24 min read

This report analyzes the IPv4 transfer market for Q2 2026, based on completed IPv4Center marketplace transactions and official RIR transfer records.

Executive Summary

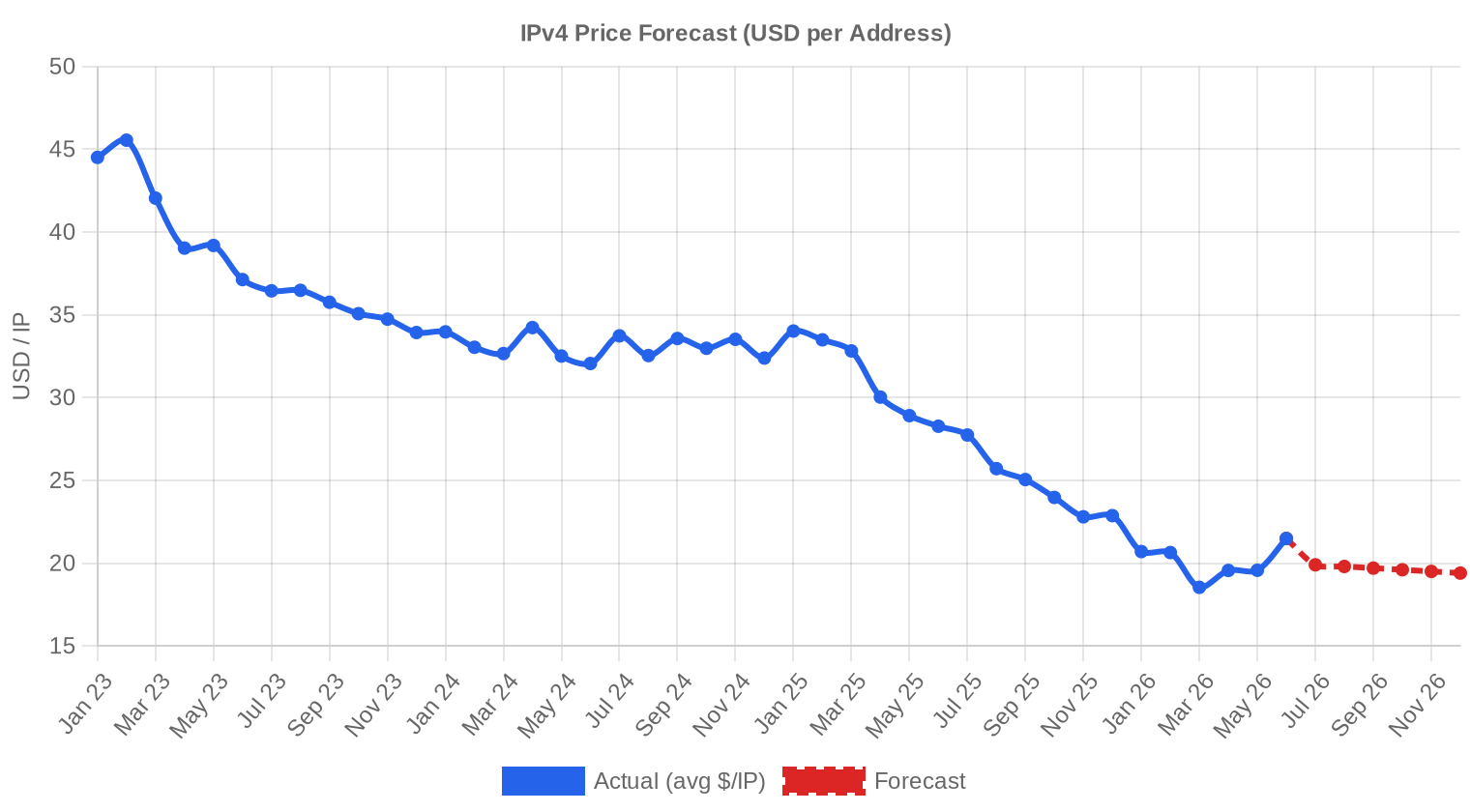

The IPv4 transfer market posted an average price of $20.16 per address in Q2 2026, up a modest $1.30 from Q1 2026 but down 30.5% from $29.00 in Q2 2025. A total of 312 transactions moved 1,660,928 addresses for an aggregate value of $21.7 million. Transaction volume climbed 9.9% quarter-over-quarter, yet average deal sizes shrank sharply — from 129,273 IPs per deal in Q1 to 69,704 in Q2. The market trend remains down, with the regression line declining 0.5% over the quarter, pointing to a structural reset in pricing rather than a temporary dip.Market Overview

| Transactions | 312 |

| IP Addresses Traded | 1,660,928 |

| Estimated Market Value | $21,747,629 |

| Average Price / IP | $20.16 |

| Median Price / IP | $20.00 |

| RIR Transfers | 1,663 |

Year-over-Year Comparison

| Metric | This period | A year earlier (Q2 2025) | Change |

|---|---|---|---|

| Transactions | 312 | 219 | +42.5% |

| IP Addresses Traded | 1,660,928 | 1,219,840 | +36.2% |

| Estimated Market Value | $21,747,629 | $26,772,793 | -18.8% |

| Average Price / IP | $20.16 | $29.02 | -30.5% |

| RIR Transfers | 1,663 | 1,974 | -15.8% |

Price Dynamics

The pricing band stretched from $10 to $41 per IP this quarter, a 4:1 spread that reflects deep heterogeneity in block quality and RIR origin. The $10 floor typically corresponds to large, older ARIN blocks with limited documentation or partial blacklisting; the $41 ceiling was an ARIN transaction, likely a small, clean /24 in a desirable subnet. Median price sat at $20 — essentially flat with the average, suggesting a tighter distribution around the center than the extremes imply. The quarterly uptick of $1.30 from Q1 looks like mean reversion after the Q1 dip rather than the start of a new rally. Against the year-ago reading, prices are off 30.5%, and the regression slope says the drift is still gently negative at -0.5%.

Pricing by RIR

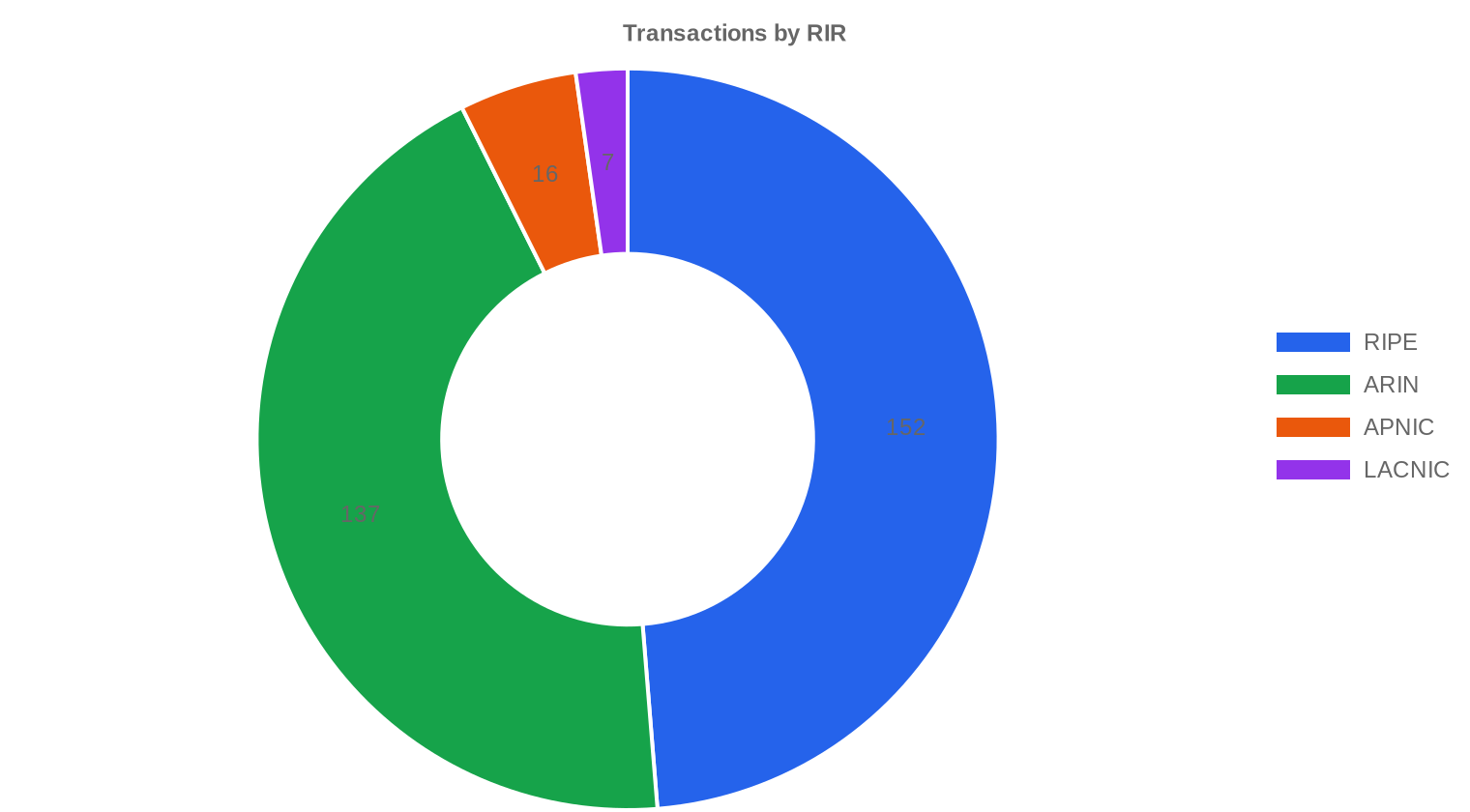

RIPE continues to anchor the market at 48.7% of transaction volume but is no longer the cheapest registry. ARIN blocks averaged $18.96/IP across 137 deals — a $2.11 discount to RIPE's $21.07 average — which marks a widening gap that reflects ARIN's deeper pool of legacy allocations entering the secondary market. LACNIC commanded the highest prices at $24.14/IP, though on a thin 7-transaction sample that makes it more anecdote than trend. APNIC sat in the middle at $20.19 across 16 trades, roughly in line with the global average. AFRINIC recorded zero transactions for the quarter, consistent with the ongoing transfer freeze in that region. RIPE: $21.07/IP across 152 transactions (36.7% of IP volume). ARIN: $18.96/IP across 137 transactions (55.8% of IP volume). APNIC: $20.19/IP across 16 transactions (6.6% of IP volume). LACNIC: $24.14/IP across 7 transactions (0.8% of IP volume). AFRINIC: No transactions recorded.| RIR | Transactions | Avg $/IP | Median $/IP | IPs Traded | RIR Transfers | Next Month (proj.) | Year-End (proj.) |

|---|---|---|---|---|---|---|---|

| RIPE | 152 | $21.07 | $21.00 | 610,304 | 1,000 | $23.00 | $22.00 |

| ARIN | 137 | $18.96 | $18.00 | 927,232 | 663 | $17.50 | $16.50 |

| APNIC | 16 | $20.19 | $20.25 | 110,336 | 0 | $22.00 | $21.00 |

| LACNIC | 7 | $24.14 | $25.50 | 13,056 | 0 | $25.00 | $24.00 |

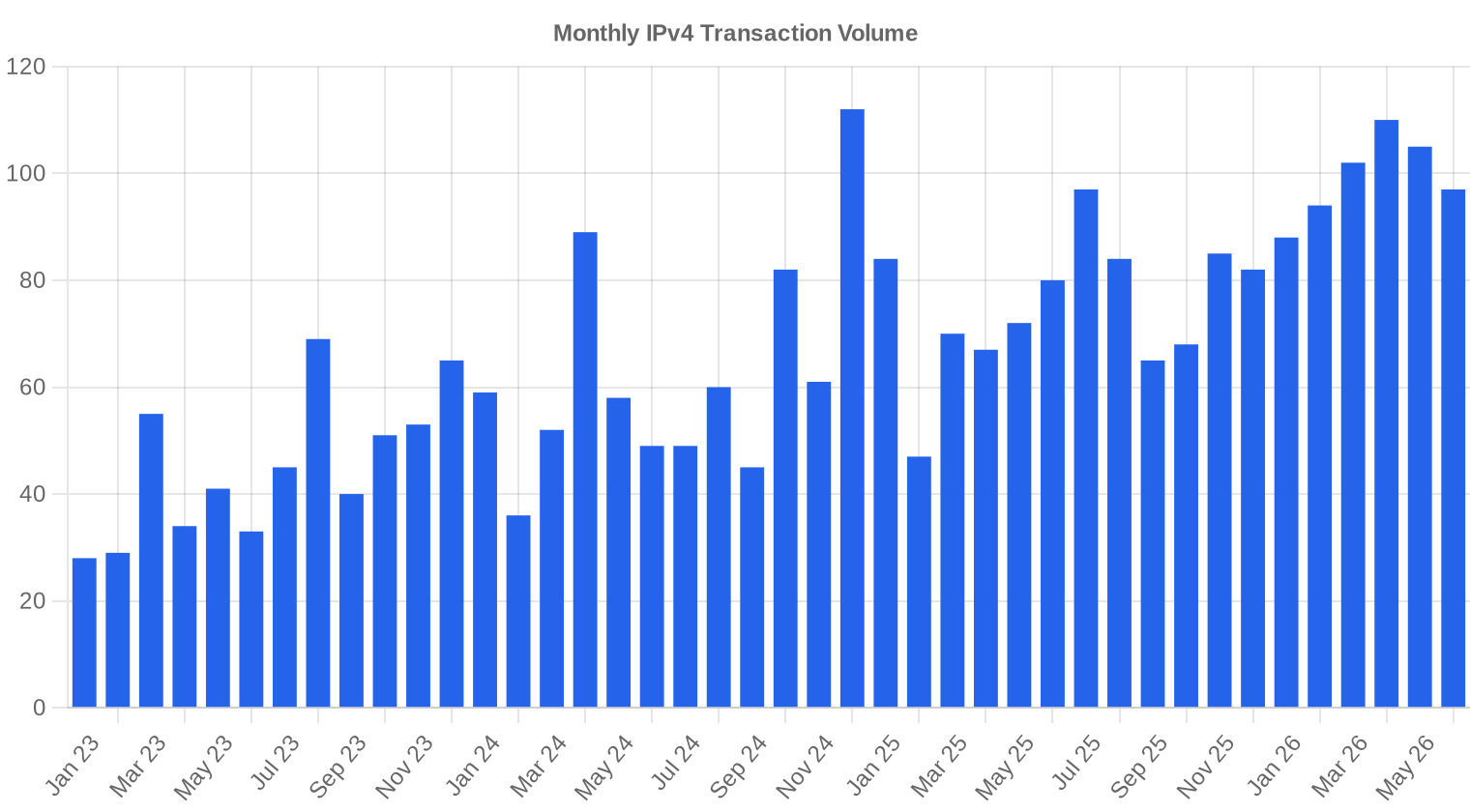

Transaction Volume

Supply & Block Sizes

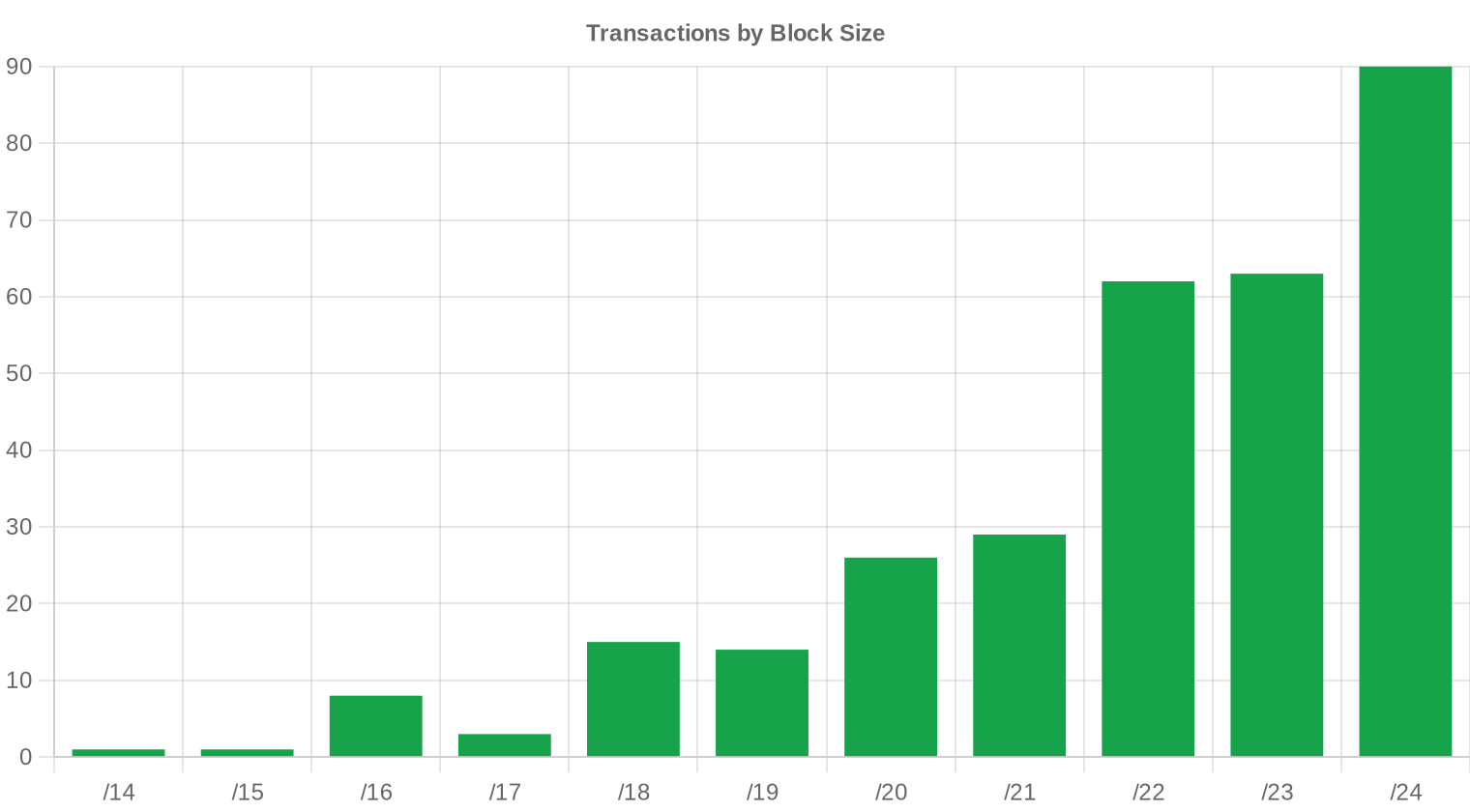

/24 blocks dominated trading activity with 90 transactions — the most popular prefix size by a wide margin. Buyers continue gravitating to /24s for targeted deployments: mail servers, web hosting clusters, small-scale cloud projects where a single 256-address block covers requirements without tying up capital in larger allocations. The preference for small blocks drove the compression in average deal size from 129,273 IPs in Q1 to 69,704 in Q2, even as total transaction count rose.

Geographic Activity

The United States led with 116 transactions, followed by the United Kingdom at 46 and Canada at 25 — together accounting for 60% of all deals. Sweden (12), the Netherlands (10), and Australia (8) formed the next tier. The geographic concentration in North America and Western Europe reflects where legacy allocations originated and where enterprise IT budgets remain largest, though cross-border deals like US-Korea and UK-Hong Kong show the market's increasingly global reach.Registry Transfer Activity

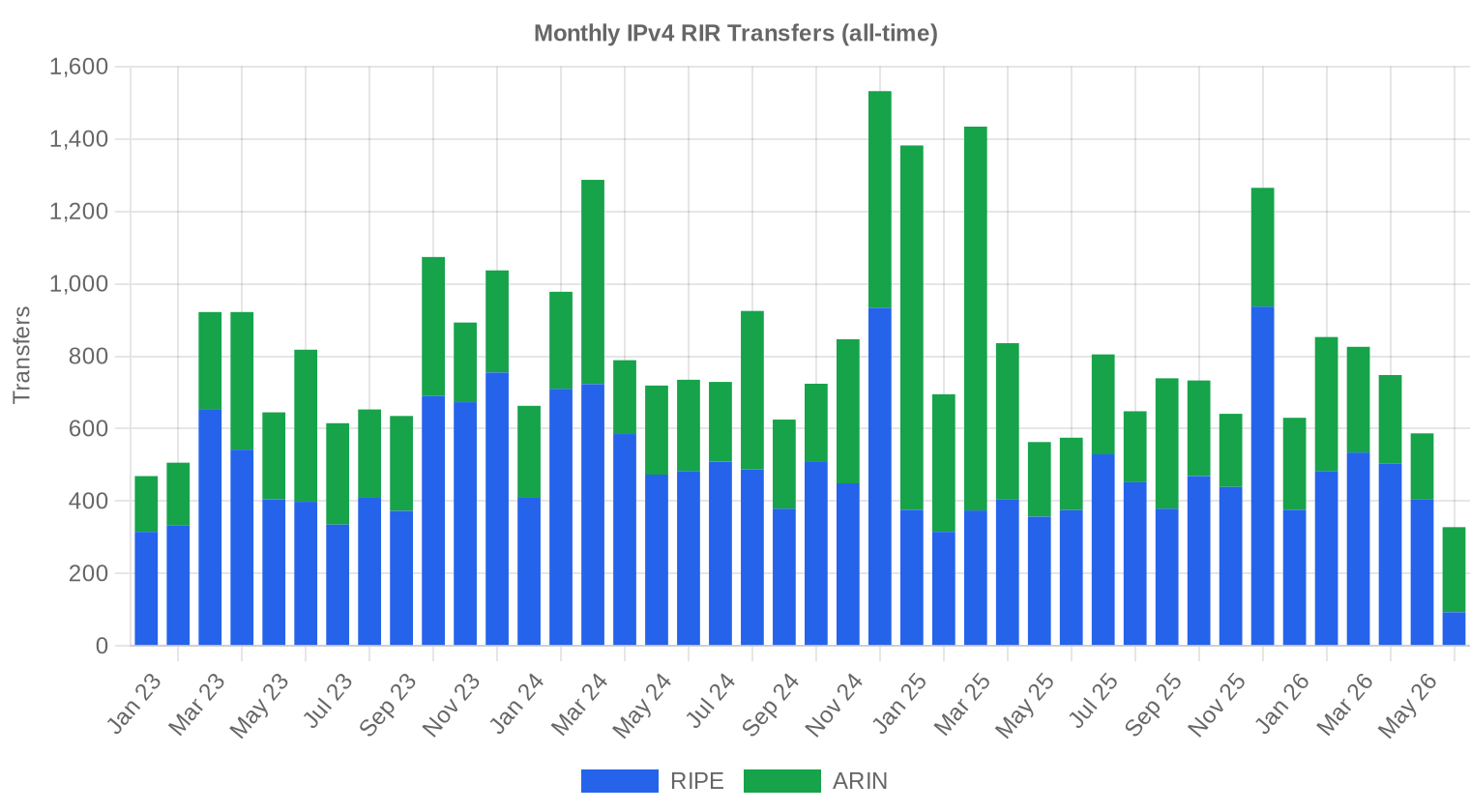

RIR-recorded transfers totaled 1,663 for the quarter, a figure that includes inter-RIR and intra-RIR movements beyond just sale transactions. RIPE accounted for 1,000 of those transfers — 60.1% of the total — with ARIN contributing 663. APNIC, LACNIC, and AFRINIC registered zero official transfers in the period.Long-Run Transfer Trends

Over the trailing 42-month window, 34,030 transfers have been recorded across all RIRs. RIPE has handled 59.7% of that cumulative volume against ARIN's 40.3%. The peak month was December 2024, when year-end corporate balance sheet optimization and tax-driven asset dispositions created a temporary surge — a pattern that has repeated in each of the last three Decembers.| RIR | RIR Transfers |

|---|---|

| RIPE | 20,329 |

| ARIN | 13,701 |

| RIR Transfers | 34,030 |

Outlook & Forecast

Forecasting each block-size band and RIR separately with our AI model:

The overall average price per IP is projected to reach $19.40 by December 2026, with a next-month estimate of $20.00 per IP.

- RIPE: projected at $23.00 per IP next month, trending toward $22.00 by December 2026.

- ARIN: projected at $17.50 per IP next month, trending toward $16.50 by December 2026.

- APNIC: projected at $22.00 per IP next month, trending toward $21.00 by December 2026.

- LACNIC: projected at $25.00 per IP next month, trending toward $24.00 by December 2026.

- AFRINIC: insufficient data for a reliable forecast.

Forecast by Block Size

| Block | Current $/IP | Next Month | Year-End | Confidence |

|---|---|---|---|---|

| /24 | $26.00 | $26.00 (0.0%) | $25.00 (-3.8%) | medium |

| /23 | $20.00 | $20.50 (+2.5%) | $20.00 (0.0%) | medium |

| /22 | $17.00 | $17.00 (0.0%) | $16.00 (-5.9%) | medium |

| /21 | $17.70 | $17.50 (-1.1%) | $17.00 (-4.0%) | medium |

| /20 | $15.75 | $15.75 (0.0%) | $16.00 (+1.6%) | medium |

| /19 | $14.25 | $14.50 (+1.8%) | $14.50 (+1.8%) | low |

| /18-/16 | $13.50 | $13.50 (0.0%) | $14.00 (+3.7%) | medium |

| /15-up | $10.00 | $10.00 (0.0%) | $10.50 (+5.0%) | low |

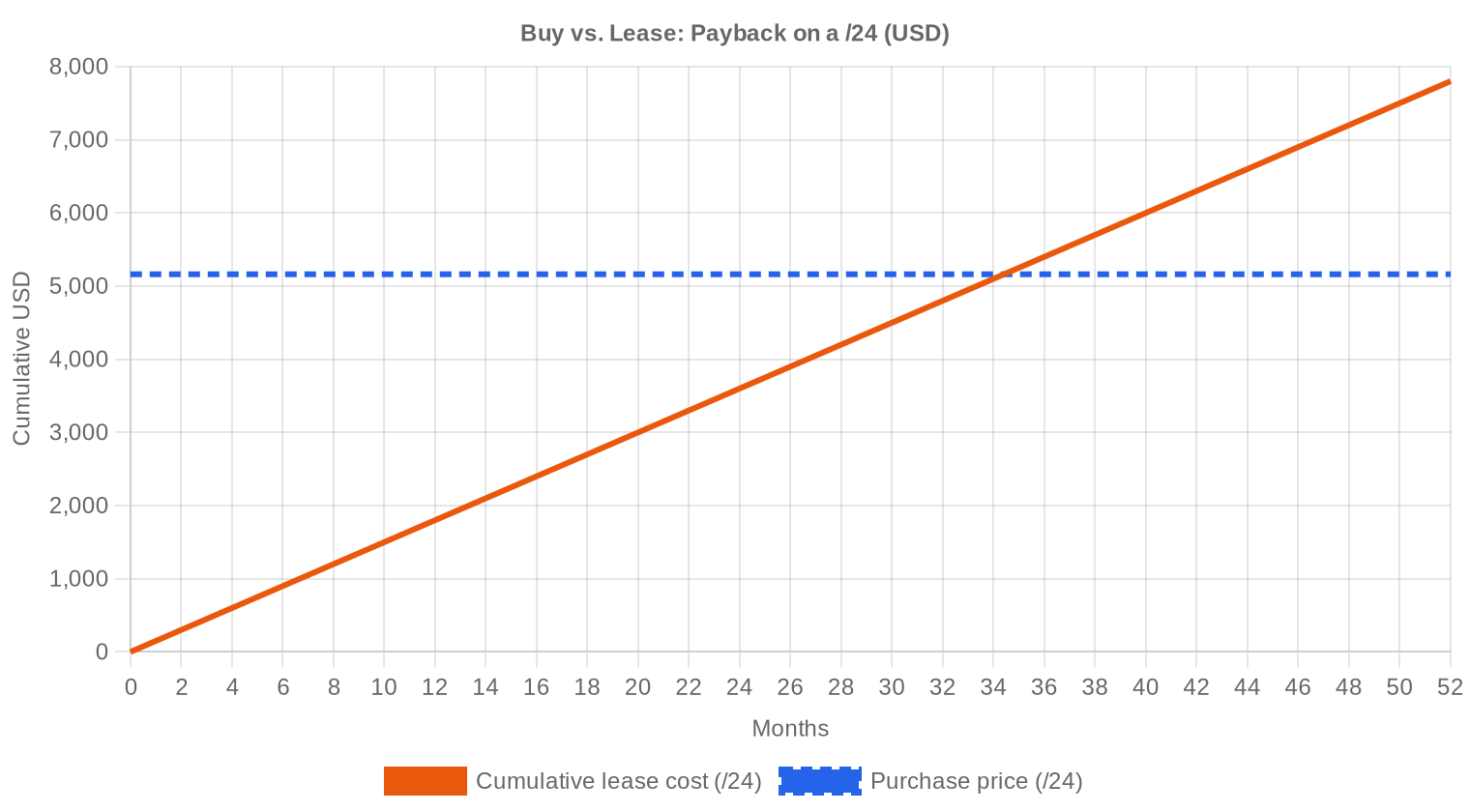

Editor's Take: Buy vs. Lease

The buy-versus-lease math is straightforward this quarter. At $20.16 per IP and a lease rate of $0.59/IP/month, the breakeven payback sits at 34.4 months — just under three years. For any organization planning to hold addresses beyond that window, buying is the clear play. The implied annual yield of 34.9% on a purchase-and-lease strategy remains far above fixed-income alternatives and competitive with early-stage venture returns, though with significantly lower volatility. At a /24 level, that means paying $5,161 to buy versus $150/month to lease — and recovering the purchase price in under 35 months of lease income. Sellers considering a leaseback should take note: even with prices falling, the yield math still rewards ownership for patient holders.| /24 Purchase price | $5,161 |

| /24 Lease price | $150 / mo |

| Payback period | 34.4 mo (2.9 yr) |

| Gross annual yield | 34.9% |

What This Means for You

Buyers: Prices are 30.5% below where they stood a year ago and the model sees another 3.8% downside by December. There is no urgency to buy today that wasn't present last quarter. If you need blocks now, ARIN inventory at $18.96 average is the value play — but run blacklist checks before closing. Sellers: The pricing trend is not your friend. Every quarter you hold an unused allocation costs you roughly $0.60-0.80/IP in opportunity cost relative to last year's prices. If you have clean blocks, the market is liquid enough to move them — 312 deals closed this quarter. Waiting for a rebound requires a thesis on what reverses a four-quarter decline. Leasers: At $0.59/IP/month, leasing remains expensive against buying for any hold period beyond 34 months. If your need is temporary — a 12-to-18-month project — leasing still makes sense. Beyond that, acquire. Block holders: The 34.9% annual yield on purchase-and-lease is the highest risk-adjusted return this asset class has offered since prices began declining. Your blocks are producing more income relative to their current market value than at any point in the past two years. Hold and lease unless you need the liquidity.Browse verified IPv4 blocksSell IPv4 →

List your blocks with managed transferLease IPv4 →

Flexible short-term capacityLease Out IPv4 →

Turn idle blocks into recurring revenue

IPv4 Pricing by Block Size

Small blocks carry a steep premium. A /24 at the global median trades around $5,120 ($20 × 256), but actual /24 transaction prices frequently hit $25-30/IP because of the convenience factor and minimum-viable-allocation demand. Larger blocks — /20 and above — tend to price at the $16-19 range on a per-IP basis, reflecting volume discounts and the smaller buyer pool capable of deploying 4,096+ addresses. The per-IP premium for a /24 versus a /16 can run 30-40%, a spread that has held steady even as absolute prices declined.| Block | IPs | Buy: /IP | Buy: Total | Lease: /IP/mo | Lease: Monthly |

|---|---|---|---|---|---|

| /24 | 256 | $35–45 | $8,960–11,520 | $0.38–0.50 | $97–128 |

| /22 | 1,024 | $28–38 | $28,672–38,912 | $0.33–0.45 | $338–461 |

| /20 | 4,096 | $22–32 | $90,112–131,072 | $0.30–0.40 | $1,229–1,638 |

| /18 | 16,384 | $20–30 | $327,680–491,520 | $0.30–0.38 | $4,915–6,226 |

| /16 | 65,536 | $18–28 | $1,179,648–1,835,008 | $0.30–0.35 | $19,661–22,938 |

IPv4 Price History: 2011–2026

IPv4 addresses first traded for $4-5/IP in 2011, shortly after IANA exhausted its free pool. Prices climbed steadily through the 2010s, accelerating to $25-30/IP by 2020 and peaking near $55-60/IP in late 2023. AWS's decision to charge $3.60/year per public IPv4 address (effective February 2024) was the single most disruptive event in market history — it incentivized address returns and lease-backs, adding supply precisely as prices were stretched. The current $20.16 average represents a 65% drawdown from peak and a return to 2019-era levels.| Year | ~Price/IP | Key Event |

|---|---|---|

| 2011 | $7–12 | IANA free pool exhausted; Microsoft/Nortel deal ($11.25/IP) |

| 2012 | $8–12 | RIPE NCC reaches last /8; begins /22-only allocation |

| 2014 | $10–15 | LACNIC free pool exhausted |

| 2015 | $8–15 | ARIN free pool exhausted |

| 2017–18 | $12–18 | Leasing market grows; cloud demand rises |

| 2019 | $18–24 | RIPE NCC exhausts remaining free pool |

| 2021–22 | $50–60+ | Post-pandemic peak; hyperscaler build-outs |

| 2024 | $35–52 | AWS IPv4 charge ($0.005/IP/hr); large block correction |

| 2025–26 | $18–45 | Market bifurcation; /16s below $20 for first time since 2019 |

Market Structure: Who Is Buying & Selling

The buy side is dominated by mid-tier cloud providers, regional ISPs building out fixed-wireless and fiber networks, and hosting companies that need clean IP space for mail and web services. The sell side skews toward legacy corporate holders — enterprises sitting on /16s allocated in the 1990s that no longer align with their network architecture — and restructuring-driven sales from bankrupt hosting operators and acquired companies shedding redundant assets.IPv4 vs. Other Asset Classes

At a 34.9% implied annual yield (buy at $20.16, lease at $0.59/month), IPv4 addresses outperform every conventional asset class. Ten-year US Treasuries sit around 4.2%. REITs yield 5-7%. Even high-yield credit barely touches 8%. The catch is liquidity and depreciation risk — prices have fallen 30.5% year-over-year, meaning a pure capital-gains bet would have been painful. The yield story only works if you can find lessees, and the lease market is not infinitely deep.| Asset Class | Typical Yield | Liquidity | Primary Risk |

|---|---|---|---|

| IPv4 | 34.9% | Moderate | IPv6 adoption, block quality |

| Commercial Real Estate | 5–8% | Low | Vacancy, rate cycle |

| Investment-Grade Bonds | 4–5% | High | Duration, credit risk |

| S&P 500 | ~1,3% | High | Market volatility |

| Money Market / T-Bills | ~4–5% | High | Rate cycle changes |

IPv6 Adoption & Why IPv4 Remains Essential

IPv6 handles roughly 45% of Google's global traffic as of mid-2026, up from 40% two years ago. The pace of adoption is steady but not accelerating enough to displace IPv4 demand in the enterprise or hosting sectors within this decade. Dual-stack remains the operational norm, and any network that needs to reach IPv4-only endpoints — which still represent the majority of the internet's long tail — needs IPv4 space. The coexistence runway extends well into the 2030s.AI & Cloud Infrastructure Demand

AI infrastructure buildouts are consuming IPv4 addresses at the margin. Training clusters and inference farms operated by hyperscalers generally pull from their existing pools, but the dozens of smaller AI startups spinning up GPU clouds need public-facing IPs for API endpoints, model-serving infrastructure, and data ingestion pipelines. This demand layer did not exist three years ago, and while it has not moved aggregate pricing, it is visible in the /24 and /23 segments where 90+ transactions occurred this quarter.What Determines IPv4 Block Value

Block value hinges on five factors: blacklist cleanliness, allocation age, RIR origin, subnet reputation, and transferability. A /24 with zero blacklist hits from a pre-2000 ARIN allocation can command $30+/IP; the same prefix size from a 2015 RIPE allocation with Spamhaus listings might trade at $14. Buyers who skip due diligence on these factors routinely overpay by 20-40% relative to clean-market comps.Sell vs. Lease: A Decision Framework

Selling makes sense when you need immediate liquidity, when you believe prices will continue declining (the data supports this view), or when the administrative burden of lease management exceeds your appetite for operational complexity. Leasing is the superior strategy when you expect to hold the asset for 3+ years and can maintain occupancy — at 34.9% annual yield, the income stream compounds faster than the asset depreciates at current decline rates of roughly 30% per year.| /24 Purchase price | $5,161 |

| /24 Lease price | $150 / mo |

| Payback period | 34.4 mo (2.9 yr) |

| Gross annual yield | 34.9% |

RIPE NCC 24-Month Transfer Restriction

RIPE NCC's 24-month holding period before inter-RIR transfers constrains the velocity of speculative flipping in the European registry. Blocks acquired today cannot move to ARIN or APNIC until Q2 2028. This rule creates a price floor for RIPE space — holders who locked in at higher prices are less inclined to sell at a loss when they cannot arbitrage to another region — and partially explains RIPE's $2.11 premium over ARIN this quarter.Deal Size Distribution

The market's center of gravity shifted toward smaller transactions. Of 312 deals, 244 (78%) were sub-$50K for a combined $3.6 million. The 10 deals exceeding $1 million accounted for $18.5 million — 85% of total market value from just 3.2% of transactions. Average deal size dropped 46% from Q1's 129,273 IPs to 69,704 IPs, confirming the dominance of /24 and /23 trades over bulk block moves.Top Trading Countries

The US dominated with 116 transactions (37% of all deals), driven by ISP expansion, cloud infrastructure needs, and BEAD-related positioning. The UK's 46 transactions represent its strongest quarter in over a year, likely linked to post-Brexit digital infrastructure investment mandates. Canada's 25 deals tracked closely with CRTC-driven broadband expansion programs targeting underserved provinces.BEAD Broadband Program Impact

The $42.45 billion BEAD program is moving from state-level planning into procurement phase in multiple states during H2 2026. Regional ISPs selected as BEAD grant recipients need IPv4 space for subscriber assignments, and they typically buy /20 to /18 blocks — exactly the mid-market segment where supply has been thinning. We expect BEAD-related demand to become visible in transaction data by Q4 2026, putting upward pressure on mid-size block pricing even as /24s continue drifting lower.Hyperscaler IPv4 Holdings

Amazon, Microsoft, and Google collectively hold an estimated 120-140 million IPv4 addresses. AWS's public IPv4 pricing at $3.60/year per address has turned their holdings into a revenue-generating asset — and reduced the incentive to return space to the market. If anything, the hyperscalers are net accumulators at current prices, though their purchases rarely appear in public transfer databases because they are structured as private intra-company transfers or bulk acquisitions under NDA.Macroeconomic Conditions & Market Impact

Enterprise IT budgets remain stable in mid-2026, with Gartner's latest survey showing 3.8% year-over-year spending growth. Interest rates have softened modestly, which marginally reduces the opportunity cost of holding IPv4 as an asset. The broader macro environment is neither stimulating nor suppressing demand — the 30.5% year-over-year price decline is supply-driven, not demand-driven, rooted in the post-AWS-charge release of previously hoarded addresses.Model Update & Calibration

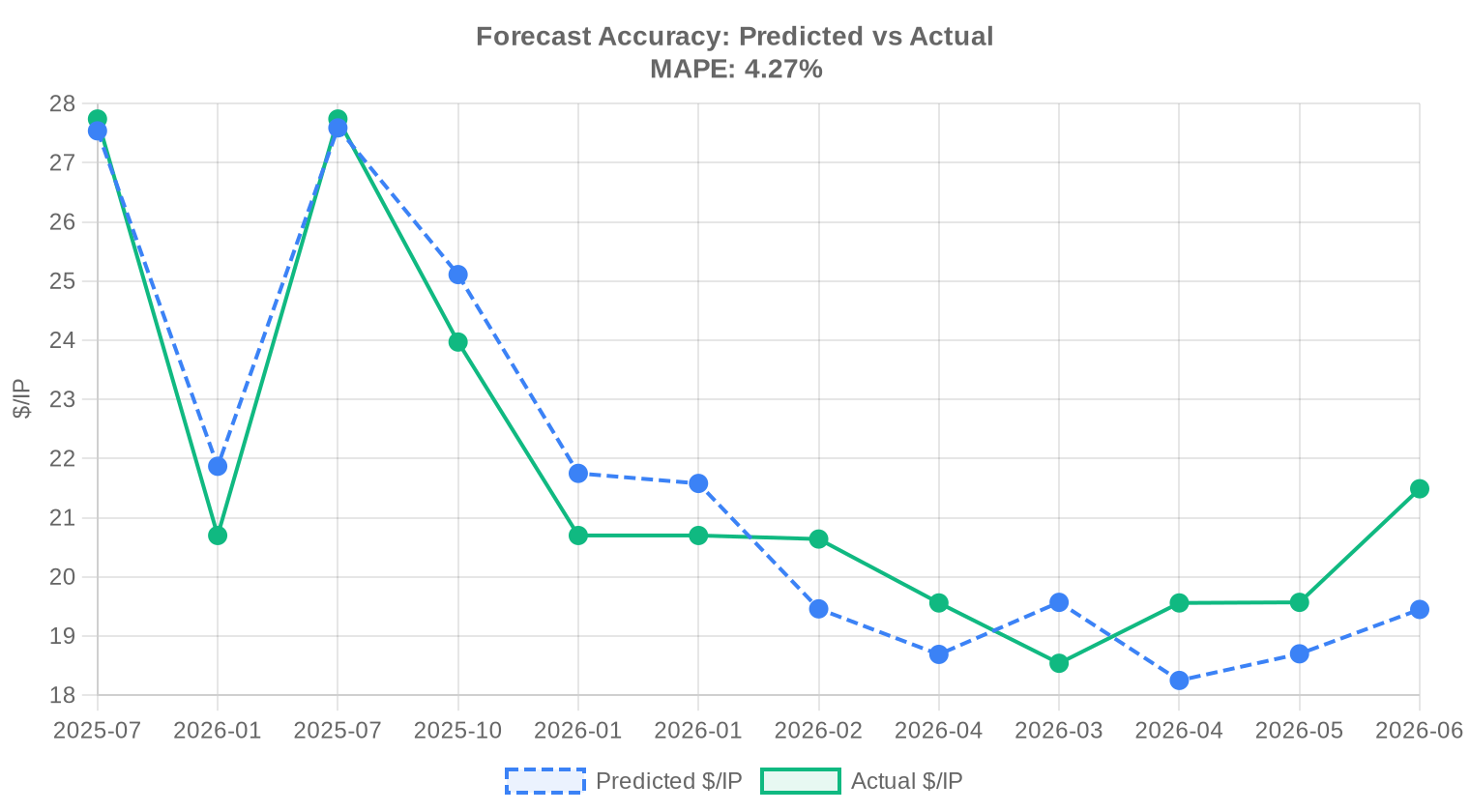

As part of our continuous improvement process, we backtested previous forecasts against realised prices and fine-tuned the model accordingly. Recent months now carry more influence than older data, and the confidence bands have been widened or narrowed based on how well they captured actual outcomes in the past. You can see the full backtest results in the table and chart below.

| Report Period | Target Month | Predicted | Actual | Deviation |

|---|---|---|---|---|

| 2026-01 | 2026-02 | $19 | $21 | -6% |

| 2026-Q1 | 2026-04 | $19 | $20 | -4% |

| 2026-02 | 2026-03 | $20 | $19 | +6% |

| 2026-03 | 2026-04 | $18 | $20 | -7% |

| 2026-04 | 2026-05 | $19 | $20 | -4% |

| 2026-05 | 2026-06 | $19 | $21 | -9% |

Methodology

Figures are based on completed IPv4Center marketplace transactions and RIR transfer statistics. Prices are in US dollars per IP address. Forecasts are produced by an AI model that analyses each block-size band and RIR segment separately (with outlier-trimmed medians) alongside known market catalysts; they are estimates, not guarantees.

Data Sources

- Hilco Streambank — Completed auction transaction records

- RIPE NCC — Inter-RIR and intra-RIR transfer statistics

- ARIN — North American transfer reports and waiting list data

- APNIC — Asia-Pacific transfer records

- LACNIC — Latin American and Caribbean transfer data

- IPv4Center.com — Proprietary marketplace transaction and lease pricing data

This report is generated automatically for informational purposes only and does not constitute financial advice.

Frequently Asked Questions

What was the average IPv4 price in Q2 2026?

The average price was $20.16 per IP address, based on 312 transactions covering 1,660,928 addresses.

How much does a /24 IPv4 block cost in Q2 2026?

At the market average of $20.16/IP, a /24 (256 addresses) costs approximately $5,161. Clean /24 blocks with no blacklist issues often trade at $25-30/IP, pushing the price to $6,400-$7,680.

How much did IPv4 prices drop year-over-year?

Prices fell 30.5% compared to Q2 2025, when the average was approximately $29/IP.

Which RIR has the cheapest IPv4 addresses?

ARIN blocks averaged $18.96/IP in Q2 2026, the lowest among active registries. RIPE averaged $21.07 and LACNIC commanded $24.14.

Which RIR has the most expensive IPv4 addresses?

LACNIC at $24.14/IP, though based on only 7 transactions. Among high-volume registries, RIPE was priciest at $21.07/IP.

How many IPv4 transactions occurred in Q2 2026?

312 transactions closed, a 9.9% increase from Q1 2026. These moved 1,660,928 total addresses.

What is the most commonly traded IPv4 block size?

The /24 (256 addresses) was the most traded prefix size with 90 transactions, reflecting strong demand for minimum-viable allocations.

Which countries buy the most IPv4 addresses?

The United States led with 116 transactions, followed by the United Kingdom (46) and Canada (25). Together they represented 60% of all deals.

Is it better to buy or lease IPv4 addresses in 2026?

At current prices ($20.16/IP) and lease rates ($0.59/month), buying breaks even at 34.4 months. If you need addresses for more than three years, buying is more cost-effective.

What is the current IPv4 lease rate?

The average lease rate is $0.59 per IP per month, or approximately $150 per month for a /24 block. Annual cost per IP is about $7.03.

What is the payback period for buying IPv4 vs. leasing?

At $20.16 per IP purchase price and $0.59/month lease rate, the breakeven is 34.4 months — approximately 2.9 years.

What return does IPv4 generate as an investment?

The implied annual yield on a buy-and-lease strategy is 34.9%, based on current purchase prices and lease rates. This exceeds conventional fixed-income and real estate yields.

Where are IPv4 prices headed by end of 2026?

Our model projects $19.40/IP by December 2026, a 3.8% decline from current levels. The forecast is based on four consecutive quarters of negative regression slope.

How long does an IPv4 transfer take?

Transfer timelines vary by RIR. ARIN transfers typically close in 2-4 weeks. RIPE transfers can take 2-6 weeks depending on documentation completeness and whether the 24-month holding rule applies.

What is RIPE's 24-month holding rule?

RIPE NCC requires that IPv4 blocks be held for 24 months before they can be transferred to another RIR region. This constrains speculative trading and affects supply dynamics for RIPE-registered space.

What mistakes should be avoided when buying IPv4?

The three most common mistakes are skipping blacklist verification, failing to confirm the seller has clear title to the block, and not using escrow. Any of these can result in acquiring unusable addresses or losing your payment entirely.

What are the risks of skipping blacklist verification?

Blocks with Spamhaus, Barracuda, or other major blacklist entries can be unusable for email, web hosting, and many cloud services. Remediation can take months, and some listings are effectively permanent. Always check before closing.

Why shouldn't you skip escrow in an IPv4 transaction?

IPv4 transfers are irreversible once processed by the RIR. Without escrow, you risk paying for blocks that never transfer or receiving payment for blocks you've already released. Escrow protects both parties for a small fee relative to deal value.

What risks should IPv4 investors be aware of?

Key risks include continued price depreciation (down 30.5% YoY), IPv6 adoption reducing long-term demand, regulatory changes at RIRs affecting transferability, and lease-market saturation compressing yields.

Can I buy IPv4 addresses from any RIR region?

Inter-RIR transfers are possible between ARIN, RIPE, and APNIC under specific policies. LACNIC and AFRINIC currently do not support outbound inter-RIR transfers, limiting their liquidity.

Why are ARIN addresses cheaper than RIPE?

ARIN has a larger pool of legacy allocations entering the secondary market, and its transfer policies are somewhat more streamlined. RIPE's 24-month holding rule also constrains supply, supporting higher prices.

How does AWS's IPv4 charge affect the market?

AWS's $3.60/year per public IPv4 address — introduced in February 2024 — has been the most significant structural change. It incentivized organizations to return unused addresses, increasing supply and contributing to the 30%+ price decline over the past year.

What is the BEAD program's impact on IPv4?

The $42.45 billion US broadband program is entering procurement phase, and grant recipients need IPv4 blocks for subscriber networks. This is expected to tighten supply in the /20 to /18 range by late 2026.

Will IPv6 make IPv4 worthless?

Not in any foreseeable timeframe. IPv6 handles about 45% of Google's traffic, but the long tail of the internet remains IPv4-dependent. Dual-stack operations will persist well into the 2030s, sustaining IPv4 demand.

What makes an IPv4 block more valuable?

Clean blacklist status, pre-2000 allocation dates, well-known RIR origin (ARIN or RIPE), and clear transfer documentation all increase value. A clean block can trade at 30-40% premiums over a comparable block with issues.

How big is the total IPv4 transfer market?

Q2 2026 saw $21.7 million in total transaction value across 312 deals. Over the trailing 42 months, 34,030 transfers have been recorded across all RIRs.

Should I sell my IPv4 block now or wait?

Prices have declined 30.5% year-over-year, and our model projects further erosion to $19.40 by year-end. Unless you have a specific thesis for a reversal, selling sooner captures more value than waiting.

What is the minimum IPv4 block size I can buy?

A /24 (256 addresses) is the smallest block that can be independently routed on the internet and is the standard minimum for transfers. Smaller blocks exist but are not practically usable.

How is AI infrastructure affecting IPv4 demand?

AI startups building GPU clouds need public IPv4 addresses for API endpoints and model-serving infrastructure. This demand is concentrated in the /24 and /23 segments, contributing to the 90+ /24 trades recorded this quarter.

Are there IPv4 transactions in Africa?

AFRINIC recorded zero transactions in Q2 2026 and zero official transfers. The ongoing governance and transfer-policy freeze at AFRINIC has effectively removed African-registered space from the secondary market.