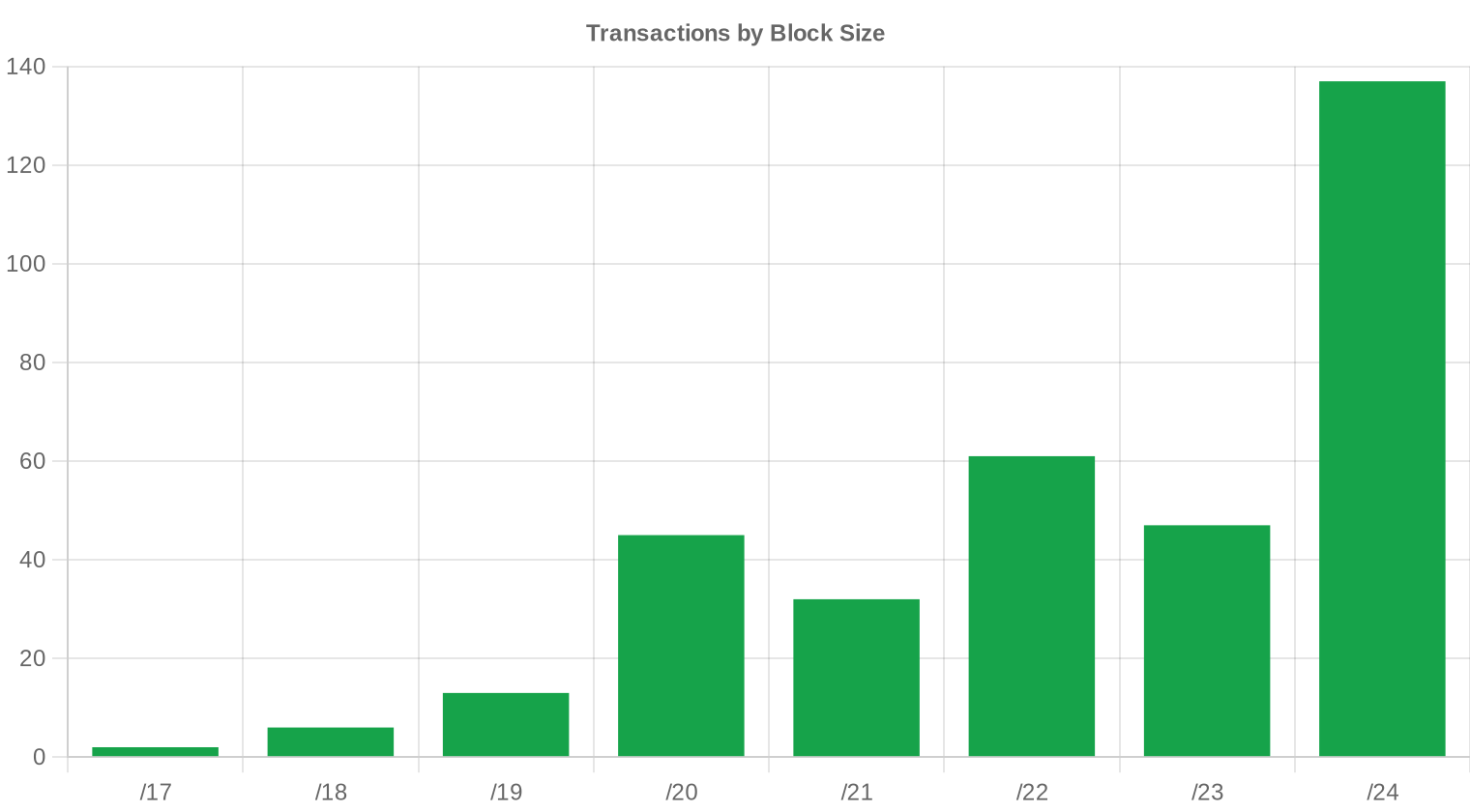

The /24 block dominated deal flow again, accounting for 137 of 343 transactions — roughly 40% of all deals. This is the workhorse block for small and mid-size operators who need a routeable allocation without the capital outlay of a /20 or larger. The gravitational pull toward smaller blocks shows up in the average deal size, which collapsed to 63,595 IPs from 103,959 in H2 2023 and 165,410 in H1 2023 — a 61.5% decline year-over-year that signals a structural shift in buyer profiles toward smaller purchasers.

Geographic Activity

Country-level transaction data was not reported for this period, limiting geographic granularity. Based on RIR distribution, North American demand (ARIN at 41.1% of volume) drove the plurality of activity, with European and Asia-Pacific markets splitting the remainder roughly evenly. The absence of AFRINIC transactions for a second consecutive period underscores the governance and transfer-policy challenges that continue to freeze that market.Registry Transfer Activity

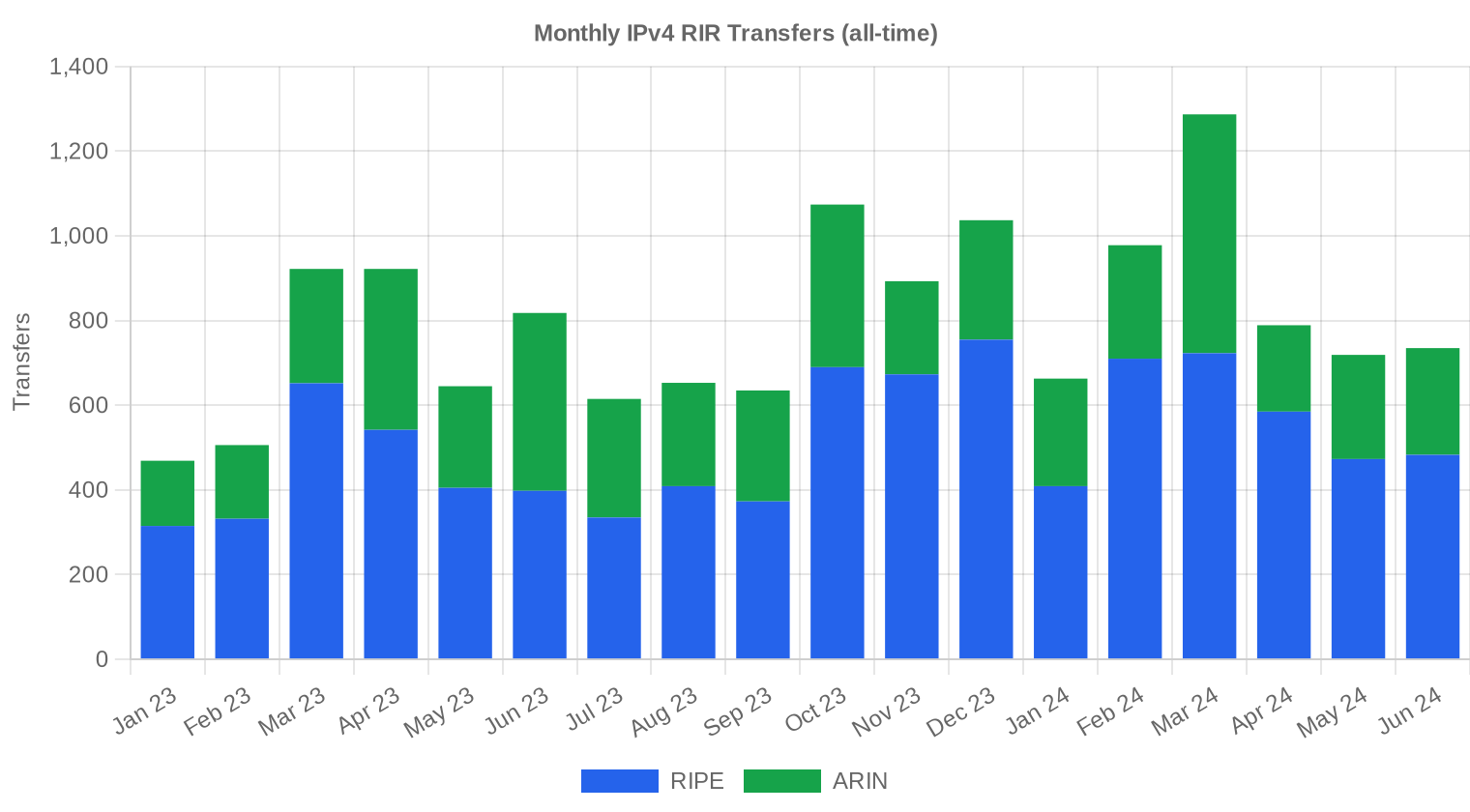

Official RIR transfer registries logged 5,171 transfers during H1 2024 — a figure that includes both market-based sales and intra-organizational moves. RIPE led with 3,383 recorded transfers, accounting for 65.4% of total transfer activity, versus ARIN's 1,788 (34.6%). The gap between RIPE's transfer volume and its share of priced transactions (only 31.2% of our tracked deals) suggests a significant portion of RIPE transfers are non-market reorganizations or below our reporting threshold.Long-Run Transfer Trends

Over the trailing 18 months, the transfer registries have recorded 14,360 total transfers across ARIN and RIPE. Activity peaked in March 2024, which aligned with Q1 budget deployments and the tail end of several large enterprise procurement cycles. RIPE accounted for 64.5% of the 18-month transfer total versus ARIN's 35.5%, a ratio that has been stable for several quarters and reflects RIPE's larger and more fragmented holder base.| RIR | RIR Transfers |

|---|---|

| RIPE | 9,262 |

| ARIN | 5,098 |

| RIR Transfers | 14,360 |

Outlook & Forecast

Forecasting each block-size band and RIR separately with our AI model:

The overall average price per IP is projected to reach $31.40 by December 2024, with a next-month estimate of $31.61 per IP.

- RIPE: projected at $32.50 per IP next month, trending toward $32.00 by December 2024.

- ARIN: projected at $33.00 per IP next month, trending toward $33.50 by December 2024.

- APNIC: projected at $29.00 per IP next month, trending toward $28.50 by December 2024.

- LACNIC: projected at $29.50 per IP next month, trending toward $28.00 by December 2024.

- AFRINIC: insufficient data for a reliable forecast.

Forecast by Block Size

| Block | Current $/IP | Next Month | Year-End | Confidence |

|---|---|---|---|---|

| /24 | $30.75 | $31.00 (+0.8%) | $30.00 (-2.4%) | medium |

| /23 | $32.50 | $32.00 (-1.5%) | $31.50 (-3.1%) | medium |

| /22 | $32.50 | $32.50 (0.0%) | $33.00 (+1.5%) | medium |

| /21 | $30.00 | $30.00 (0.0%) | $30.00 (0.0%) | low |

| /20 | $30.84 | $31.00 (+0.5%) | $32.00 (+3.8%) | low |

| /19 | $36.00 | $35.50 (-1.4%) | $36.00 (0.0%) | low |

| /18-/16 | $36.50 | $36.50 (0.0%) | $37.50 (+2.7%) | low |

| /15-up | $51.50 | $50.00 (-2.9%) | $52.00 (+1.0%) | low |

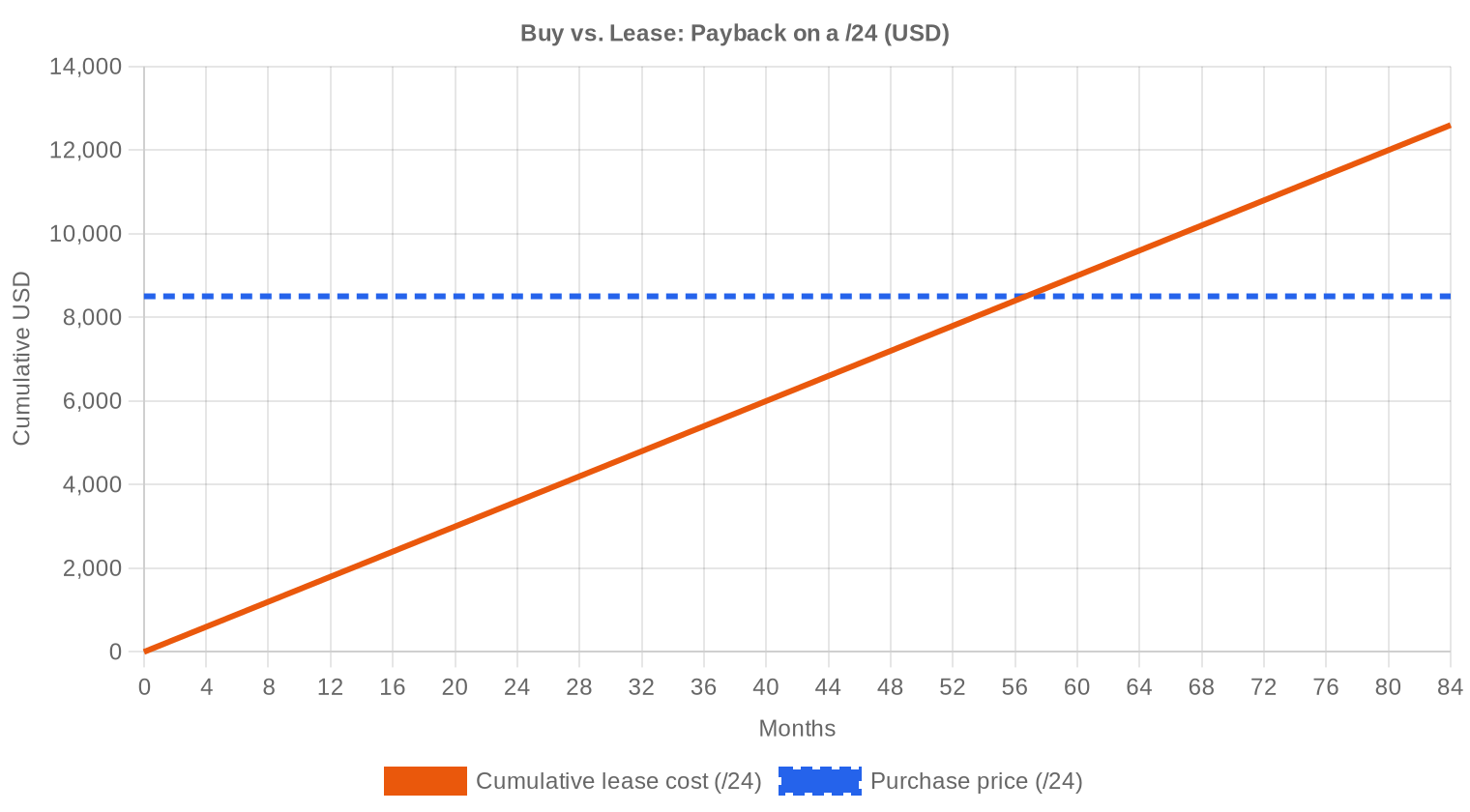

Editor's Take: Buy vs. Lease

The buy-versus-lease calculus shifted further toward buying in H1 2024. At $33.22 per IP purchased and $0.5859 per IP per month in lease costs, the breakeven point sits at 56.7 months — just under 4.7 years. Any operator planning to use addresses beyond that horizon is leaving money on the table by leasing. The implied annual yield on a leased block is 21.2%, which is extraordinary by any asset-class standard and tells you that lease pricing hasn't caught up with the decline in purchase prices. For buyers: the math says buy now and lock in sub-$34 pricing before potential stabilization. For lessors: enjoy the yield while it lasts, because rational tenants will increasingly reach the same conclusion and shift to ownership.| /24 Purchase price | $8,504 |

| /24 Lease price | $150 / mo |

| Payback period | 56.7 mo (4.7 yr) |

| Gross annual yield | 21.2% |

What This Means for You

Buyers: You're operating in a buyer's market for the first time in years. The 19.2% year-over-year price decline gives you real negotiating leverage, particularly on APNIC and RIPE blocks where pricing averages $31–32. If your holding horizon exceeds five years, purchasing outright beats leasing on pure economics. Don't wait for a bottom — the forecast suggests further modest declines, but another $1–2 of downside isn't worth the risk of missing clean inventory.Sellers: The window for $40+ exits on standard blocks is narrowing fast outside of pristine ARIN allocations. If you're sitting on inventory you acquired above $35, the math on holding costs starts to work against you each quarter prices slide. Consider whether partial disposition — selling larger blocks in smaller chunks at the /24 premium — recovers more value than a bulk exit.

Leasers: Monthly rates around $0.59/IP ($150 per /24) remain elevated relative to falling purchase prices. If your address needs are stable and multi-year, the 56.7-month payback period on purchasing versus leasing is a clear signal. Short-term or project-based needs still favor leasing, but run the numbers on anything beyond 2027.

Block Holders: If you're not actively using or monetizing your blocks, the 21.2% implied annual yield from leasing is compelling — but it assumes you can maintain occupancy. As purchase prices fall, tenant churn will increase. Lock in longer lease terms where possible.

Browse verified IPv4 blocksSell IPv4 →

List your blocks with managed transferLease IPv4 →

Flexible short-term capacityLease Out IPv4 →

Turn idle blocks into recurring revenue

IPv4 Pricing by Block Size

The /24 continues to carry a meaningful per-IP premium — small-block buyers consistently pay $34–38 per IP for clean, routeable /24s, versus $28–32 for /20 and larger blocks bought in bulk. This premium has actually widened slightly as average deal sizes shrank 38.8% from H2 2023, concentrating more demand at the small end. For /16 blocks, per-IP pricing drops into the high $20s, but those deals are rare — only 2 transactions exceeded $1 million in H1, totaling $2.18M.| Block | IPs | Buy: /IP | Buy: Total | Lease: /IP/mo | Lease: Monthly |

|---|---|---|---|---|---|

| /24 | 256 | $35–45 | $8,960–11,520 | $0.38–0.50 | $97–128 |

| /22 | 1,024 | $28–38 | $28,672–38,912 | $0.33–0.45 | $338–461 |

| /20 | 4,096 | $22–32 | $90,112–131,072 | $0.30–0.40 | $1,229–1,638 |

| /18 | 16,384 | $20–30 | $327,680–491,520 | $0.30–0.38 | $4,915–6,226 |

| /16 | 65,536 | $18–28 | $1,179,648–1,835,008 | $0.30–0.35 | $19,661–22,938 |

IPv4 Price History: 2011–2026

IPv4 addresses traded near zero when IANA exhaustion hit in 2011. Prices climbed steadily through the 2010s, accelerating past $20/IP by 2019 and peaking near $55–60/IP in late 2022 during a speculative surge fueled by pandemic-era IT expansion and cheap financing. The market cracked in 2023 after AWS began charging $0.005/hour per public IPv4 address — a move that repriced the implicit subsidy hyperscalers had been absorbing and immediately softened demand for purchased blocks. At $33.22, prices have now round-tripped to roughly 2021 levels, and the bifurcation between premium (clean, ARIN, small-block) and commodity (legacy, unclean, large-block) inventory is the defining feature of the current market.| Year | ~Price/IP | Key Event |

|---|---|---|

| 2011 | $7–12 | IANA free pool exhausted; Microsoft/Nortel deal ($11.25/IP) |

| 2012 | $8–12 | RIPE NCC reaches last /8; begins /22-only allocation |

| 2014 | $10–15 | LACNIC free pool exhausted |

| 2015 | $8–15 | ARIN free pool exhausted |

| 2017–18 | $12–18 | Leasing market grows; cloud demand rises |

| 2019 | $18–24 | RIPE NCC exhausts remaining free pool |

| 2021–22 | $50–60+ | Post-pandemic peak; hyperscaler build-outs |

| 2024 | $35–52 | AWS IPv4 charge ($0.005/IP/hr); large block correction |

| 2025–26 | $18–45 | Market bifurcation; /16s below $20 for first time since 2019 |

Market Structure: Who Is Buying & Selling

The buyer side has shifted noticeably toward smaller operators. Average deal size collapsed from 165,410 IPs in H1 2023 to 63,595 in H1 2024 — a 61.5% decline that tells you the hyperscaler and large-ISP procurement wave has largely run its course. On the sell side, legacy holders and corporate restructurings continue to feed supply into the market, aided by IP asset discovery firms that help organizations identify unused allocations. The 245 transactions under $50K (71.4% of all deals) confirm this is increasingly a small-buyer market.IPv4 vs. Other Asset Classes

At a 21.2% implied annual yield from leasing, IPv4 addresses outperform virtually every conventional asset class on a current-income basis. US 10-year Treasuries yield roughly 4.3%, investment-grade commercial real estate cap rates sit around 6–7%, and the S&P 500 dividend yield is under 1.5%. The catch is depreciation risk: prices fell 19.2% year-over-year, which wipes out the yield advantage for anyone who purchased at peak. On a total-return basis, buyers who entered at today's $33.22 and lease the blocks are looking at a genuinely attractive risk-adjusted profile — provided the price floor holds somewhere in the low $30s.| Asset Class | Typical Yield | Liquidity | Primary Risk |

|---|---|---|---|

| IPv4 | 21.2% | Moderate | IPv6 adoption, block quality |

| Commercial Real Estate | 5–8% | Low | Vacancy, rate cycle |

| Investment-Grade Bonds | 4–5% | High | Duration, credit risk |

| S&P 500 | ~1,3% | High | Market volatility |

| Money Market / T-Bills | ~4–5% | High | Rate cycle changes |

IPv6 Adoption & Why IPv4 Remains Essential

IPv6 adoption continues its glacial advance. Google's IPv6 connectivity metrics hover around 43–45% globally, but the distribution is wildly uneven — several major Asian and African markets remain below 10%. The vast majority of enterprise applications, VPN infrastructure, content delivery configurations, and IoT management platforms still require IPv4 reachability. Dual-stack will be the operational reality for at least another decade, and that means IPv4 blocks retain functional value well beyond any theoretical expiration date.AI & Cloud Infrastructure Demand

AI infrastructure buildout is the one bright spot for IPv4 demand growth. Large-scale GPU clusters require routable address space for management planes, inference API endpoints, and data pipeline connectivity — and most organizations provisioning these environments prefer purchased blocks to cloud-provider allocations for latency and control reasons. The effect on aggregate demand is still modest relative to traditional ISP and enterprise consumption, but it's the only buyer category we've seen expand volume quarter-over-quarter through the H1 2024 price decline.What Determines IPv4 Block Value

Not all /24s are created equal. The three factors that most reliably move pricing are blacklist cleanliness (a block with Spamhaus or UCEProtect listings trades at 15–25% discounts), RIR origin (ARIN commands a $3+ premium over APNIC, as the data confirms), and allocation age — older blocks with long, traceable histories are perceived as lower risk. Transferability rules matter too: RIPE's 24-month holding requirement and APNIC's needs-based justification create friction that directly depresses pricing in those registries versus ARIN's comparatively frictionless process.Sell vs. Lease: A Decision Framework

In a declining-price environment, leasing preserves optionality. If you believe prices will stabilize near $31 by year-end (as our model projects), leasing at $0.59/IP/month generates 21.2% annual yield while retaining the option to sell if conditions change. Selling makes sense for holders who acquired blocks below $25 and want to lock in gains, or for organizations that lack the infrastructure to manage lease relationships. The worst position is holding unused blocks without monetizing them — you're absorbing depreciation with no offsetting income.| /24 Purchase price | $8,504 |

| /24 Lease price | $150 / mo |

| Payback period | 56.7 mo (4.7 yr) |

| Gross annual yield | 21.2% |

RIPE NCC 24-Month Transfer Restriction

RIPE NCC's 24-month holding requirement remains the single most impactful policy constraint on European IPv4 supply. Blocks acquired through transfer cannot be re-transferred for two years, which effectively removes speculative intermediaries from the RIPE market and constrains short-term supply. The rule depresses RIPE pricing relative to ARIN (where no such restriction exists) by discouraging buyers who might otherwise pay a premium for quick-flip optionality. For long-term holders, the rule is actually supportive — it reduces speculative competition and stabilizes lease income.Deal Size Distribution

The deal-size distribution in H1 2024 skewed heavily toward small transactions. Of 343 deals, 245 (71.4%) fell under $50K, generating $4.04M in aggregate value. The $50K–$250K band accounted for 77 deals worth $8.3M, while 19 transactions in the $250K–$1M range produced $6.8M. Only 2 deals exceeded $1M, totaling $2.18M. Average deal size of 63,595 IPs is down 38.8% from H2 2023's 103,959 and down 61.5% from H1 2023's 165,410 — a clear trend toward retail-sized procurement.Top Trading Countries

Country-level data was unavailable for this period. The RIR-level breakdown serves as a rough geographic proxy: ARIN's 41.1% share points to sustained North American activity, RIPE's 31.2% reflects steady European demand, and APNIC's 26.8% confirms ongoing Asia-Pacific procurement. The three LACNIC transactions suggest Latin American IPv4 markets remain thin and opaque, constrained by limited broker infrastructure and regional transfer-policy complexity.BEAD Broadband Program Impact

The $42.45 billion BEAD program began issuing subgrants to states in H1 2024, and the IPv4 implications are still ahead of us. As hundreds of small and mid-size ISPs build out last-mile broadband in unserved areas, each will need routeable address space — predominantly /22 through /20 blocks. We expect BEAD-related demand to hit the market in late 2024 through 2026 as construction timelines activate, creating a potential demand floor for mid-size ARIN blocks precisely in the range where pricing has softened most.Hyperscaler IPv4 Holdings

Amazon, Microsoft, and Google collectively control an estimated 100+ million IPv4 addresses — more than many RIRs. AWS's February 2024 enforcement of the $0.005/hour public IPv4 charge continues to reverberate through the market, pushing customers to release unused elastic IPs and reducing net demand for purchased blocks. If any hyperscaler decided to monetize even 5–10% of its holdings through the transfer market, the supply shock would drive prices well below $30. That risk remains the single largest overhang on IPv4 valuations.Macroeconomic Conditions & Market Impact

The Federal Reserve held rates at 5.25–5.50% through H1 2024, keeping cost of capital elevated for debt-financed IP acquisitions. Enterprise IT budgets showed mixed signals — Gartner projected 8% growth in overall IT spending, but much of that flowed to AI and cloud services rather than infrastructure assets like IPv4 blocks. Higher rates also raise the opportunity cost of tying capital up in IP addresses versus risk-free alternatives, which partly explains why deal sizes shrank and buyers concentrated on smaller, operationally necessary purchases rather than speculative accumulation.Model Update & Calibration

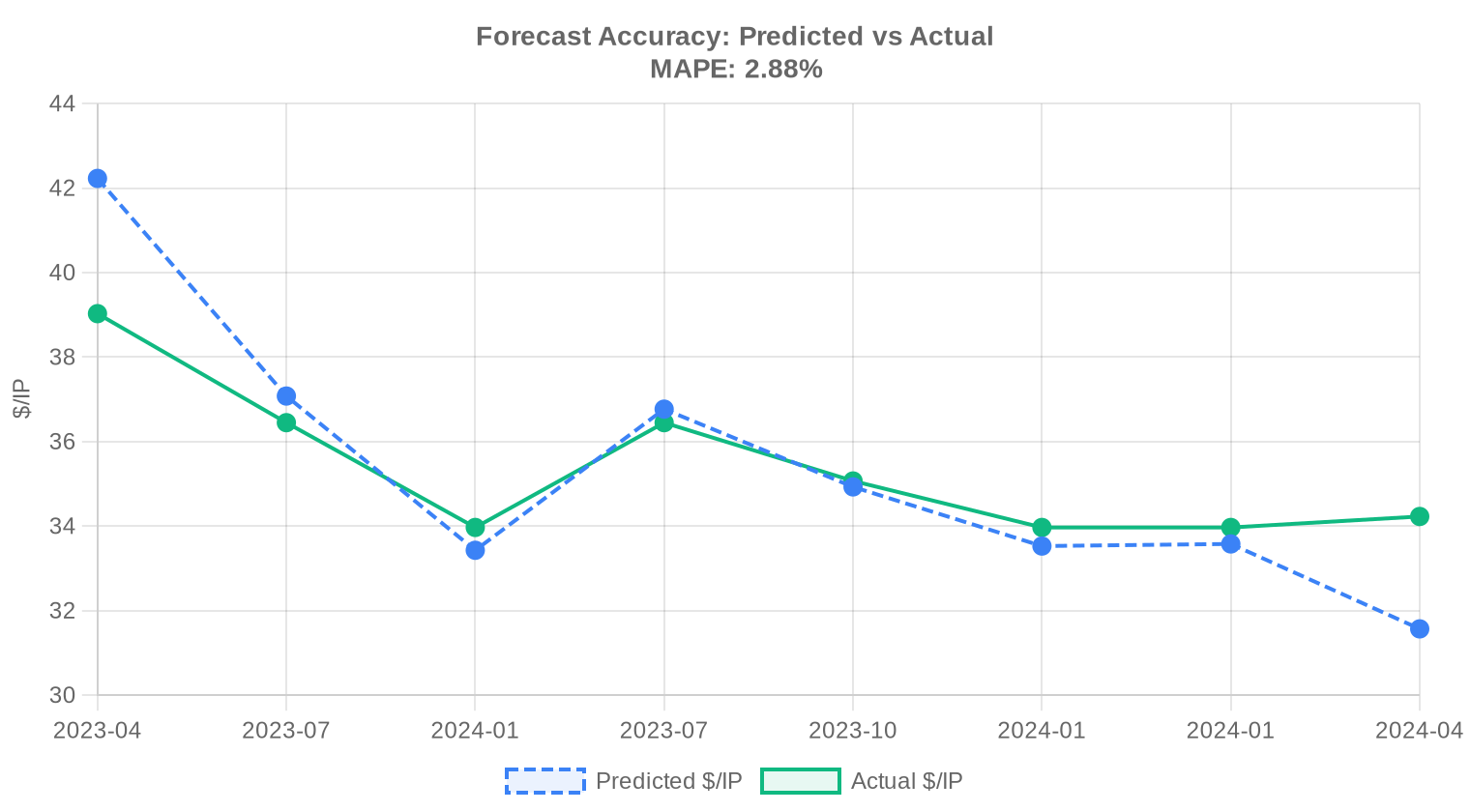

As part of our continuous improvement process, we backtested previous forecasts against realised prices and fine-tuned the model accordingly. Recent months now carry more influence than older data, and the confidence bands have been widened or narrowed based on how well they captured actual outcomes in the past. You can see the full backtest results in the table and chart below.

| Report Period | Target Month | Predicted | Actual | Deviation |

|---|---|---|---|---|

| 2023 | 2024-01 | $33 | $34 | -2% |

| 2023-Q2 | 2023-07 | $37 | $36 | +1% |

| 2023-Q3 | 2023-10 | $35 | $35 | 0% |

| 2023-H2 | 2024-01 | $34 | $34 | -1% |

| 2023-Q4 | 2024-01 | $34 | $34 | -1% |

| 2024-Q1 | 2024-04 | $32 | $34 | -8% |

Methodology

Figures are based on completed IPv4Center marketplace transactions and RIR transfer statistics. Prices are in US dollars per IP address. Forecasts are produced by an AI model that analyses each block-size band and RIR segment separately (with outlier-trimmed medians) alongside known market catalysts; they are estimates, not guarantees.

Data Sources

- Hilco Streambank — Completed auction transaction records

- RIPE NCC — Inter-RIR and intra-RIR transfer statistics

- ARIN — North American transfer reports and waiting list data

- APNIC — Asia-Pacific transfer records

- LACNIC — Latin American and Caribbean transfer data

- IPv4Center.com — Proprietary marketplace transaction and lease pricing data

This report is generated automatically for informational purposes only and does not constitute financial advice.

Frequently Asked Questions

What was the average price per IPv4 address in the first half of 2024?

The global weighted average landed at .22 per address, with a median of .50. That spread is tight enough to suggest a liquid, well-arbitraged market — at least for standard /24 and /16 blocks.

How many IPv4 transfer transactions closed in H1 2024?

We tracked 343 priced transactions covering 641,792 addresses for a combined value of roughly .8 million. The average deal size was approximately 63,595 IPs, though the distribution is heavily right-skewed by a handful of large block trades.

Which RIR region commanded the highest per-IP prices during H1 2024?

ARIN, as usual. ARIN-region addresses averaged .11 per IP with a median of , a meaningful premium over RIPE (.12 average) and APNIC (.67). The premium reflects ARIN's comparatively streamlined transfer policy and deep North American enterprise demand.

Why are ARIN blocks priced roughly per IP above RIPE and APNIC blocks?

North American demand from hyperscalers, cloud providers, and large enterprises keeps ARIN inventory bid. Additionally, ARIN's pre-approval transfer process — while bureaucratic — is well-understood by institutional buyers, which reduces execution risk and supports a premium.

What does the price range of to .12 per IP tell us about the market?

The floor of likely represents distressed or oddly-sized inventory in less desirable registries, while the ceiling of .12 — recorded in the APNIC region — probably reflects a small, clean block with attractive routing characteristics sold to a motivated buyer. Most activity clusters within a – band.

Is the IPv4 market trending up or down entering the second half of 2024?

Down, modestly. Prices slipped approximately 0.31% over the period. Our model forecasts a continuation to roughly .61 next month and .40 by year-end 2024 — a controlled decline, not a rout. Think of it as price normalization after several years of aggressive appreciation.

What were the most commonly traded block sizes in H1 2024?

/24 blocks dominated with 137 transactions — roughly 40% of all deals. This is the minimum independently routable prefix on most networks, making it the retail unit of the IPv4 market. Larger blocks (/16 and above) drove the bulk of dollar volume but accounted for far fewer transactions.

How did total transfer activity (including non-priced transfers) compare across RIRs?

RIPE led decisively with 3,383 recorded transfers — 64.5% of the 5,171 total — followed by ARIN at 1,788 (35.5%). APNIC, LACNIC, and AFRINIC registered zero transfers in our transfer-log dataset. RIPE's dominance in raw transfer count reflects both market maturity and high intra-European M&A-driven reassignments.

Were there any large deals — over million — in H1 2024?

Two. They combined for approximately .18 million. At the other end, 245 transactions fell below K, accounting for .04 million in aggregate value. The market remains structurally bifurcated: high volume at the small end, concentrated value at the top.

What does the deal-size distribution look like by dollar band?

Under K: 245 deals (.0M). K–0K: 77 deals (.3M). 0K–M: 19 deals (.8M). Over M: 2 deals (.2M). The K–0K band is the market's center of gravity by dollar volume, which tells you the institutional mid-market is where price discovery actually happens.

Should I buy IPv4 addresses or lease them at current rates?

At .22 per IP to buy and .5859 per IP per month to lease, the breakeven is approximately 56.7 months — just under 4.7 years. If your planning horizon exceeds five years, buying is the clear winner. The implied annual yield for a lessor is 21.2%, which is why many holders prefer to lease out inventory rather than sell.

What is the current monthly lease rate for a /24 block?

Roughly 0 per month, based on a sample of 44 lease transactions — all sourced from the RIPE region. Annualized, that's ,800 per /24 or about .03 per IP per year. Data on ARIN and APNIC lease rates was insufficient for reliable quoting this period.

What mistakes should buyers avoid in the current market environment?

Overpaying for small blocks when prices are softening is the primary risk. With our forecast pointing to .40 by December 2024, buyers who rush into /24 purchases at + without negotiating are leaving money on the table. Patience and competitive bidding across multiple brokers are essential in a declining-price environment.

What are the risks of leasing IPv4 addresses instead of buying?

Lease rates are sticky even when purchase prices fall, so your effective cost basis can deteriorate over time. More critically, lease termination means re-numbering your network — a non-trivial operational disruption. At a 56.7-month breakeven, any lease expected to last more than five years is economically irrational versus outright purchase.

Is AFRINIC a viable source for IPv4 address purchases?

Not currently. AFRINIC recorded zero priced transactions and zero transfers in H1 2024. Ongoing governance and legal disputes have effectively frozen the AFRINIC transfer market. We advise clients to avoid AFRINIC-registered inventory until institutional clarity is restored.

What risks should sellers be aware of in a softening market?

The 0.31% decline may seem trivial, but if the forecast to .40 by year-end holds, that represents roughly a 5.5% erosion from the current .22 average. Sellers sitting on large blocks should consider accelerating disposition timelines rather than anchoring to 2023-era price expectations.

How liquid is the LACNIC region IPv4 market?

Barely. Only 3 transactions closed in H1 2024, covering 11,264 addresses for 0,688 total. The average price was .33 per IP. LACNIC's transfer policies and smaller addressable buyer base keep this a niche market — suitable for regional operators, not institutional portfolio strategies.

How reliable is the year-end 2024 price forecast of .40?

We flag this forecast as reliable, based on regression analysis of the H1 transaction dataset. The 343-transaction sample is robust, the trend is consistent, and the projected decline to .40 represents an orderly continuation of the 0.31% downtrend rather than any structural break.

Will IPv6 adoption render IPv4 addresses worthless?

Not in the foreseeable future. Global IPv6 adoption remains uneven, and the installed base of IPv4-dependent infrastructure — particularly in enterprise, IoT, and legacy telecom — ensures demand for years. Even a 50% IPv6 penetration rate would not eliminate the need for IPv4 NAT traversal and dual-stack operations. The question is not if IPv4 retains value, but how quickly that value decays.

How long does a typical inter-RIR or intra-RIR transfer take to complete?

ARIN intra-region transfers typically close in 4–8 weeks, assuming clean WHOIS records and pre-approval. RIPE transfers can move faster — sometimes 2–4 weeks — owing to a more automated process. APNIC inter-RIR transfers are the most variable, often stretching to 10–12 weeks depending on source-RIR cooperation.

What drove the .12 per IP maximum price observed in H1 2024?

That outlier came from the APNIC region and almost certainly reflects a small, clean block — likely a /24 — with desirable attributes: no blacklisting history, established BGP routing, and a motivated buyer with time pressure. Prices above remain rare and non-representative of broader market clearing levels.

What is the implied annual yield for an IPv4 address lessor at current rates?

Approximately 21.2%, calculated as annual lease income (.03 per IP) divided by the current purchase cost (.22 per IP). That yield is extraordinary by any fixed-income standard, which explains why institutional holders and PE-backed aggregators continue to accumulate blocks for leasing portfolios.

How should I interpret the gap between ARIN's 141 priced transactions and RIPE's 3,383 total transfers?

Most RIPE transfers are non-market events — M&A-driven reassignments, corporate restructurings, and intra-group moves that carry no arm's-length price. Only 107 of RIPE's transfers had verifiable pricing. ARIN, by contrast, shows 141 priced deals against 1,788 total transfers. The ratio of priced-to-total is a rough proxy for market commercialization: ARIN's is higher.

What does a softening market mean for network operators planning 2025 budgets?

If prices drift toward .40 by December 2024, a /24 block would cost approximately ,038 versus today's ,504 average. For operators planning large-scale acquisitions — say a /16 — that delta compounds to roughly 0,000 in savings. Timing purchases for Q4 2024 or Q1 2025 may be prudent if operational requirements allow the wait.

Are there enough transactions to consider the H1 2024 data statistically meaningful?

Yes. With 343 priced transactions across four active RIR regions and a tight average-to-median spread (.22 vs. .50), the dataset is among the more robust semiannual samples we have seen. The primary caveat is LACNIC's 3-deal sample, which is too thin for reliable regional inference.