9 min read

This report analyzes the IPv4 transfer market for February 2026, based on completed IPv4Center marketplace transactions and official RIR transfer records.

Executive Summary

The February 2026 market recorded 94 IPv4 transactions — 868,864 addresses changed hands at an average of $20.64 per IP, representing an estimated $10,113,379 in total transaction volume.

Against January 2026, per-IP pricing dropped 0.3% to $20.64. The directional move aligns with broader market repricing.

That marks a 38.4% move (dropped) from February 2025 levels, with the average settling at $20.64.

ARIN blocks traded at a premium: $21.37 per IP, well above the market-wide median of $21.75.

Market Overview

| Transactions | 94 |

| IP Addresses Traded | 868,864 |

| Estimated Market Value | $10,113,379 |

| Average Price / IP | $20.64 |

| Median Price / IP | $21.75 |

| RIR Transfers | 853 |

Year-over-Year Comparison

| Metric | This period | A year earlier (February 2025) | Change |

|---|---|---|---|

| Transactions | 94 | 47 | +100.0% |

| IP Addresses Traded | 868,864 | 437,504 | +98.6% |

| Estimated Market Value | $10,113,379 | $14,043,587 | -28.0% |

| Average Price / IP | $20.64 | $33.49 | -38.4% |

| RIR Transfers | 853 | 695 | +22.7% |

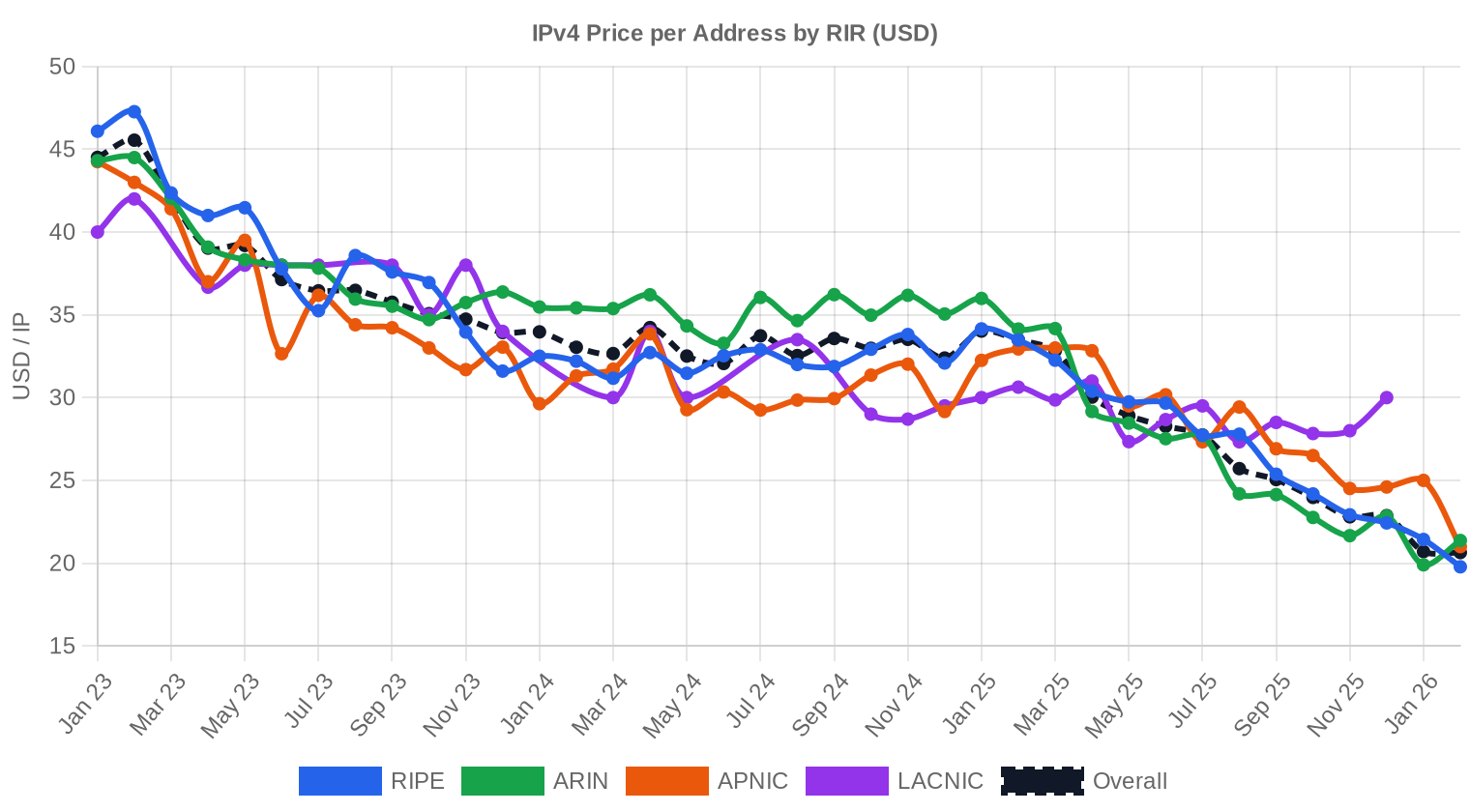

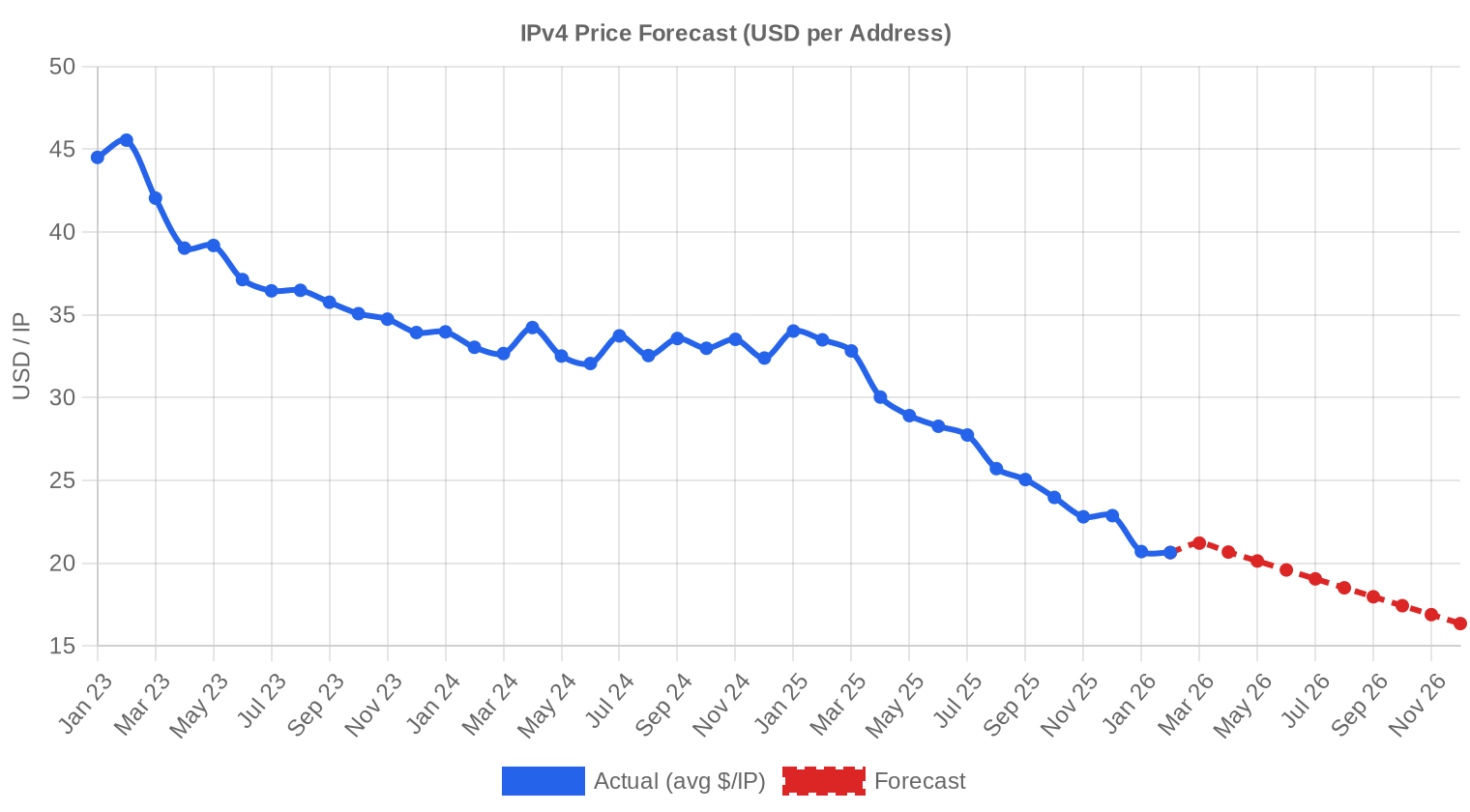

Price Dynamics

Per-IP pricing softened a bit over the observed window. The spread: $9.50 to $38.50 per address, with block cleanliness, size, and RIR origin driving divergence.

Regression analysis indicates a monthly drift of approximately 2.5% (dropped).

Pricing by RIR

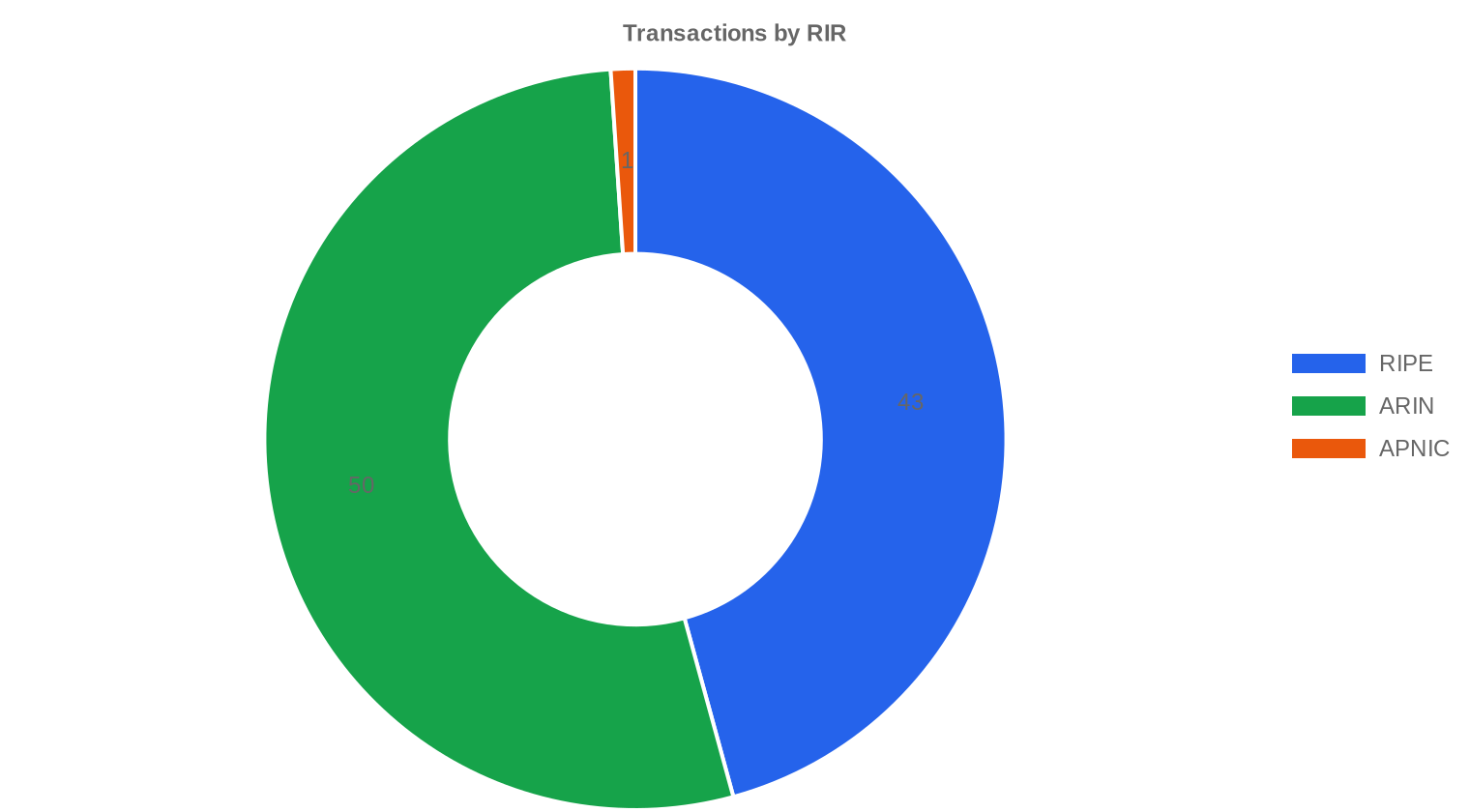

The RIR breakdown for February 2026 reveals clear pricing stratification:

- RIPE: $19.78 per IP across 43 transactions (45.7% of volume).

- ARIN: $21.37 per IP across 50 transactions (53.2% of volume).

- APNIC: $21.00 per IP across 1 transactions (1.1% of volume).

| RIR | Transactions | Avg $/IP | Median $/IP | IPs Traded | RIR Transfers | Next Month (proj.) | Year-End (proj.) |

|---|---|---|---|---|---|---|---|

| RIPE | 43 | $19.78 | $21.00 | 656,640 | 483 | $19.16 | $14.64 |

| ARIN | 50 | $21.37 | $22.50 | 211,968 | 370 | $20.94 | $18.11 |

| APNIC | 1 | $21.00 | $21.00 | 256 | 0 | $21.92 | $14.71 |

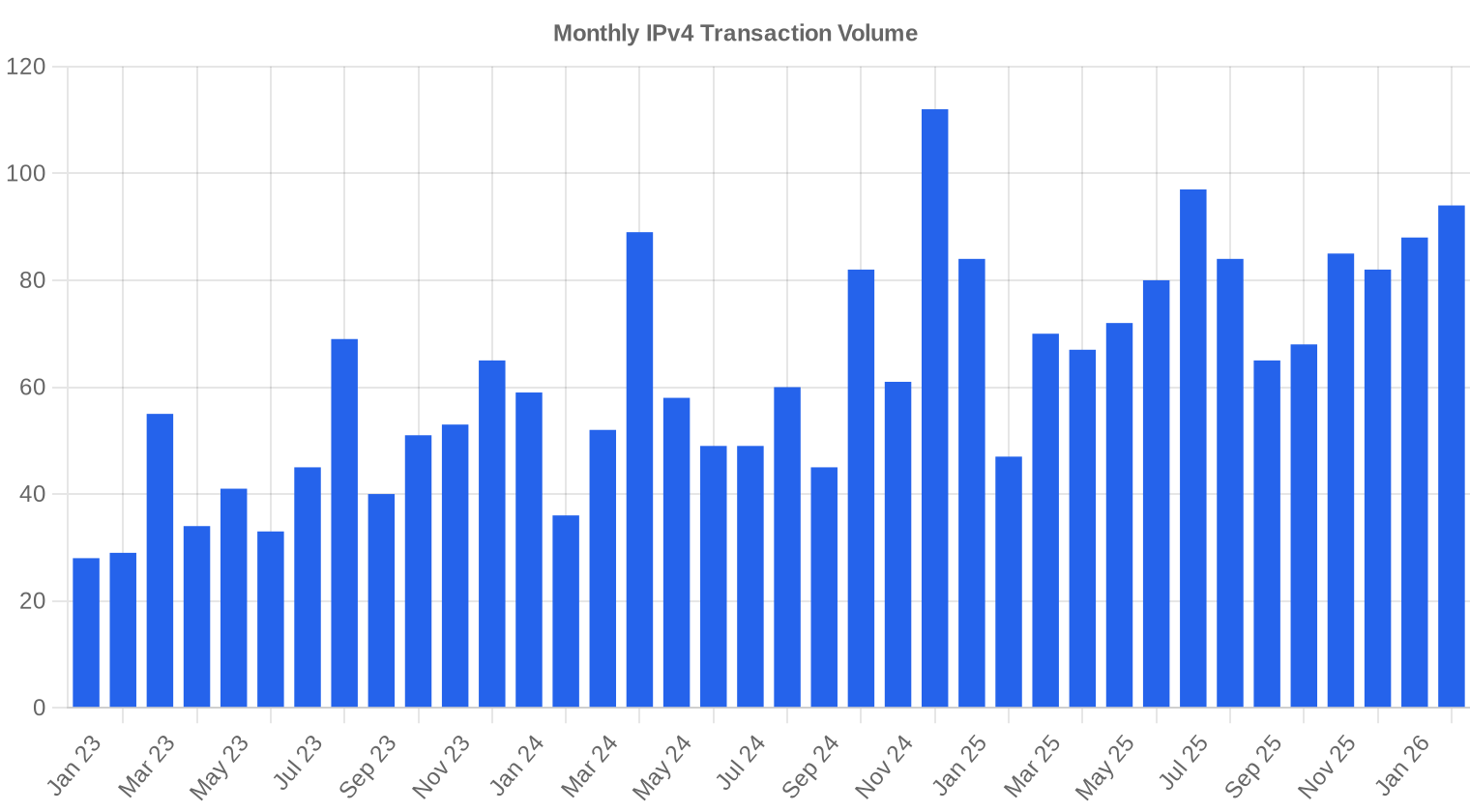

Transaction Volume

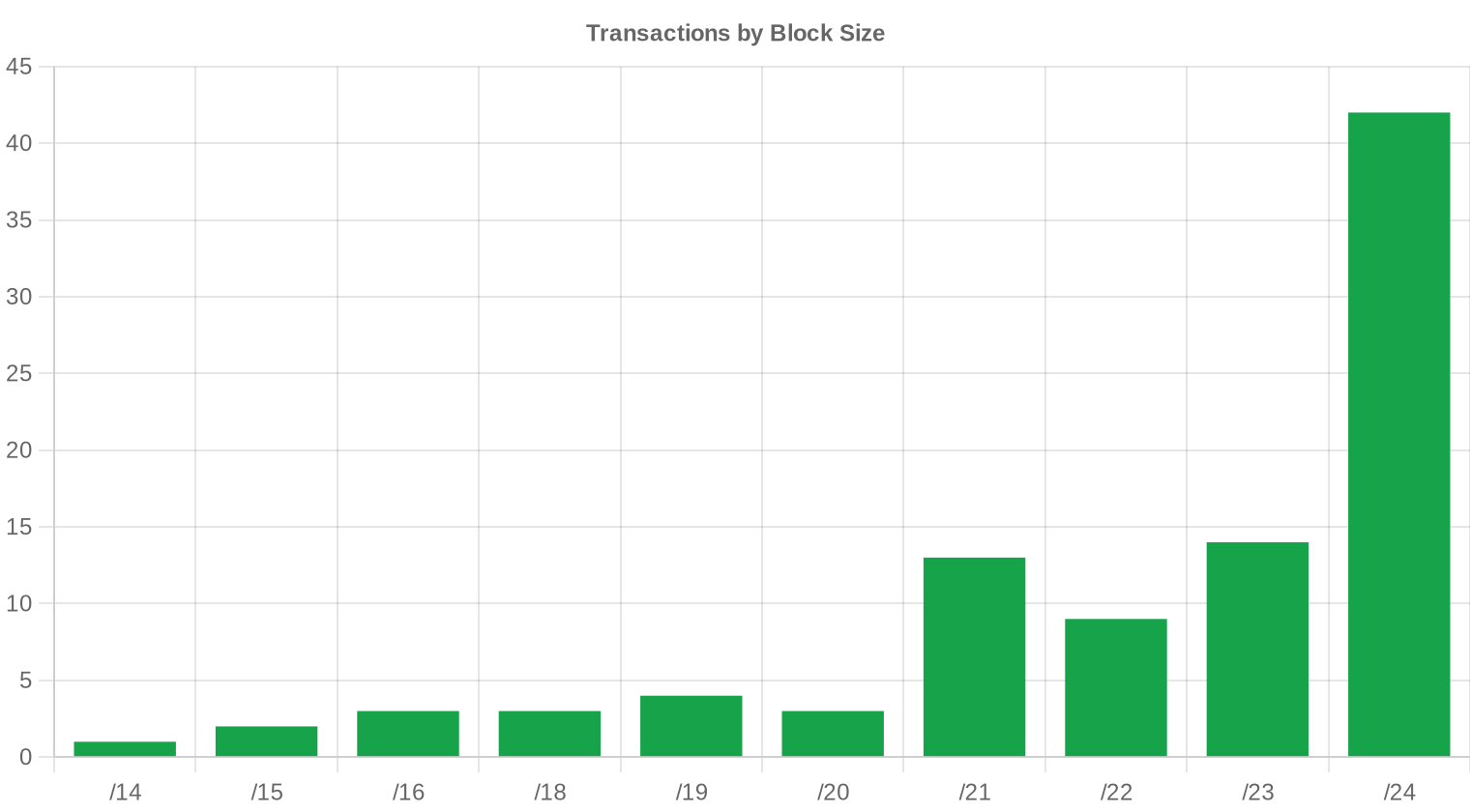

Supply & Block Sizes

/24 blocks dominated trading activity with 42 completed deals — the market's primary liquidity band.

Geographic Activity

The most active jurisdictions by traded block volume: US, GB, NL.

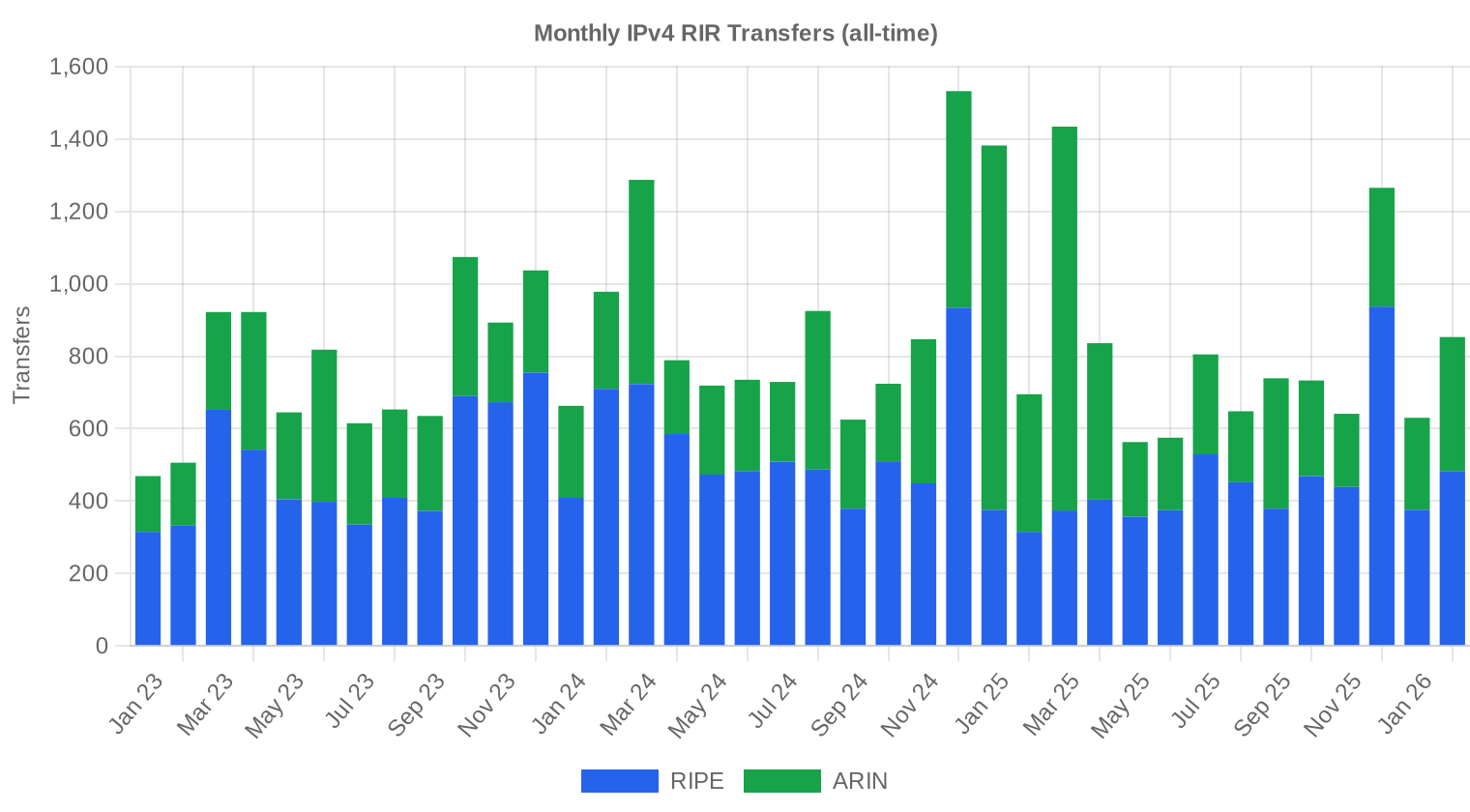

Registry Transfer Activity

Registry data confirms 853 IPv4 transfers during February 2026. RIPE led volume. These figures capture RIR-approved ownership changes — the authoritative measure of real address reallocation.

RIPE 59.6% · ARIN 40.4%

Long-Run Transfer Trends

The aggregate picture: 31,541 IPv4 transfers across 38 months, with December 2024 delivering peak volume. Below, we decompose transfer activity by registry — RIPE, ARIN, APNIC, LACNIC, and AFRINIC — to isolate where momentum is concentrating.

RIR Distribution: RIPE: 59.6%, ARIN: 40.4%, APNIC: 0.0%, LACNIC: 0.0%, AFRINIC: 0.0%

| RIR | RIR Transfers |

|---|---|

| RIPE | 18,795 |

| ARIN | 12,746 |

| RIR Transfers | 31,541 |

Outlook & Forecast

Using ordinary least-squares regression on the trailing monthly price series:

The overall average price per IP is projected to reach $16.36 by December 2026, with a next-month estimate of $20.49 per IP.

- RIPE: projected at $19.16 per IP next month, trending toward $14.64 by December 2026.

- ARIN: projected at $20.94 per IP next month, trending toward $18.11 by December 2026.

- APNIC: projected at $21.92 per IP next month, trending toward $14.71 by December 2026.

- LACNIC: projected at $30.01 per IP next month, trending toward $26.62 by December 2026.

- AFRINIC: insufficient data for a reliable forecast.

Forward curve: approximately $20.49 per IP next month, $16.36 by December 2026. Projections assume continuation of prevailing trends and are subject to revision.

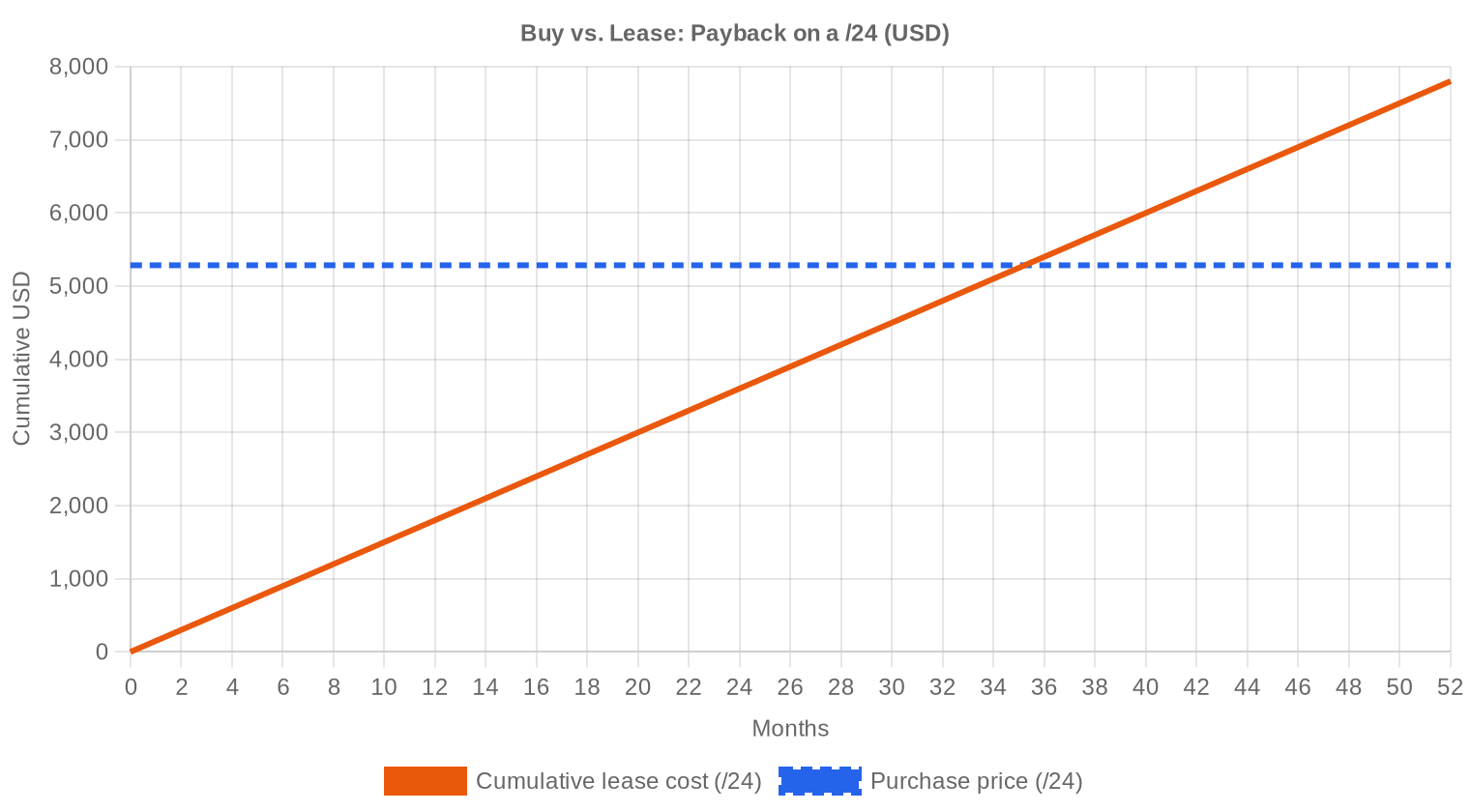

Editor's Take: Buy vs. Lease

The buy-versus-lease calculus: at current rates, /24 blocks lease for approximately $150.00 per month and sell for roughly $5,284. That implies a payback period of 35.2 months (2.9 years) — a gross rental yield of 34.1% annually.

At 35.2 months, the payback period falls well below our 90-month threshold — the economics favor outright acquisition. Operators can buy IPv4 today and rent out IPv4 to offset cost immediately. At these levels, the asset is attractively priced for purchase.

| /24 Purchase price | $5,284 |

| /24 Lease price | $150 / mo |

| Payback period | 35.2 mo (2.9 yr) |

| Gross annual yield | 34.1% |

What This Means for You

Full-lifecycle coverage: buy IPv4 from verified sellers with managed escrow, sell IPv4 through streamlined transfer processes, lease IPv4 for elastic capacity, or rent out IPv4 to generate yield on idle address space.

IPv4 Pricing by Block Size

Block size matters a lot when it comes to IPv4 pricing. A /24 block — the minimum routable unit at 256 addresses — currently sells for roughly $35–45 per IP, reflecting strong demand from smaller operators. Move up to a /16 and per-IP prices drop to the $18–28 range.

| Block | IPs | Buy: /IP | Buy: Total | Lease: /IP/mo | Lease: Monthly |

|---|---|---|---|---|---|

| /24 | 256 | $35–45 | $8,960–11,520 | $0.38–0.50 | $97–128 |

| /22 | 1,024 | $28–38 | $28,672–38,912 | $0.33–0.45 | $338–461 |

| /20 | 4,096 | $22–32 | $90,112–131,072 | $0.30–0.40 | $1,229–1,638 |

| /18 | 16,384 | $20–30 | $327,680–491,520 | $0.30–0.38 | $4,915–6,226 |

| /16 | 65,536 | $18–28 | $1,179,648–1,835,008 | $0.30–0.35 | $19,661–22,938 |

IPv4 Price History: 2011–2026

The IPv4 secondary market effectively began in 2011, when IANA exhausted its free pool and Microsoft acquired 666,624 addresses from Nortel at $11.25 per IP. Prices climbed through the 2010s: $8–15 by 2014 as LACNIC exhausted its pool, $18–24 by late 2019 when RIPE ran out. The 2021–2022 boom pushed prices above $60/IP, driven by hyperscaler build-outs. The correction since has been structural — large blocks to $18–28, small blocks holding at $35–45.

| Year | ~Price/IP | Key Event |

|---|---|---|

| 2011 | $7–12 | IANA free pool exhausted; Microsoft/Nortel deal ($11.25/IP) |

| 2012 | $8–12 | RIPE NCC reaches last /8; begins /22-only allocation |

| 2014 | $10–15 | LACNIC free pool exhausted |

| 2015 | $8–15 | ARIN free pool exhausted |

| 2017–18 | $12–18 | Leasing market grows; cloud demand rises |

| 2019 | $18–24 | RIPE NCC exhausts remaining free pool |

| 2021–22 | $50–60+ | Post-pandemic peak; hyperscaler build-outs |

| 2024 | $35–52 | AWS IPv4 charge ($0.005/IP/hr); large block correction |

| 2025–26 | $18–45 | Market bifurcation; /16s below $20 for first time since 2019 |

Market Structure: Who Is Buying & Selling

The IPv4 market composition has shifted. Demand is no longer dominated by hyperscalers — AWS, Microsoft, Google, and Oracle absorbed roughly 150 million IPs over five years, but that phase has slowed. Today's buyers: ISPs in emerging markets, hosting providers, VPN operators, and AI infrastructure companies. Sellers: legacy telecoms, universities with oversized allocations, and holders splitting /16s for better per-IP pricing.

IPv4 vs. Other Asset Classes

IPv4 functions as a digital infrastructure asset class with real yield. At current rates, a /24 block generates roughly 34.1% gross annual yield through leasing — above commercial real estate (5–8%), bonds (4–5%), or S&P 500 dividends (~1.3%). For pre-2020 acquirers, yields exceed 25% annually. The trade-off: no central exchange, unique risks, and long-term IPv6 displacement.

| Asset Class | Typical Yield | Liquidity | Primary Risk |

|---|---|---|---|

| IPv4 (current acquisition) | 34.1% | Moderate | IPv6 adoption, block quality |

| Commercial Real Estate | 5–8% | Low | Vacancy, rate cycle |

| Investment-Grade Bonds | 4–5% | High | Duration, credit risk |

| S&P 500 Dividends | ~1.3% | High | Market volatility |

| Money Market / T-Bills | ~4–5% | High | Rate cycle changes |

IPv6 Adoption & Why IPv4 Remains Essential

The IPv6 transition is real but much slower than predicted. Around 40–45% of internet traffic uses IPv6, but enterprise and carrier networks still rely on dual-stack. Legacy compatibility, email reputation, and regulatory requirements keep IPv4 firmly in place.

AI & Cloud Infrastructure Demand

AI infrastructure is a growing driver of IPv4 demand. Compute clusters, hybrid training environments, and edge deployments all need routable IPv4 for compatibility. AI companies prioritize rapid scale-up and flexibility without long-term lock-in, making leasing a natural fit.

What Determines IPv4 Block Value

Several factors impact IPv4 block value: block size (smaller = more liquid), reputation (clean blocks command premiums), RIR region (ARIN/RIPE most traded, APNIC highest lease rates), documentation quality (RPKI, LOA, WHOIS), and routing status (announced blocks worth more than dark ones).

Sell vs. Lease: A Decision Framework

The sell-vs-lease decision: capital now versus recurring income. Selling delivers immediate liquidity but gives up the asset permanently. Leasing — with a payback period around 35.2 months and 34.1% annual yield — retains ownership. Under 7–8 years payback, leasing generally wins.

| /24 Purchase price | $5,284 |

| /24 Lease price | $150 / mo |

| Payback period | 35.2 mo (2.9 yr) |

| Gross annual yield | 34.1% |

RIPE NCC 24-Month Transfer Restriction

RIPE NCC enforces a 24-month holding requirement on transferred blocks. Acquired blocks cannot be re-transferred for two years. Leasing is unaffected — only ownership transfer is locked. Investment buyers should build this into ROI calculations.

Deal Size Distribution

| Value Band | Deals | Share |

|---|---|---|

| < $50K | 78 | 83.0% |

| $50K – $250K | 7 | 7.4% |

| $250K – $1M | 3 | 3.2% |

| > $1M | 6 | 6.4% |

Top Trading Countries

| # | Country | Transactions | Share |

|---|---|---|---|

| 1 | US | 47 | 50.0% |

| 2 | GB | 22 | 23.4% |

| 3 | NL | 4 | 4.3% |

| 4 | IT | 3 | 3.2% |

| 5 | CA | 2 | 2.1% |

| 6 | IE | 2 | 2.1% |

| 7 | GB,SG | 1 | 1.1% |

| 8 | ZZ | 1 | 1.1% |

| 9 | UA | 1 | 1.1% |

| 10 | ES | 1 | 1.1% |

BEAD Broadband Program Impact

The US government's Broadband Equity, Access, and Deployment (BEAD) program has allocated $42.45 billion to expand internet access in rural and underserved areas. As funds flow primarily to regional ISPs who need IPv4 addresses for network buildouts, industry participants expect significant tightening of IPv4 supply — particularly for mid-sized blocks (/20 to /22) favored by smaller providers. BEAD recipients must meet audit and lawful access requirements that complicate carrier-grade NAT usage, making unique IPv4 allocations the preferred deployment path.

Hyperscaler IPv4 Holdings

Major cloud providers have accumulated massive IPv4 portfolios. AWS alone holds an estimated 191 million IPv4 addresses worth approximately $6.7 billion at current market rates. Microsoft, Google Cloud, and Oracle have collectively absorbed roughly 150 million addresses over the past five years. While the pace of hyperscaler accumulation has slowed as these companies increasingly build IPv6-native infrastructure, their existing holdings represent a significant portion of the total allocated IPv4 space and are unlikely to return to the secondary market.

Macroeconomic Conditions & Market Impact

Macroeconomic conditions affect IPv4 pricing. Tight capital markets slow acquisitions, pushing prices down. High interest rates increase the opportunity cost of IPv4 purchases, favoring leasing. Government programs like the $42.45B US BEAD broadband expansion can create regional demand surges.

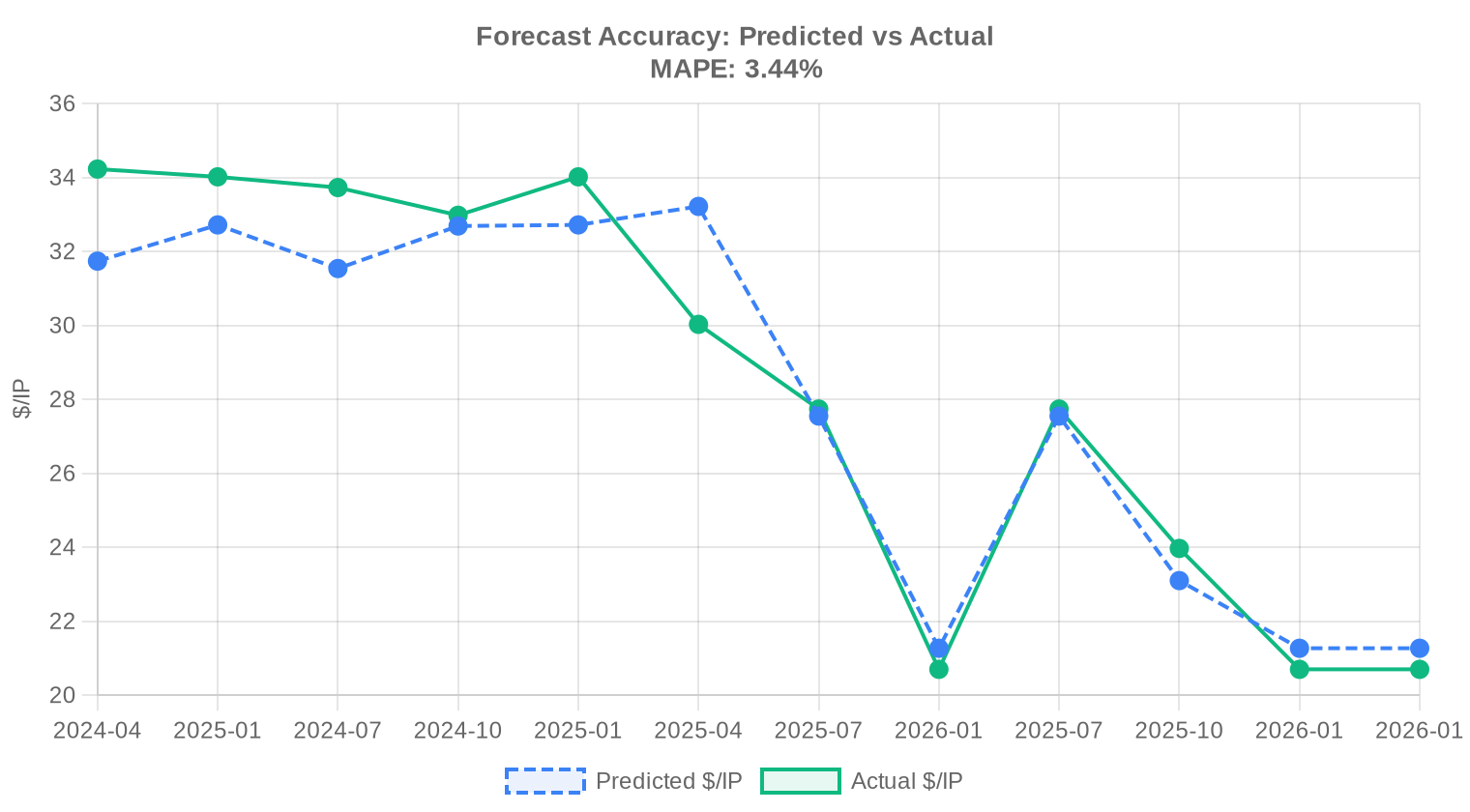

Model Update & Calibration

As part of our continuous improvement process, we backtested previous forecasts against realised prices and fine-tuned the model accordingly. Recent months now carry more influence than older data, and the confidence bands have been widened or narrowed based on how well they captured actual outcomes in the past. You can see the full backtest results in the table and chart below.

| Report Period | Target Month | Predicted | Actual | Deviation |

|---|---|---|---|---|

| 2025-H1 | 2025-07 | $28 | $28 | -1% |

| 2025 | 2026-01 | $21 | $21 | +3% |

| 2025-Q2 | 2025-07 | $28 | $28 | -1% |

| 2025-Q3 | 2025-10 | $23 | $24 | -4% |

| 2025-H2 | 2026-01 | $21 | $21 | +3% |

| 2025-Q4 | 2026-01 | $21 | $21 | +3% |

Methodology

Figures are based on completed IPv4Center marketplace transactions and RIR transfer statistics. Prices are expressed in US dollars per IP address. Forecasts use linear regression over the trailing 24 months and are estimates, not guarantees.

Source: IPv4Center.com market data and RIR transfer statistics.

This report is generated automatically for informational purposes only and does not constitute financial advice.

Frequently Asked Questions

What was the average IPv4 price in February 2026?

During February 2026, IPv4 addresses traded at an average of $20.64 per IP, with a median of $21.75.

Which RIR had the most expensive IPv4 addresses in February 2026?

ARIN recorded the highest average per-IP price during February 2026.

What's the IPv4 price forecast looking like?

Based on regression analysis of historical data, per-IP pricing is projected near $16.36 by December 2026. Keep in mind this is a projection, not a guarantee.

Should I buy or lease IPv4 right now?

At current price levels, buying pays back in roughly 35.2 months of equivalent lease payments. Below about 90 months, buying usually makes better long-term sense; above that, leasing helps preserve capital.