26 min read

This report analyzes the IPv4 transfer market for June 2026, based on completed IPv4Center marketplace transactions and official RIR transfer records.

Executive Summary

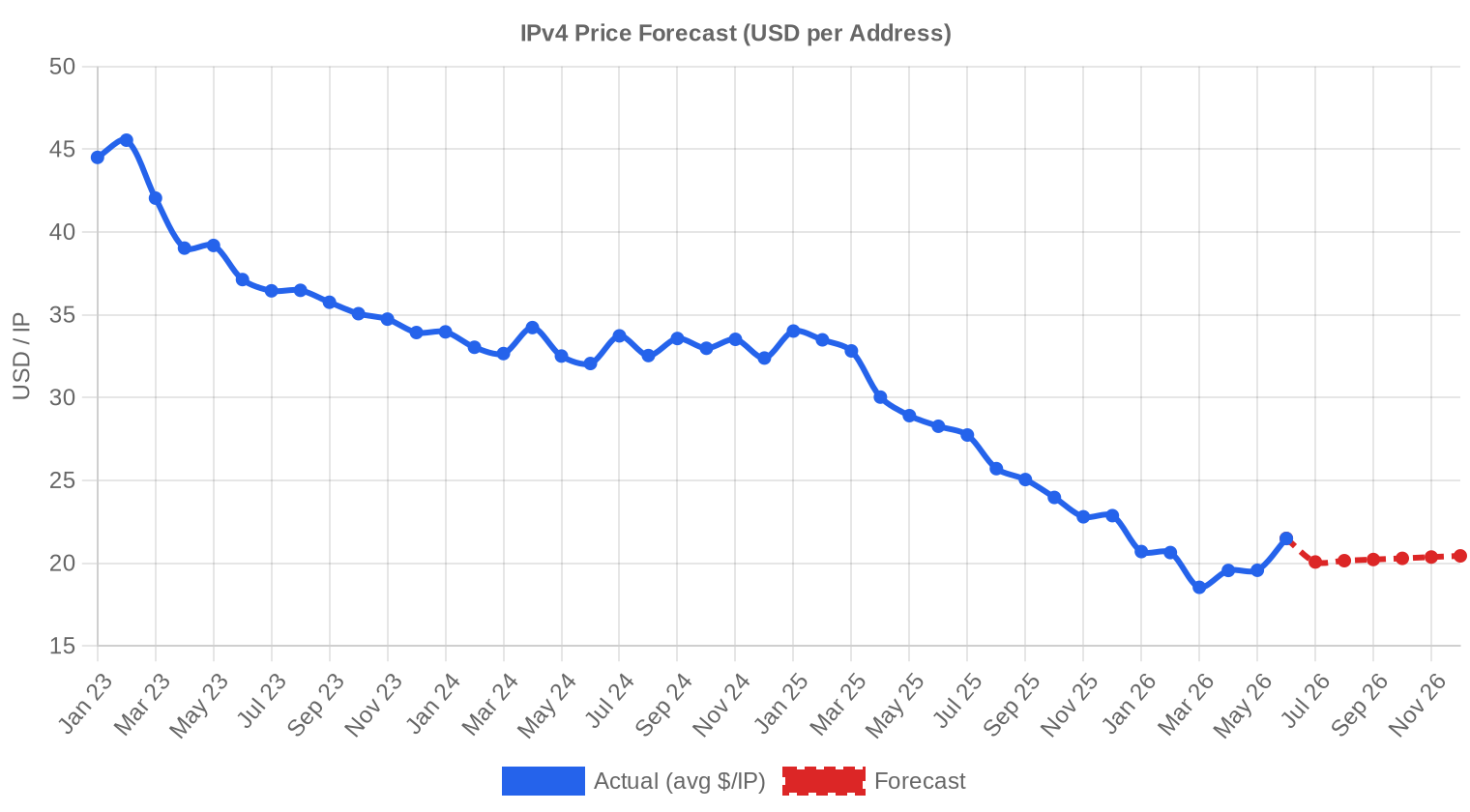

The IPv4 transfer market processed 97 transactions in June 2026 covering 580,608 addresses at a weighted average of $21.49 per IP, generating $7.18 million in total value. Average pricing rose 9.8% from May's levels, but the year-over-year picture tells the real story: $21.49 is 24% below the June 2025 average. Transaction volume dipped 7.6% month-over-month, while deal sizes swelled — the average transaction moved 74,033 addresses, up 35% from May's 54,716. The median of $20 per IP and the overall trend classification of "up" on a 0.37% regression slope suggest the month-over-month bounce is more of a stabilization than a reversal of the broader downtrend.Market Overview

| Transactions | 97 |

| IP Addresses Traded | 580,608 |

| Estimated Market Value | $7,181,153 |

| Average Price / IP | $21.49 |

| Median Price / IP | $20.00 |

| RIR Transfers | 328 |

Year-over-Year Comparison

| Metric | This period | A year earlier (June 2025) | Change |

|---|---|---|---|

| Transactions | 97 | 80 | +21.3% |

| IP Addresses Traded | 580,608 | 295,424 | +96.5% |

| Estimated Market Value | $7,181,153 | $6,613,239 | +8.6% |

| Average Price / IP | $21.49 | $28.27 | -24.0% |

| RIR Transfers | 328 | 575 | -43.0% |

Price Dynamics

The spread between the cheapest and most expensive IP traded in June was $31 — from $10 at the floor to $41 at the ceiling. That $10 low almost certainly reflects a large, lightly-cleaned ARIN block sold in bulk, while the $41 high likely represents a small, pristine RIPE allocation sold at a per-IP premium. The 9.8% month-over-month increase in average pricing was driven in part by a shift in deal-size composition: three transactions exceeding $1 million totaled $8.45 million alone, pulling the weighted average higher. Strip those out and the sub-$50K tier — which accounted for 80 of 97 deals — averaged far less. Against the 24% year-over-year decline, June's uptick looks like noise within a secular price compression that has been grinding since late 2024.

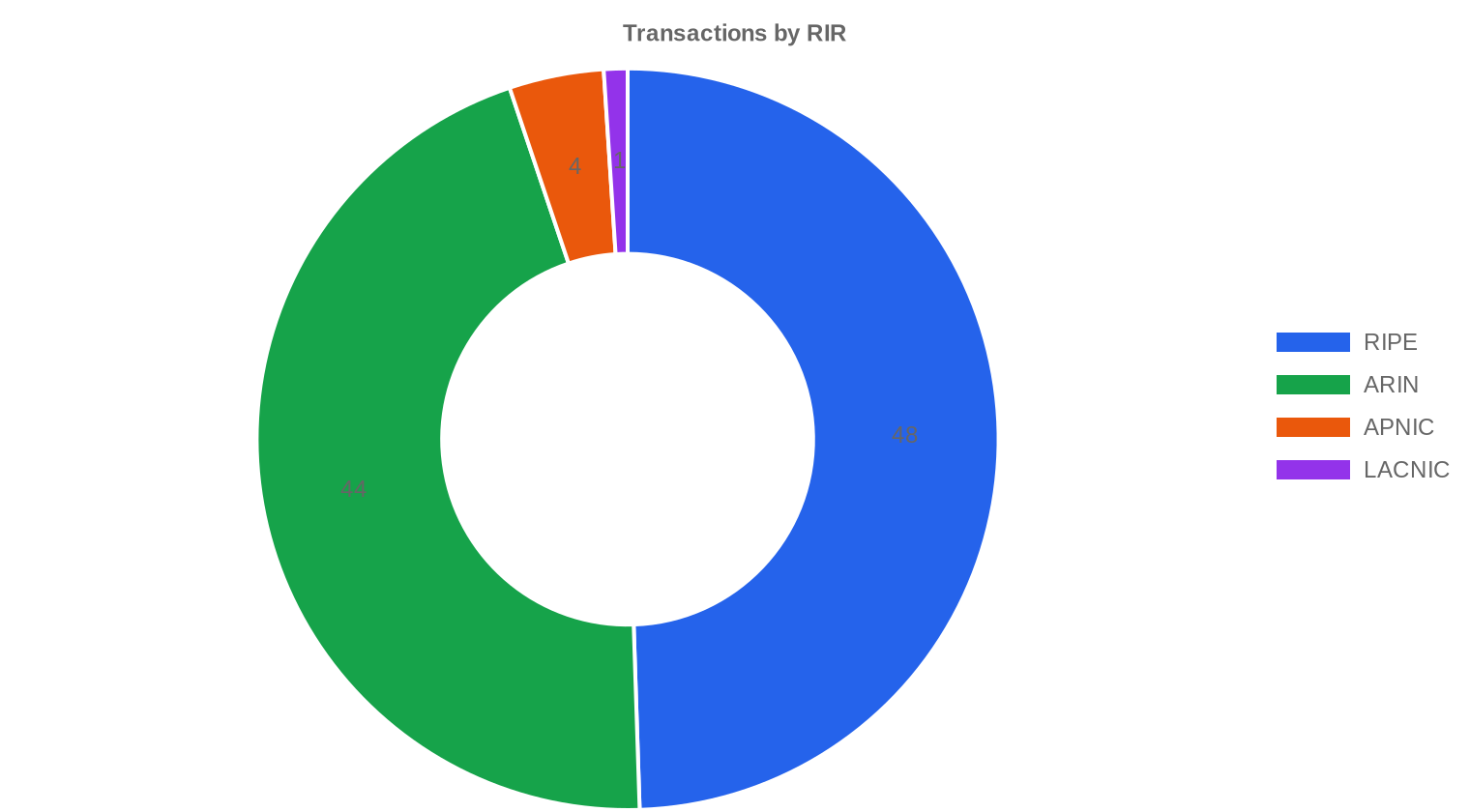

Pricing by RIR

RIPE held 49.5% of transaction volume with 48 deals but accounted for only 97,792 IPs — small blocks at premium prices. ARIN moved the real tonnage: 480,512 IPs across 44 deals at a $19.25 average, well below RIPE's $23.20. The gap between RIPE and ARIN pricing has narrowed relative to 2024 peaks but remains meaningful at roughly $4 per IP. LACNIC posted the highest per-IP price at $25.50 on a single 1,024-address transaction, a scarcity premium on a thin market. APNIC was similarly sparse with four deals averaging $24.75. RIPE NCC: $23.20 per IP across 48 transactions (49.5% of deal count). ARIN: $19.25 per IP across 44 transactions (82.8% of IP volume). APNIC: $24.75 per IP across 4 transactions (0.2% of IP volume). LACNIC: $25.50 per IP across 1 transaction (0.2% of IP volume). AFRINIC: No recorded transactions.| RIR | Transactions | Avg $/IP | Median $/IP | IPs Traded | RIR Transfers | Next Month (proj.) | Year-End (proj.) |

|---|---|---|---|---|---|---|---|

| RIPE | 48 | $23.20 | $23.22 | 97,792 | 93 | $23.50 | $24.00 |

| ARIN | 44 | $19.25 | $17.75 | 480,512 | 235 | $17.50 | $17.00 |

| APNIC | 4 | $24.75 | $23.00 | 1,280 | 0 | $22.00 | $21.00 |

| LACNIC | 1 | $25.50 | $25.50 | 1,024 | 0 | $25.00 | $24.00 |

Transaction Volume

Supply & Block Sizes

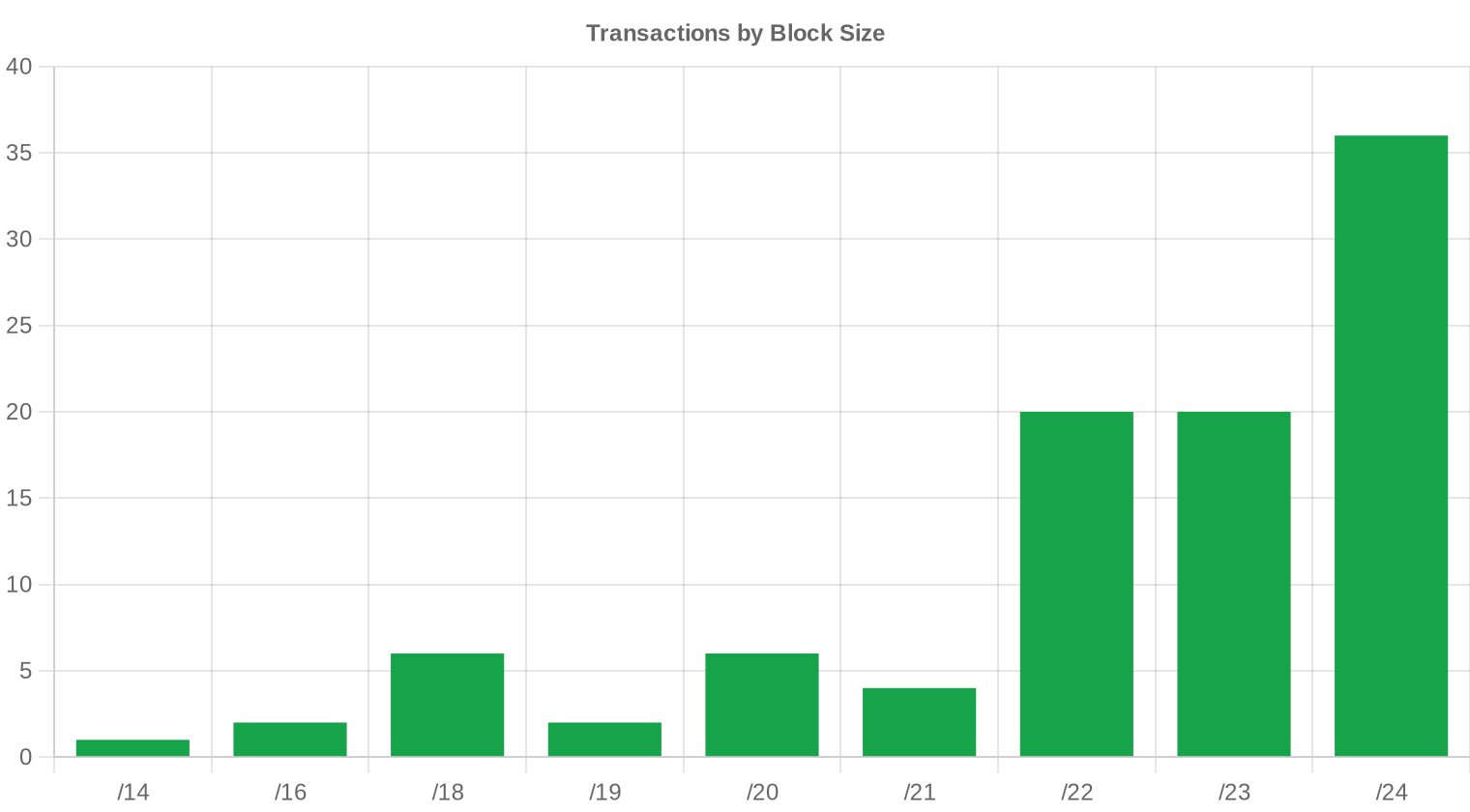

/24 blocks dominated once again with 36 transactions — 37% of all deals. That concentration is structural: /24s are the minimum BGP-routable unit, and most mid-market buyers — hosting companies, regional ISPs, enterprises spinning up edge infrastructure — need exactly one or two subnets, not a /16. The remaining 61 deals spread across larger prefixes, with three $1M-plus deals almost certainly involving /16 or larger blocks from ARIN's legacy pool.

Geographic Activity

The US accounted for 40 of 97 transactions, a 41% share that reflects ARIN's dominance in bulk IP volume. The UK came in second with 19 deals — a disproportionate share relative to GDP, driven by London's role as a hosting and cloud hub. Canada placed third at 7, with Germany (4), Sweden (3), and a handful of others rounding out a 16-country buyer pool. The geographic distribution skews Anglophone and Northern European, consistent with patterns observed over the past three years.Registry Transfer Activity

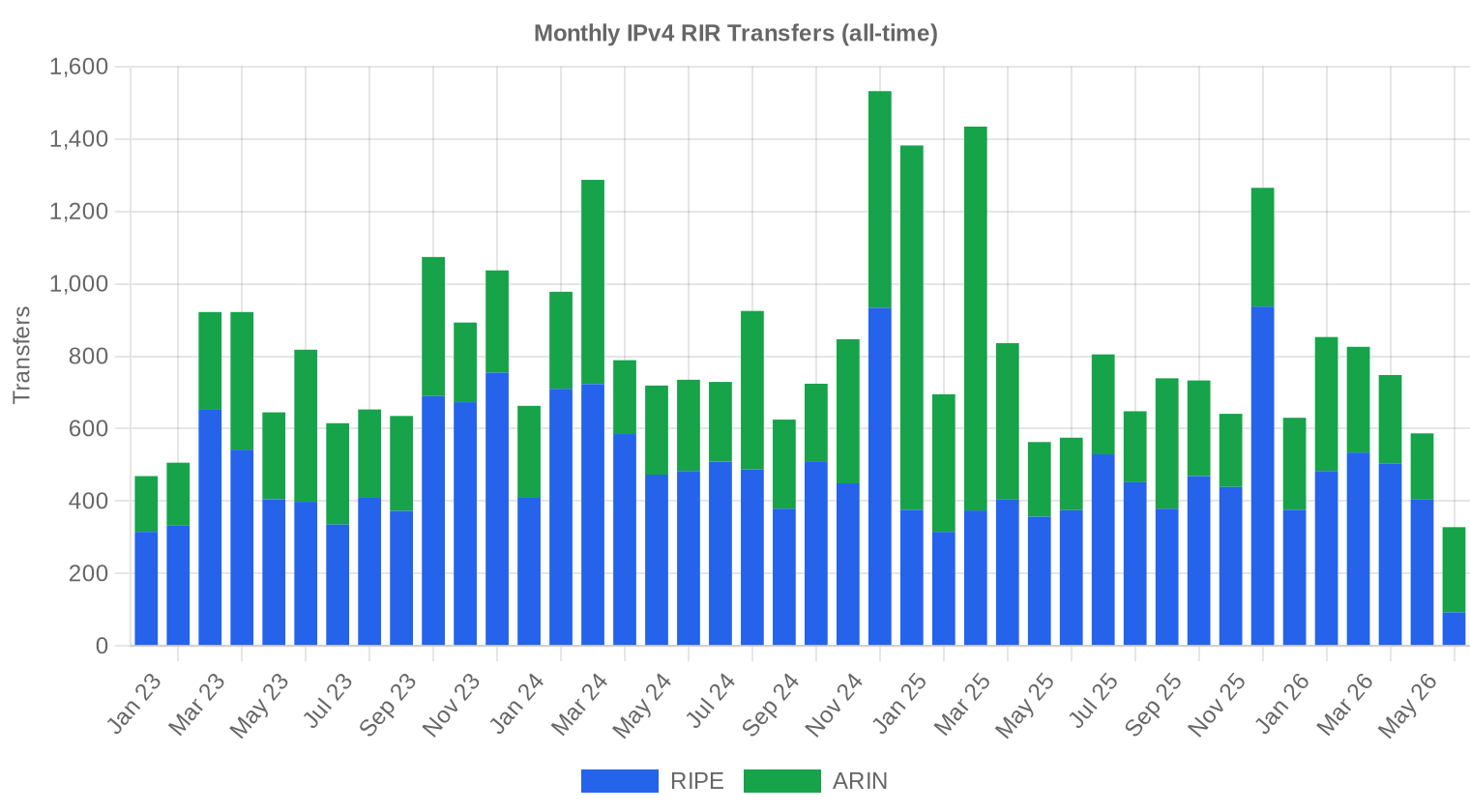

RIR-recorded transfers totaled 328 in June, significantly higher than the 97 priced transactions in our dataset — the gap reflects inter-company transfers, M&A-related reassignments, and deals where pricing was not disclosed. ARIN led with 235 transfers (71.6%), while RIPE logged 93. Neither APNIC, LACNIC, nor AFRINIC registered any transfers this month.Long-Run Transfer Trends

Over the 42-month tracking window, 34,030 total transfers have been recorded across all RIRs. RIPE has accounted for 59.7% of that cumulative total versus ARIN's 40.3% — a split that reflects RIPE's more fragmented block landscape and higher transaction frequency. The peak month for transfer activity was December 2024, consistent with year-end tax and budget-cycle motivations that have historically driven Q4 spikes.| RIR | RIR Transfers |

|---|---|

| RIPE | 20,329 |

| ARIN | 13,701 |

| RIR Transfers | 34,030 |

Outlook & Forecast

Forecasting each block-size band and RIR separately with our AI model:

The overall average price per IP is projected to reach $20.44 by December 2026, with a next-month estimate of $20.83 per IP.

- RIPE: projected at $23.50 per IP next month, trending toward $24.00 by December 2026.

- ARIN: projected at $17.50 per IP next month, trending toward $17.00 by December 2026.

- APNIC: projected at $22.00 per IP next month, trending toward $21.00 by December 2026.

- LACNIC: projected at $25.00 per IP next month, trending toward $24.00 by December 2026.

- AFRINIC: insufficient data for a reliable forecast.

Forecast by Block Size

| Block | Current $/IP | Next Month | Year-End | Confidence |

|---|---|---|---|---|

| /24 | $26.00 | $26.00 (0.0%) | $25.50 (-1.9%) | medium |

| /23 | $20.00 | $20.50 (+2.5%) | $20.00 (0.0%) | medium |

| /22 | $17.00 | $17.00 (0.0%) | $16.50 (-2.9%) | medium |

| /21 | $17.70 | $17.50 (-1.1%) | $17.00 (-4.0%) | low |

| /20 | $15.75 | $15.75 (0.0%) | $16.00 (+1.6%) | low |

| /19 | $14.25 | $14.50 (+1.8%) | $14.00 (-1.8%) | low |

| /18-/16 | $13.50 | $13.50 (0.0%) | $14.00 (+3.7%) | low |

| /15-up | $10.00 | $10.00 (0.0%) | $10.50 (+5.0%) | low |

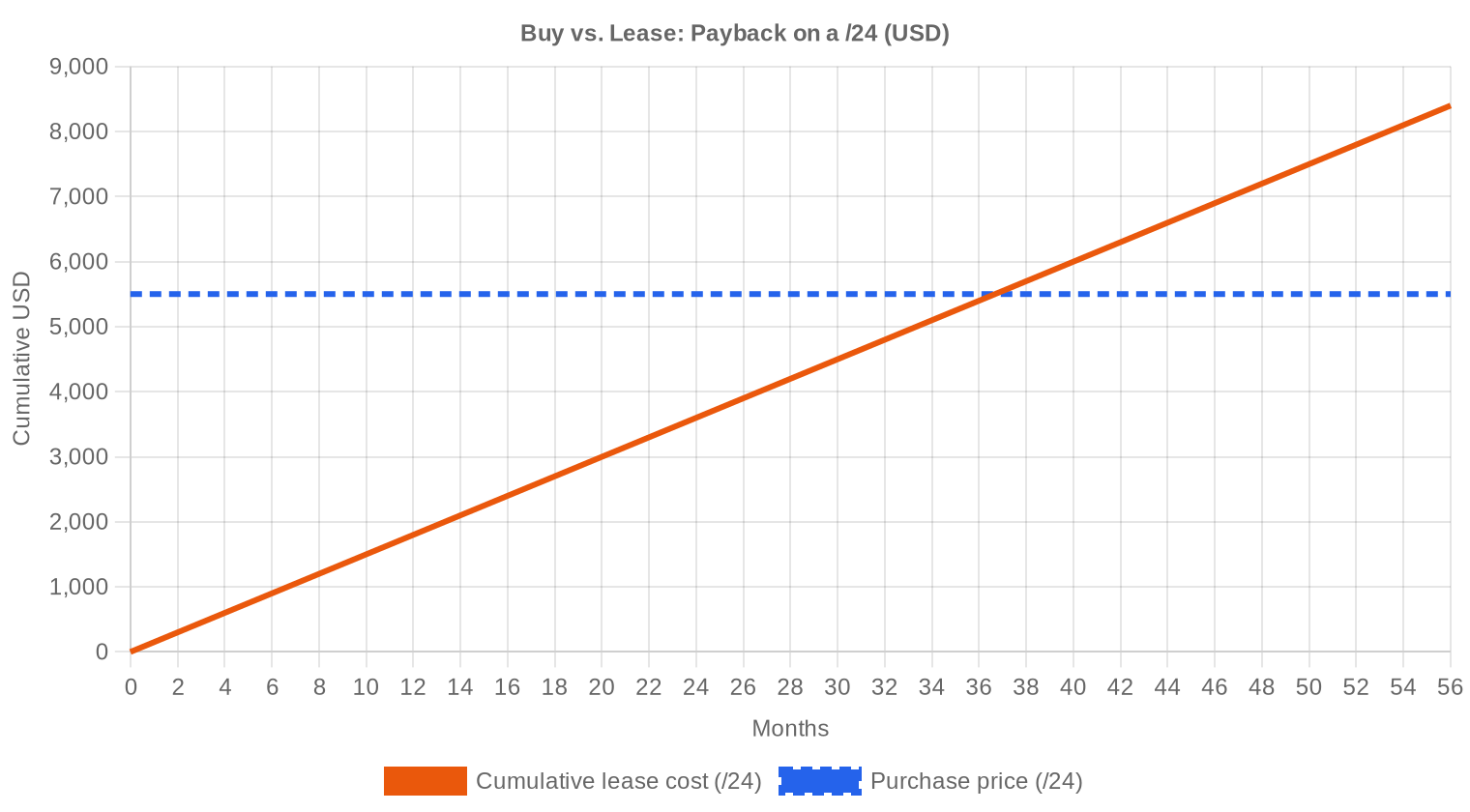

Editor's Take: Buy vs. Lease

The buy-versus-lease math is unambiguous this month. At $21.49 per IP and a lease rate of $0.5859 per IP per month, the breakeven on a purchase occurs at 36.7 months — just over three years. For any organization with a planning horizon beyond 2029, buying is the clear play. At a /24 level, the numbers are $5,501 to buy versus $150 per month to lease, yielding the same 36.7-month payback. The implied annual yield for a block holder leasing at current rates is 32.7%, a return that dwarfs fixed income and rivals private equity vintage years. Buyers who secured addresses at $28-$35 per IP in 2023-2024 are underwater on a mark-to-market basis, but those blocks still generate the same lease income — the yield on cost at those entry points remains north of 20%.| /24 Purchase price | $5,501 |

| /24 Lease price | $150 / mo |

| Payback period | 36.7 mo (3.1 yr) |

| Gross annual yield | 32.7% |

What This Means for You

Buyers: The 24% year-over-year price decline means you are buying at the cheapest levels since early 2022. The forecast suggests another 5% downside by year-end. Rushing is unnecessary, but waiting for a crash is speculative — the floor is approaching at or near current ARIN bulk pricing around $17-19. Sellers: If you hold legacy ARIN blocks and have been waiting for a bounce, the data does not support that thesis. Prices are down 24% year-over-year and the model projects continued softness. Monetize now or lease the blocks and collect the 32.7% yield. Lessees: Monthly lease rates at $0.59 per IP are stable, but the buy-versus-lease breakeven at 36.7 months makes leasing a poor long-term strategy for anyone with capital access. Leasing remains correct for short-term projects or organizations that cannot justify the upfront spend. Block holders: A 32.7% annual yield on leased addresses is exceptional. The risk is asset depreciation — addresses bought at $30+ are now worth $21.49 on the open market. Leasing offsets that decline and then some, but holders should monitor the convergence between buy and lease pricing closely.Browse verified IPv4 blocksSell IPv4 →

List your blocks with managed transferLease IPv4 →

Flexible short-term capacityLease Out IPv4 →

Turn idle blocks into recurring revenue

IPv4 Pricing by Block Size

Per-IP premiums on /24 blocks remain significant. A clean /24 in RIPE trades at $23-$25 per IP — roughly $5,900-$6,400 per block — while bulk /16 pricing through ARIN comes in at $17-$19 per IP, a 20-25% discount. The premium for small blocks reflects the BGP-routability floor and the fact that most mid-market buyers need exactly 256 addresses. Larger blocks command volume discounts but require buyers with the network infrastructure and justification to deploy them.| Block | IPs | Buy: /IP | Buy: Total | Lease: /IP/mo | Lease: Monthly |

|---|---|---|---|---|---|

| /24 | 256 | $35–45 | $8,960–11,520 | $0.38–0.50 | $97–128 |

| /22 | 1,024 | $28–38 | $28,672–38,912 | $0.33–0.45 | $338–461 |

| /20 | 4,096 | $22–32 | $90,112–131,072 | $0.30–0.40 | $1,229–1,638 |

| /18 | 16,384 | $20–30 | $327,680–491,520 | $0.30–0.38 | $4,915–6,226 |

| /16 | 65,536 | $18–28 | $1,179,648–1,835,008 | $0.30–0.35 | $19,661–22,938 |

IPv4 Price History: 2011–2026

When IANA exhausted its free pool in 2011, IPv4 addresses were essentially worthless on the secondary market — early transfers priced below $5 per IP. Prices climbed steadily through the 2010s, accelerated during the pandemic-era infrastructure boom, and peaked above $50 per IP in RIPE markets during late 2023. AWS's decision to charge $0.005 per hour for public IPv4 addresses (roughly $3.60/month) introduced a pricing anchor that pressured the market throughout 2024. The current $21.49 average reflects a market that has bifurcated: RIPE blocks command premiums due to scarcity and the 24-month holding rule, while ARIN bulk pricing has settled into the high teens.| Year | ~Price/IP | Key Event |

|---|---|---|

| 2011 | $7–12 | IANA free pool exhausted; Microsoft/Nortel deal ($11.25/IP) |

| 2012 | $8–12 | RIPE NCC reaches last /8; begins /22-only allocation |

| 2014 | $10–15 | LACNIC free pool exhausted |

| 2015 | $8–15 | ARIN free pool exhausted |

| 2017–18 | $12–18 | Leasing market grows; cloud demand rises |

| 2019 | $18–24 | RIPE NCC exhausts remaining free pool |

| 2021–22 | $50–60+ | Post-pandemic peak; hyperscaler build-outs |

| 2024 | $35–52 | AWS IPv4 charge ($0.005/IP/hr); large block correction |

| 2025–26 | $18–45 | Market bifurcation; /16s below $20 for first time since 2019 |

Market Structure: Who Is Buying & Selling

Buy-side activity remains concentrated among cloud infrastructure providers, hosting companies, and regional ISPs — organizations that need routable space and cannot rely solely on NAT or IPv6 in production environments. Sell-side inventory comes primarily from legacy holders — corporations, universities, and government agencies sitting on /16 or larger allocations they never fully utilized. Bankruptcy-related divestitures and corporate restructurings continue to release blocks, though the flow is lumpy and unpredictable.IPv4 vs. Other Asset Classes

At a 32.7% implied annual yield, leased IPv4 addresses outperform virtually every conventional asset class. U.S. Treasuries yield 4-5%, investment-grade corporates offer 5-6%, and even well-located commercial real estate rarely exceeds 8% cap rates. The catch is asset depreciation: addresses bought at today's $21.49 may be worth $18-20 by year-end per our model, eroding capital gains. Still, the net return — lease income minus price decline — remains strongly positive for holders who entered at lower basis points.| Asset Class | Typical Yield | Liquidity | Primary Risk |

|---|---|---|---|

| IPv4 | 32.7% | Moderate | IPv6 adoption, block quality |

| Commercial Real Estate | 5–8% | Low | Vacancy, rate cycle |

| Investment-Grade Bonds | 4–5% | High | Duration, credit risk |

| S&P 500 | ~1,3% | High | Market volatility |

| Money Market / T-Bills | ~4–5% | High | Rate cycle changes |

IPv6 Adoption & Why IPv4 Remains Essential

IPv6 adoption continues its glacial trajectory. Google's measurements show roughly 45% of traffic reaching its services over IPv6, but enterprise adoption lags badly — most internal networks, legacy applications, and B2B integrations remain IPv4-dependent. The dual-stack reality will persist for at least another decade, and probably longer. IPv4 is not dying; it is slowly becoming more expensive to avoid than to simply buy.AI & Cloud Infrastructure Demand

AI infrastructure buildout is a growing but still secondary driver of IPv4 demand. Training clusters themselves are largely internal-network operations, but inference farms — particularly those serving API endpoints at scale — require public-facing IPv4 space. The major hyperscalers already hold massive reserves, but second-tier AI companies and GPU cloud startups are active buyers in the /22 to /20 range. This demand wedge is real but has not yet moved aggregate pricing.What Determines IPv4 Block Value

Block valuation depends on five variables in rough order of importance: RIR region, block cleanliness (blacklist and spam database status), allocation age, prefix size, and transferability. A RIPE /22 with clean history commands $23+ per IP; the same prefix size from ARIN with blacklist entries might trade at $14-16. Blocks with legacy allocations (pre-RIR era) sometimes carry additional complexity around transfer eligibility, which can depress pricing by 10-15%.Sell vs. Lease: A Decision Framework

Current market conditions favor leasing for holders who can tolerate the administrative overhead. At $0.59 per IP per month and a 32.7% annual yield, leasing generates income that exceeds the likely pace of asset depreciation. Selling makes sense for holders who need liquidity immediately, want to avoid ongoing management, or believe prices will decline faster than the model projects. The breakeven calculation at 36.7 months means a holder who leases for three years earns back the full current market value of the block.| /24 Purchase price | $5,501 |

| /24 Lease price | $150 / mo |

| Payback period | 36.7 mo (3.1 yr) |

| Gross annual yield | 32.7% |

RIPE NCC 24-Month Transfer Restriction

RIPE NCC's 24-month holding requirement restricts newly acquired blocks from being resold for two years, effectively locking up supply and creating a structural price premium over ARIN. The rule was designed to prevent speculation, and it works — but the side effect is a persistently tighter RIPE market where /24s trade at $23+ while comparable ARIN blocks go for $17-19. For buyers, this means RIPE blocks carry an embedded illiquidity premium that should be factored into total cost of ownership.Deal Size Distribution

The average deal size jumped to 74,033 IPs in June, up 35% from May's 54,716 and down 10% from the year-ago figure of 82,665. The distribution is heavily skewed: 80 of 97 deals (82%) fell under $50K in value, accounting for only $1.03 million. The other 17 deals generated $11.44 million — with three transactions over $1 million alone worth $8.45 million. This kind of top-heaviness is normal in the IPv4 market, where a handful of large ARIN block transfers dominate dollar volume while the /24 and /23 market drives transaction count.Top Trading Countries

The United States dominated with 40 deals, reflecting the depth of the ARIN market and the concentration of cloud, hosting, and enterprise buyers in North America. The UK's 19 transactions — nearly 20% of total deal count — continue a multi-year trend driven by London's status as Europe's primary data center and connectivity hub. Canada's 7 deals round out a North American bloc that collectively accounts for nearly half of all transactions. Germany and Sweden provide modest European diversification but at volumes that do not meaningfully influence pricing.BEAD Broadband Program Impact

The $42.45 billion BEAD broadband program is beginning to generate IPv4 procurement activity as state-level grant recipients finalize network designs. Most BEAD-funded ISPs need /20 to /18 blocks to serve rural deployments, and these mid-size allocations are precisely the segment where supply is thinnest. We expect BEAD-related demand to become visible in transaction data by late 2026 or early 2027, with potential to tighten supply in the $17-22 per IP range that dominates ARIN bulk pricing.Hyperscaler IPv4 Holdings

Amazon, Microsoft, and Google collectively hold tens of millions of IPv4 addresses — Amazon alone controls an estimated 100+ million. These reserves insulate the hyperscalers from market pricing, but their decisions to charge customers for IPv4 usage (AWS's $3.60/month per IP) create downstream demand effects as smaller operators weigh buying their own blocks versus paying per-hour cloud fees. Any significant release of hyperscaler-held blocks onto the secondary market would be deflationary, but none of the three have shown any inclination to divest.Macroeconomic Conditions & Market Impact

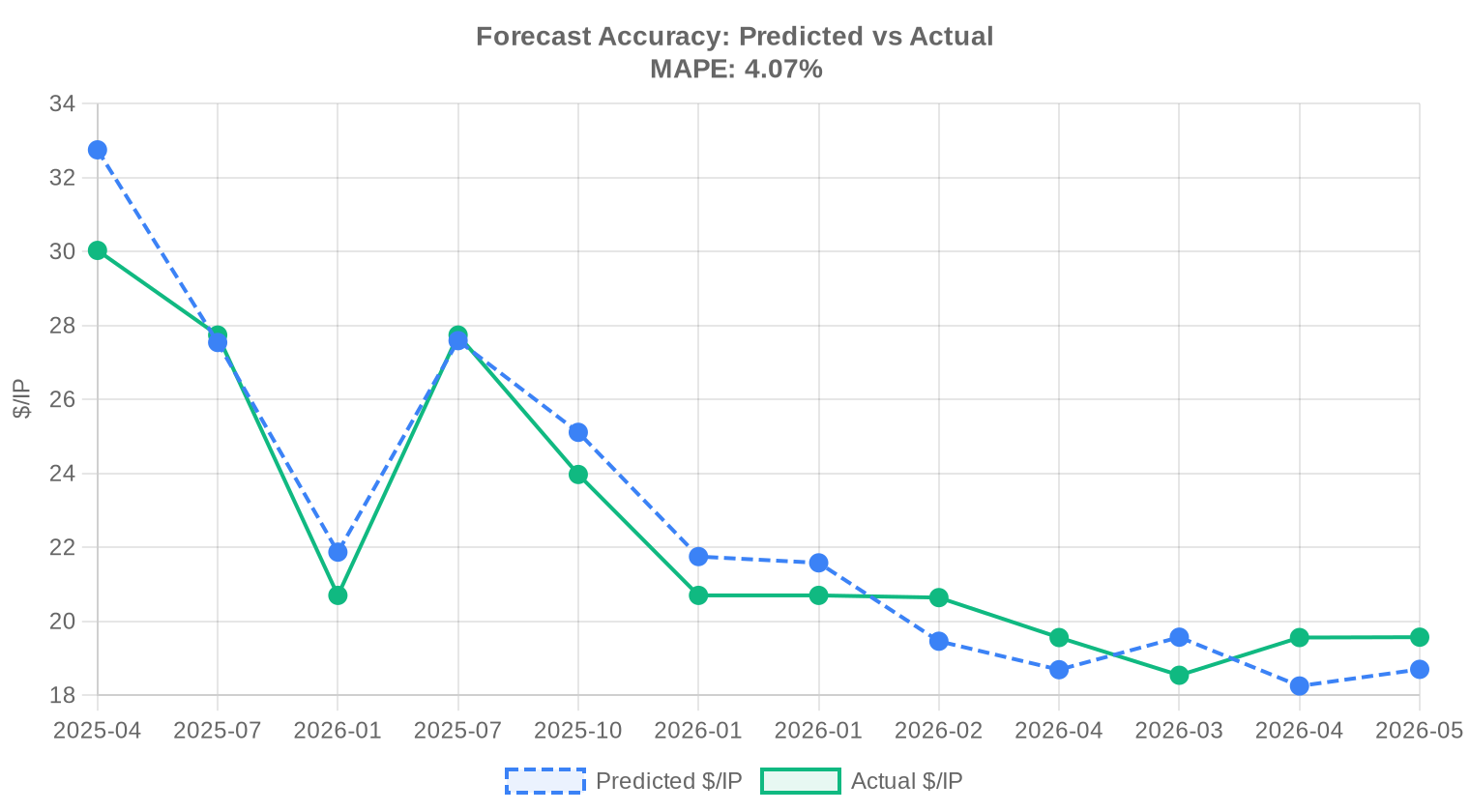

The rate environment in mid-2026 remains moderately restrictive, with the Fed holding steady and enterprise IT budgets growing at low single digits. Higher rates increase the opportunity cost of tying up capital in IPv4 blocks, which partly explains the 24% year-over-year price decline — at 5% risk-free rates, a non-yielding asset needs a stronger thesis. Organizations with leasing strategies or immediate deployment needs are less sensitive to rate effects, which is why lease pricing has held steady even as purchase prices have fallen.Model Update & Calibration

We reviewed our past projections against actual market outcomes and recalibrated the model for this report. The updated model places more weight on recent price movements using exponential decay, dynamically adjusts prediction bands to reflect current market conditions, and corrects for any systematic bias detected in earlier forecasts. The predicted-vs-actual comparison chart below shows how closely our past estimates tracked reality.

| Report Period | Target Month | Predicted | Actual | Deviation |

|---|---|---|---|---|

| 2025-Q4 | 2026-01 | $22 | $21 | +4% |

| 2026-01 | 2026-02 | $19 | $21 | -6% |

| 2026-Q1 | 2026-04 | $19 | $20 | -4% |

| 2026-02 | 2026-03 | $20 | $19 | +6% |

| 2026-03 | 2026-04 | $18 | $20 | -7% |

| 2026-04 | 2026-05 | $19 | $20 | -4% |

Methodology

Figures are based on completed IPv4Center marketplace transactions and RIR transfer statistics. Prices are in US dollars per IP address. Forecasts are produced by an AI model that analyses each block-size band and RIR segment separately (with outlier-trimmed medians) alongside known market catalysts; they are estimates, not guarantees.

Data Sources

- Hilco Streambank — Completed auction transaction records

- RIPE NCC — Inter-RIR and intra-RIR transfer statistics

- ARIN — North American transfer reports and waiting list data

- APNIC — Asia-Pacific transfer records

- LACNIC — Latin American and Caribbean transfer data

- IPv4Center.com — Proprietary marketplace transaction and lease pricing data

This report is generated automatically for informational purposes only and does not constitute financial advice.

Frequently Asked Questions

What was the average IPv4 price in June 2026?

The weighted average was $21.49 per IP address, with a median of $20 per IP across 97 recorded transactions.

How much does a /24 block of IPv4 addresses cost in June 2026?

At the June 2026 average of $21.49 per IP, a /24 block (256 addresses) costs approximately $5,501. RIPE /24s trade higher at roughly $5,940 per block.

How much has IPv4 pricing declined year-over-year?

The June 2026 average of $21.49 is 24% below the June 2025 average, representing a significant annual decline driven by increased supply and macroeconomic factors.

Which RIR has the cheapest IPv4 addresses?

ARIN blocks averaged $19.25 per IP in June 2026, the lowest among active regions. RIPE averaged $23.20, APNIC $24.75, and LACNIC $25.50.

Why are RIPE IPv4 addresses more expensive than ARIN?

RIPE's 24-month holding rule restricts resale of newly acquired blocks, constraining supply. European blocks also benefit from strong demand from hosting and cloud providers operating in the region.

How many IPv4 addresses were traded in June 2026?

A total of 580,608 IPv4 addresses changed hands across 97 transactions, generating $7.18 million in total value.

What is the current IPv4 lease rate?

The average monthly lease rate is $0.5859 per IP, or approximately $150 per month for a /24 block. The annualized rate is $7.03 per IP.

Is it better to buy or lease IPv4 addresses right now?

At current prices, buying breaks even versus leasing in 36.7 months (about 3.1 years). For organizations with a planning horizon beyond three years, buying is the more cost-effective option.

What is the expected IPv4 price by end of 2026?

Our model projects an average of $20.44 per IP by December 2026, representing approximately 5% downside from current levels. The forecast is rated as reliable.

What is the annual yield on leasing IPv4 addresses?

Based on June 2026 data, the implied annual yield for a block holder leasing addresses is 32.7%, calculated from a buy price of $21.49 and monthly lease revenue of $0.5859 per IP.

How long does an IPv4 transfer take?

Typical ARIN transfers complete in 2-4 weeks. RIPE transfers can take 3-6 weeks due to additional verification steps. Using an experienced broker and escrow service can reduce delays.

What is the most traded IPv4 block size?

/24 blocks accounted for 36 of 97 transactions in June 2026 (37%), making them the most frequently traded prefix size. They represent the minimum BGP-routable allocation.

Which countries are most active in IPv4 trading?

The US led with 40 transactions (41%), followed by the UK with 19 (20%) and Canada with 7 (7%). These three countries accounted for 68% of all deals.

What mistakes should be avoided when buying IPv4 addresses?

The most common mistakes are skipping blacklist and spam database checks, not verifying transfer eligibility with the RIR, and failing to use escrow. Any of these can result in acquiring unusable or legally encumbered addresses.

What are the risks of skipping blacklist verification before purchasing IPv4?

Blocks with blacklist entries can be rejected by major transit providers and email services, rendering them functionally useless for many applications. Cleaning a block's reputation can take 3-6 months and is not guaranteed to succeed.

Why shouldn't you skip escrow when buying IPv4 addresses?

Without escrow, there is no mechanism to ensure the seller actually transfers the block before receiving payment. IPv4 fraud — taking payment without completing the RIR transfer — is a documented risk, and escrow eliminates it entirely.

What risks should IPv4 investors be aware of?

Key risks include continued price depreciation (down 24% year-over-year), potential RIR policy changes that could restrict transfers, and the long-term possibility that IPv6 adoption reduces IPv4 demand — though that remains a multi-decade timeline.

What happens if I buy an IPv4 block with a poor reputation?

Blocks listed on major blacklists (Spamhaus, CBL, etc.) may be rejected by upstream providers or trigger spam filters when used for email. Due diligence before purchase is critical — remediation after the fact is time-consuming and sometimes impossible.

How does RIPE's 24-month holding rule affect buyers?

If you buy a RIPE block, you cannot resell it for 24 months. This limits liquidity and means RIPE purchases should be viewed as medium-term commitments, not short-term trades.

What is the price difference between a /24 and a /16?

In June 2026, /24 blocks traded at a premium of 20-25% per IP versus /16 blocks. A /24 at RIPE pricing costs roughly $5,940 while a /16 at ARIN bulk rates runs approximately $1.26 million ($19.25 × 65,536 IPs).

How does the BEAD program affect IPv4 demand?

The $42.45 billion BEAD broadband program is generating new demand for mid-size blocks (/20 to /18) as rural ISP grant recipients build out networks. This demand is expected to become more visible in market data by late 2026.

Is IPv4 a good investment in 2026?

IPv4 blocks leased at current rates yield 32.7% annually, far exceeding bonds and most real estate. However, the underlying asset is depreciating — prices are down 24% year-over-year — so net returns depend heavily on entry price and lease income stability.

Will IPv4 prices continue to fall?

Our model projects a year-end price of $20.44, suggesting modest continued softness. The pace of decline has slowed considerably compared to 2024-2025, and the market appears to be approaching a floor in the high teens for ARIN blocks.

What drives the price difference between RIRs?

Supply constraints (RIPE's holding rule), regional demand intensity (European hosting market), and transfer complexity all contribute. ARIN's larger available inventory and simpler transfer process result in consistently lower per-IP pricing.

How does AI infrastructure affect IPv4 demand?

AI inference farms serving public API endpoints require IPv4 space, and second-tier AI companies are active buyers in the /22 to /20 range. Training clusters use private addressing and do not directly drive IPv4 demand.

What is the minimum routable IPv4 block?

A /24 (256 addresses) is the minimum block size that most ISPs will accept in BGP routing tables. Smaller blocks are generally not routable on the public internet.

How do I verify an IPv4 block is clean before buying?

Check major blacklists (Spamhaus, CBL, Barracuda), review the block's history in abuse databases, verify RIR registration records, and confirm that no active routing announcements conflict with the block. A reputable broker will handle this due diligence.

What was the total value of IPv4 transactions in June 2026?

Total recorded transaction value was $7.18 million across 97 deals, with an average deal size of 74,033 IP addresses.

Can I sell my IPv4 block immediately after buying it?

Under ARIN, yes — there is no mandatory holding period. Under RIPE NCC, you must hold the block for 24 months before it can be transferred again. Other RIRs have varying policies.

What is the forecast for IPv4 prices next month?

Our model projects an average of $20.83 per IP for July 2026, a modest decline from June's $21.49. The forecast carries a reliable confidence rating.